For those who prefer to listen rather than read, this article is also available as a podcast on Spotify.

Contents:

Plenty of traditional bank execs lately are genuinely worried. They see their younger customers drifting away to apps that feel more like social media than finance tools. For example, 35% of Gen Z want to switch their primary account to a digital-first bank. Yeah, the old way of doing things is just too slow and, frankly, too expensive. Maintaining those massive legacy systems and physical branches eats up budgets that could be spent on innovation.

Startups, on the other hand, see a golden opportunity. By building custom neobank apps, they can slash operational costs dramatically. No branches means no rent, no tellers, no endless paper trails. Plus, they can actually listen to what users want and push updates in weeks, not years. However, building a digital banking infrastructure is a complex dance of real-time ledgers, third-party integrations, and navigating a maze of regulations that change depending on which side of the border you’re on.

That’s exactly why we put this guide together. We’re going to pop the hood and look at the engine. First, we’ll break down neobank app development. Then, we’ll walk through the key features that users actually care about today. We’ll also get into the nitty-gritty of the development process and technologies. Should you go cloud-native? Which APIs are worth the headache? And finally, compliance and security. We’ll cover what you need to know to sleep at night knowing your users’ money is safe.

What Is a Neobank App?

At its core, a neobank is a financial institution that exists only in the digital realm. No marble columns, no waiting lines, no awkward small talk with a teller who’s clearly having a bad day. It’s banking stripped down to its essentials and rebuilt for smartphones.

The biggest difference from traditional banks is the mindset. Old-school banks are basically tech companies that happened to get a banking license decades ago; their systems are often layered like an old cake, with new features glued on top of code written in the 80s. Neobanks are, on the contrary, born digital. They operate entirely on cloud-based platforms, which means they can update features overnight and scale up instantly when traffic spikes. It’s a little scary how fast they move compared to the giants, honestly.

But not all neobanks are built the same way. In my experience, confusing the different models is where a lot of founders get tripped up early on. Let’s break it down.

Types of neobank models

Full-stack neobanks

These are the heavy hitters. Full-stack neobanks operate with their own banking licenses. They hold the deposits, manage the risk, and deal directly with regulators. It’s impressive, sure, but wow, is it expensive and slow to get there. You’re looking at years of groundwork, neobank development, and millions in capital before you can even launch. If you’ve got the patience and the deep pockets, though, the control you get is unmatched.

Neobanks with banking partners

This is the route most startups take, and for good reason. This type relies on traditional banks for the heavy lifting: holding the actual money, insuring deposits, and handling the regulatory backend. While the neobank focuses on what it does best: the user experience, the app interface, and the customer service. The trade-off? You have to share revenue with your partner bank, and you’re somewhat limited by their legacy systems. But honestly, for 90% of use cases, it’s the smartest play.

Niche neobanks

Instead of trying to be everything to everyone, niche neobanks focus on specific audiences. Maybe it’s an app designed specifically for freelancers to handle irregular income and taxes automatically. Or perhaps one built for SMEs that integrates directly with accounting software. Some are even targeting crypto users, delivering crypto-enabled financial services and bridging the gap between digital assets and fiat currency. By narrowing the focus, these apps can solve very specific pains that big banks just ignore.

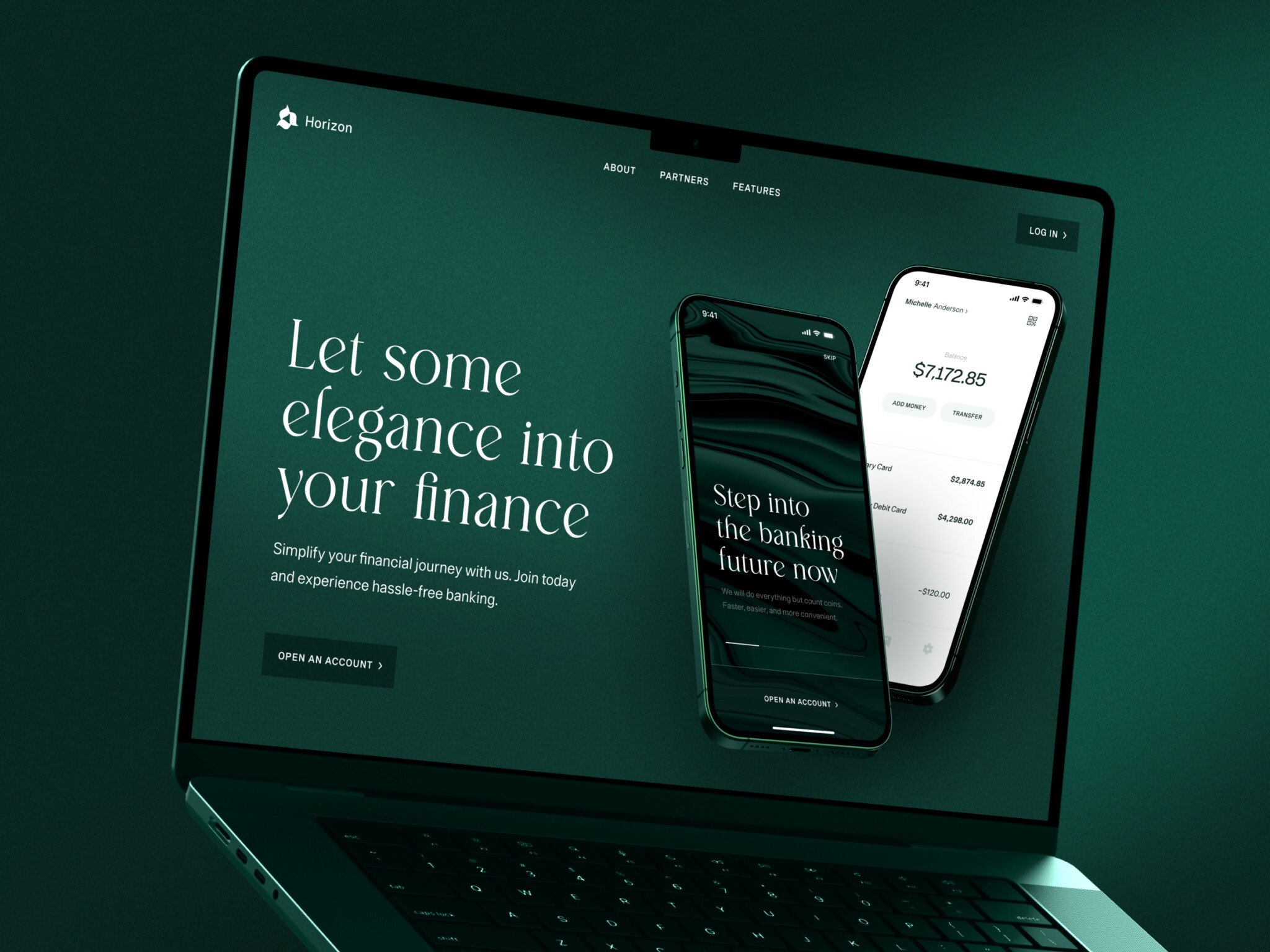

Mobile Banking App by Conceptzilla

Core components of neobank apps

Okay, so you’ve picked your model. What should you pack under the hood during mobile banking app development? Because if you think it’s just an app on a phone, well, you’re in for a surprise. A functioning neobank is more like an orchestra of different systems playing in perfect sync.

For starters, you need the mobile banking application. It’s the face of your operation, what your customers see and interact with. It has to be easy to navigate, easy to use, and accessible. No walls of text or raw data, just glanceable reports to manage finances. If the app lags or crashes, you’re done.

The backend banking system is the brain. It manages accounts, calculates interest, tracks balances in real-time, and makes sure the ledger never lies. When people send money via wire, swipe a card or scan a QR code, the payment processing infrastructure deals with the actual movement of funds. With its help, you connect the systems to networks like Visa, Mastercard, or local clearinghouses. Setting up this infrastructure requires a lot of skill, because one failed transaction can lose you a customer forever. Or even damage your reputation.

Compliance systems are a vital part of your future project since they handle KYC (Know Your Customer), anti-money laundering checks, and fraud detection. Running in the background, they are constantly vetting transactions to keep you out of legal trouble. Yeah, it may be a little annoying for people to take selfies to verify their identities, but they quickly get used to it when they clearly know it keeps the bad actors out.

Finally, the analytics platforms. They help you spot good or bad patterns, for example, why users are leaving or what features they love. You can track every click, every transaction, and every drop-off point.

Put it all together during digital banking app development, and you’ve got a machine that’s far more complex than it appears on the screen.

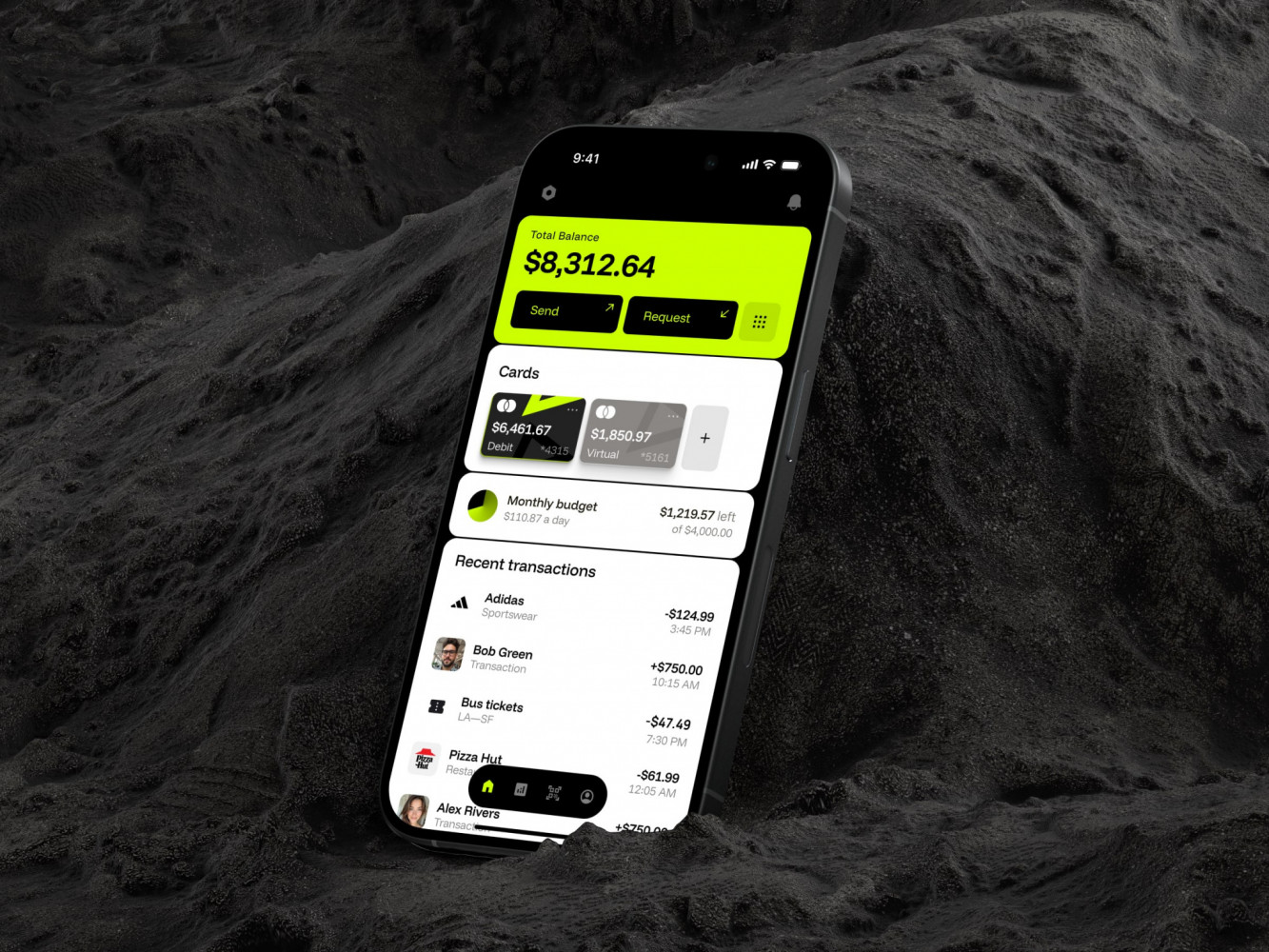

Mobile Banking App by Coneptzilla

Key Features of a Neobank App

If your neobank app doesn’t do the basics perfectly, nobody cares about your fancy AI features or crypto integrations. Users judge you on whether they can see their money and move it without a headache. Beautifully designed apps can fail because they couldn’t handle a simple transfer without crashing.

So, what actually makes the cut? What are the features that users expect as standard these days?

Account Management

User onboarding and account creation used to mean filling out ten pages of paperwork and waiting a week for approval. Now, it needs to happen in minutes, right there on the phone. If it takes longer than five minutes, people bail.

Balance tracking and transaction history have to be flawless in real-time. Nobody wants to wait until tomorrow morning to see that coffee purchase.The history needs to be searchable, categorized, and easy to read on different screen sizes.

Users tend to refresh their balance obsessively, especially when they’re tight on cash. If the number is wrong or delayed even by an hour, trust evaporates instantly.

Payments and Transfers

Peer-to-peer transfers are basically the heartbeat of modern banking. If a user splits a dinner bill or pays a roommate, it should be as easy for them as sending a text message. It should feel frictionless, almost invisible. If I have to ask for a routing number and account digits just to send twenty bucks, something has gone wrong during neobank software development.

Traditional banks often charge a fortune for international payments and take days to process them. Neobanks have a huge advantage here by offering near-instant transfers with transparent, low fees. Getting payment processing infrastructure right is a massive selling point for travelers and expats. If you can make sending money abroad as easy as domestic transfers, you’ve got a winner.

Cards and Spending Management

Physical cards are still a thing, but how you manage them digitally matters more. Debit card management needs to give users total control. Freeze the card instantly if it’s lost? Check. Generate virtual cards for sketchy online shopping? Absolutely. Change the PIN without calling a call center? Yes, please. Granting users this kind of power makes them feel safe and cared for.

Speaking of caring, financial analytics dashboards and budgeting tools help people not to overspend and save money for something that matters. They can understand their habits. “Wait, did I really spend that much on takeout last month?” Good apps answer that question automatically with nice charts and alerts. It helps users catch overspending before it becomes a problem.

Security and Compliance

GDPR, KYC, and AML verification are the gatekeepers in neobank app development. They need to be smooth, though, because making the user upload blurry photos three times is a hassle. The tech has to be smart enough to check identity quickly while keeping the bad guys out.

Another component, AI-driven fraud detection systems, run silently in the background, watching for weird patterns. Did someone just try to buy a TV in London when you’re in New York? The app should flag it instantly. Yes, false alarms are possible when you have to verify a legit purchase. But it’s better than having the account drained. It gives you peace of mind knowing someone (or something) is watching your back.

Mobile-First Experience

66% of people in the world use mobile banking. So your product should have a native version for iOS and Android, with high performance and responsive features. If the app feels clunky, users assume the bank is clunky too. This also includes designing for different screen sizes and OS versions.

An optimized user experience for mobile banking means designing for thumbs. Big buttons, clear navigation, and biometric login (FaceID or fingerprint) are must-haves. Nobody wants to type in a long password every time they open the app. Especially while being outdoors.

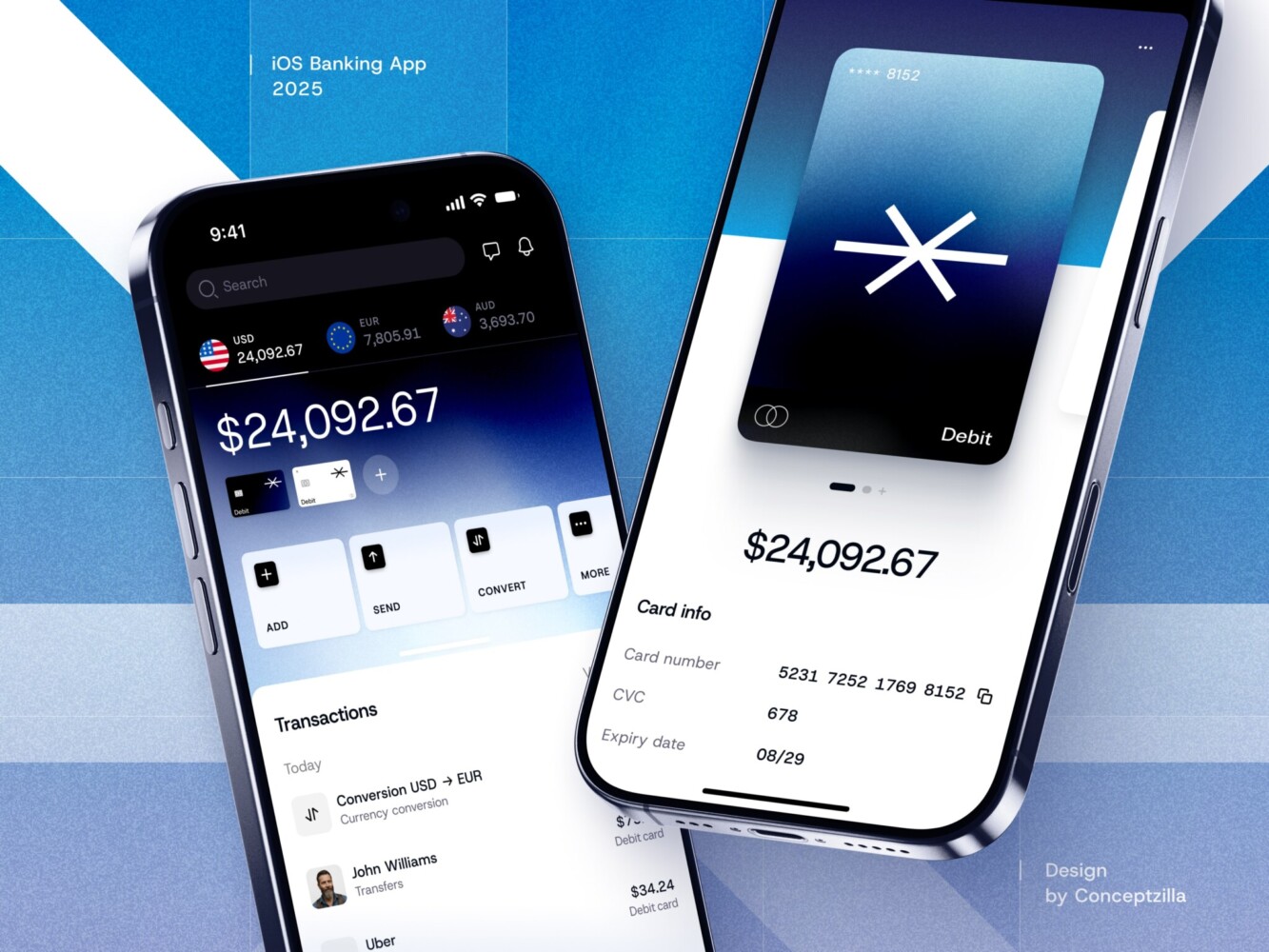

Fintech Mobile Banking App by Conceptzilla

Neobank App Development Process

You can’t just “move fast and break things” here because if you break things, people lose money, and regulators come knocking. Many teams rush into coding without a solid plan, only to hit a wall months later when they realize they missed a critical compliance step or picked a tech stack that can’t handle real-time transactions. So, let’s walk through the actual process, step by step.

1. Product Strategy and Regulatory Planning

First and foremost, get your head around the business side and decide on the business model clearly. Are you targeting freelancers? SMEs? Gen Z? Your model dictates everything from features to revenue streams.

You also need to check compliance requirements and licensing right out of the gate. This part is honestly a bit of a headache. Depending on where you operate, you might need a full banking license (which takes years) or you can partner with an existing bank. In my experience, talking to legal experts early saves you from massive pivots later.

2. UX/UI Design for Banking Apps

Once the strategy is set, it’s time to design. Remember, people are dealing with their life savings here. If they can’t find the “transfer” button in two seconds, they’ll panic. So all the elements should be intuitive and easy to find.

When you dive into fintech app development, just remember the old-fashioned, traditional banking apps and the feeling you got trying to figure something out. And do the opposite: focus on simplicity and trust. Use clear language, avoid jargon, and make sure every action feels secure. Avoid “creative” decisions when users can’t tell if a payment goes through.

Keep it clean, keep it obvious, and add a little animation as a micro-interaction. It reassures that the action is successful and really helps calm nerves.

3. Choosing the Technology Stack

Picking the wrong tools can haunt you forever. There is a lot on your plate: scaling, team’s skills, budget, app type, target platforms, etc. But here are the technologies worth your attention:

For backend, you have reliable options like Java for its stability in financial systems, or Node.js if you need high concurrency for real-time updates. In case you want to pursue rapid development and data-heavy tasks, opt for Python with FastAPI. If you’re deep in the Microsoft ecosystem, C# is a great choice.

Speaking about creating interactive interfaces, React is still the king for web dashboards. But when it comes to mobile, you’ll likely go with native frameworks (Swift for iOS, Kotlin for Android) or cross-platform tools like Flutter or React Native.

If we take a look at databases, PostgreSQL is the go-to for reliable transactional data with ACID compliance. Redis handles caching and real-time sessions beautifully. Docker and Kubernetes will help you containerize and orchestrate everything for building infrastructure.

4. Core Banking and API Architecture

In custom neobank app development, building a monolith is an unwise idea. An architecture based on microservices is mandatory. Why? Because if the “notifications” service crashes, you don’t want the “payments” service to go down with it. Breaking the system into small, independent services makes it resilient and easier to update.

API integrations with banking infrastructure are the heavy lifting in this process. You’ll be connecting your app to core banking providers, payment rails, and identity verification services. Just like connecting little threads to create an intricate web. These APIs are the lifelines of your app. If they’re slow or unreliable, your app is dead in the water.

That’s why spend extra time designing a robust API gateway to manage all core banking systems.

5. Integrations with Financial Ecosystems

Your neobank app can’t exist in a vacuum. You have to connect it to payment processors like Stripe to deal with transactions, blockchain-based financial systems, card providers such as Marqeta to issue physical and virtual cards, and financial data services to group accounts or check income.

Each integration brings its own quirks and documentation challenges. So it’s better to be somewhat pessimistic and assume third-party services might fail. Build fallbacks just in case.

6. Testing and Compliance Verification

Before you even think about launching, you have to test. And I don’t mean just clicking around to see if buttons work. You need rigorous security testing. Penetration testing, vulnerability scans, the whole nine yards. Hackers love fintech apps, so you have to be tougher when doing mobile banking app development.

Apart from testing, there are compliance audits. Regulators will want proof that your KYC and AML systems work exactly as promised. This part is tedious, sure, but it’s your shield against fines and reputation damage.

Finally, run extensive performance testing. Simulate thousands of users hitting the app at once. Does it lag? Do transactions queue up? If the answer is yes, go back to the drawing board. It’s better to delay launch than to launch broken.

7. Deployment and Maintenance

Launch mobile applications on the App Store and Google Play. But honestly, launch day is just the beginning. Now you need to monitor system performance 24/7.

Set up alerts for everything: failed transactions, high latency, server spikes, etc. You’ll be sleeping with your phone next to your bed for a while because the work never really stops. You’ll need continuous updates and improvements. Users will ask for new features, regulations will change, and bugs will pop up.

Treat your app as a living product, not a one-time project. It’s a little exhausting, but seeing people actually use and love what you built makes it all worth it.

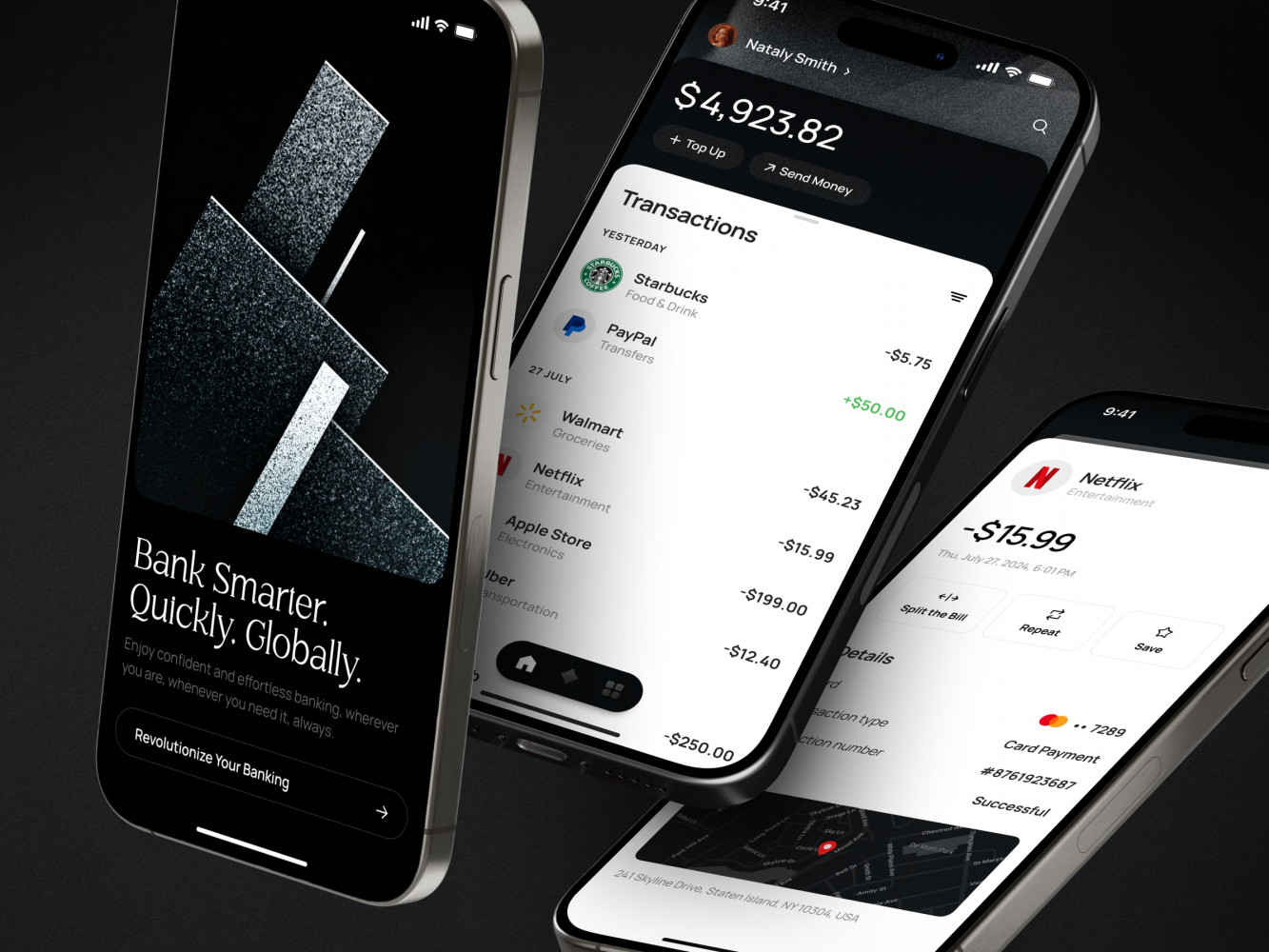

Finance Management Mobile App Design by Shakuro

Cost of Neobank App Development

Money is always an awkward subject for discussion. Specifically, how much it’s actually going to cost you to build such an app. Many founders have the same problem: there is a brilliant idea but a spreadsheet that looks like it was drawn on a napkin.

Key Cost Factors

First up, compliance requirements. They are a silent budget killer. You can have the sleekest app in the world, but if you aren’t compliant, you’re shut down before you launch. Getting your licenses or partnering with a licensed bank, setting up KYC/AML systems, and hiring legal experts to navigate local laws—that alone can eat up 30-40% of your initial budget. Skipping them altogether is tempting, I get you, but the fines are way more expensive than the setup.

The scope creep is real. Do you need just basic transfers, or do you want crypto trading, investment portfolios, and AI-driven budgeting? Every extra feature adds more lines to the blueprint, more complexity in testing, security checks, and tech stacks. Teams often start with a “simple” list that doubles in size by month three. Be honest about what you need versus what you want.

Integrations with banking infrastructure eat a huge chunk of your budget as well. You’re connecting to core banking providers, card issuers, payment rails, and identity verification services. Each of these partners charges setup fees, monthly minimums, and per-transaction costs. Plus the engineering hours needed to glue all these APIs together seamlessly. I’d compare it to assembling a puzzle where every piece comes from a different manufacturer and speaks a different language. A nightmare in the world of Lego.

Custom neobank app development also brings complexity in mobile versions. Are you going native (iOS and Android separate) or cross-platform? Do you need biometric login, offline modes, or complex animations? The more polished and secure the app needs to be, the more senior talent you need. Senior fintech developers don’t come cheap. You get what you pay for and cutting corners here usually leads to security breaches or a clunky user experience that drives customers away.

Example Scenarios

Let’s illustrate potential costs with two common scenarios. Keep in mind, these are rough estimates. The numbers differ wildly depending on your location, team skills, and partners.

MVP Neobank App

In the first case, your goal is to prove the MVP concept with a niche audience, maybe freelancers in one country. You’re partnering with an existing bank for the license and core infrastructure. The feature set is lean: account opening, basic P2P transfers, a debit card, and transaction history. No investments, no crypto, no fancy AI.

That’s why you’re looking at a development timeline of maybe 4-6 months. The cost is probably somewhere between $40,000 and $70,000. This covers a small team of experienced devs, design, basic compliance setup, and the initial integrations. It’s not pocket change, but it’s manageable for a seed-round startup. Just don’t try to add “one more feature” before launch.

Full-Fledged Digital Bank

Let us talk about something else now. Suppose you want to reach the moon and go further. You would like to build a neobank app from scratch—fully licensed, operating in multiple countries, offering not only payment services but also lending, depositing, investment opportunities, insurance, and crypto. In such an instance, you require a highly scalable backend able to handle millions of transactions, round-the-clock service, fraud prevention, etc.

In this case, we speak about a neobank app development company consisting of 20-50+ people. You will need experienced compliance specialists, security experts, engineers, and many others. As for the timeline, here it will be 12-18 months or even more. Just to mention that for a neobank app to appear, you need to invest at least $300,000.

Yes, these figures look impressive. However, attempting to save money on it leads to rewriting, additional expenses, penalties, and failures. Better have realistic estimates about expenses from the beginning, make your plans carefully, and keep prioritizing ruthlessly. Cutting expenses turns out to be one of the costliest moves in neobank development.

Dark theme for a fintech app by Shakuro

Common Problems With Neobank Development

It looks like all you have to do is to create a neat and functional application with API connectivity. Then your users will come pouring. Yet, this is only what happens in theory.

Here are the big hurdles you’re going to face, and trust me, they aren’t just minor bumps in the road.

Regulatory Compliance

Regulatory compliance is a constant, shifting landscape you have to navigate every single day. Rules change depending on which country—or even which state—you’re operating in. One day you’re fine, the next day a new anti-money laundering (AML) law drops, and suddenly your onboarding flow is broken.

I’ll dwell on the most popular regulations. First of all, KYC (Know Your Customer). It demands identity verification before delivering financial services to prevent fraud. The AML I mentioned above implements monitoring systems to find money laundering patterns. Regulations such as GDPR are a must for user data privacy and security in the EU and US. If you handle cardholder data, you will have to adhere to PCI DSS.

So, you might have a brilliant feature ready to go, but legal tells you to hold it for six months while they figure out if it violates some obscure banking regulation. In my experience, underestimating this is the fastest way to burn through your cash reserve. You need neobank developers who live and breathe compliance, not just someone who reads a blog post about it once a year.

Security and Fraud Prevention

Traditional banks have decades of legacy security layers, clunky as they may be. As a neobank, you’re a shiny new target. Hackers love fintech startups because, well, that’s where the money is moving fast.

Building secure digital asset management is incredibly tricky. You have to stop bad actors without annoying your good customers. Have you ever had your card declined at a grocery store because the bank thought you were in another country? That’s a false positive, and it’s frustrating.

If your system is too aggressive, users will leave. If it’s too lax, you get hit with chargebacks and theft. Finding that sweet spot takes time, data, and a lot of tweaking. And let’s not forget data breaches. One slip-up, one leaked database, and your reputation is toast.

Integration with Banking Systems

You’d think nowadays, connecting systems would be plug-and-play, right? Wrong. Integration with banking systems is often a nightmare of legacy tech and undocumented APIs. You’re trying to build a sleek, modern app on top of infrastructure that might be running on code written in the 1990s.

Partner banks and payment processors all have their own quirks. One API might return data in JSON, another in XML, and a third might just timeout randomly for no reason. Making all these pieces talk to each other smoothly, in real-time, without dropping transactions is an engineering marathon. It’s messy, it’s complex, and it requires a lot of patience.

User Trust and Onboarding

To comply with regulations, you need to ask users for a lot of personal info: ID scans, selfies, proof of address, etc. But to gain trust and keep users engaged, you need the process to be instant and frictionless.

It’s a tough balance to keep in digital banking app development. If your onboarding takes ten minutes and asks for too much, people drop off. They get suspicious or just bored. But if you make it too easy, you risk letting in fraudsters or failing compliance checks.

How do you make someone feel safe handing over their life savings to an app they downloaded five minutes ago? Well, the product should be transparent and easy-to-navigate and show confidence that when things go wrong, your support is there instantly. Building that emotional connection takes time, and frankly, it’s harder than writing the code.

So, yeah, it’s challenging. Overcoming these hurdles is exactly what makes a neobank valuable. If it were easy, there’d be no moat, no competitive advantage.

Abyss app by Conceptzilla

Our Experience in Fintech Product Development

At Shakuro, we’ve spent 19 years deep in the trenches of fintech product development. It’s not just a buzzword for us; it’s basically our daily bread.

Our experience isn’t limited to just one corner of finance. We’ve tackled everything from mobile fintech applications that live in your pocket to massive financial platforms. Our team built complex SaaS systems for B2B finance and designed scalable backend architectures that don’t flinch when traffic spikes.

In neobank software development, we focus on responsive UX and a robust backend. Thanks to a close collaboration between developers and designers, time-to-market is much shorter. Glanceable reports powered by AI make managing finances a pretty simple task. At the same time, we pay attention to security: the team follows GDPR, KYC, and other international standards, as well as signs NDA.

We know that for a founder, a delay in launch isn’t just a timeline slip—it’s missed revenue. If you’re looking to build something that stands up to scrutiny and scales with ambition, well, you know where to find us.

ZAD: Developing a Responsive App for Middle East

The company needed a Shariah-compliant fintech platform for both beginners and experienced traders. Building an ethical financial product like this adds a whole other layer of complexity. We had to ensure every feature, every investment pool, and every transaction aligns with strict Islamic finance principles. No interest (Riba), no uncertainty (Gharar).

ZAD required a completely different approach to the backend than a standard interest-bearing account. We had to build systems that could automatically calculate and distribute profits based on actual performance, ensuring total transparency and compliance. We managed to create a user experience that felt just as smooth and modern as any mainstream neobank, while strictly adhering to those religious guidelines. For beginners, we integrated a robo-advisor feature that gives them firm ground while they are learning. And professionals got glanceable, detailed reports with analytics.

Risk profiling in ZAD app

Why Work with a Neobank App Development Company

The idea of building everything in-house is tempting. You want full control, you want to own the IP, and honestly, there’s a certain pride in saying your team built the whole thing from scratch. I’ve seen founders try to hire a bunch of generalist devs and hope for the best. But fintech isn’t like building an e-commerce site or a social media app. The stakes are just different. When a button doesn’t work on a shopping app, someone gets annoyed. When it doesn’t work in a banking app, someone loses money, and you get sued.

That’s why partnering with experienced neobank developers often makes way more sense than trying to go it alone. It’s not about lacking talent; it’s about leveraging specific expertise that takes years to build. Let’s break down why this move can actually save your sanity (and your budget).

Expertise in Mobile Banking

First off, there’s a huge difference between coding an app and coding a banking app. General developers might be great at React Native or Swift, but do they understand the nuances of real-time ledger updates? Do they know how to handle offline modes without creating double-spend errors? Probably not yet.

A neobank app development company has already solved the tricky problems you’re just about to encounter. They know how to design interfaces that make complex financial data look simple. They understand the psychology of a user checking their balance at 2 AM with no lights.

These specialists predict user behavior in a financial context. They know that a two-second delay in a transaction status can cause panic, so they optimize for speed and clarity in ways a generalist team might overlook. It really helps to have someone who’s already made the mistakes so you don’t have to.

Scalable Fintech Architectures

A lot of startups start with a monolithic architecture or just slap some templates because it’s faster to build from the start. But what happens when you hit Black Friday traffic? Or when you suddenly expand to a new country? The whole system can crumble.

Custom neobank app development brings flexible systems to the table from day one. People are used to building microservices that can handle millions of transactions per second without breaking a sweat. They know how to structure databases for ACID compliance while still keeping things fast. They’ve designed systems that can plug in new payment rails or currency supports without rewriting the whole core.

Having a foundation that can grow with you is way better than having to rebuild everything six months after launch, right? It’s like building a skyscraper instead of a shack; you want it to stand tall when the storm hits.

Compliance and Security Expertise

This is the area where DIY projects usually crash and burn. Regulations like GDPR, PSD2, KYC, and AML are a moving target. They vary by region, they change frequently, and the penalties for getting it wrong are brutal.

Seasoned neobank developers don’t just treat compliance as an afterthought. It’s baked into their DNA. They have security experts who know exactly how to encrypt data, manage keys, and set up fraud detection systems that actually work. They’ve already gone through audits. They know what regulators are looking for before the auditors even walk in the door.

If you are trying to learn all this on the fly while building your product, you are cooking a recipe for disaster. Working with experts gives you a shield. It lets you sleep at night knowing your users’ money and data are protected by industry standards, not just hopeful guesses.

So, yeah, hiring a specialized team costs money upfront. No doubt about it. But when you factor in the time saved, the risks avoided, and the robust foundation you get, it often turns out to be the best option in the long run. It lets you focus on what you do best—building your brand and finding customers—while leaving the heavy technical lifting to people who do it every single day.

Mobile Banking App by Conceptzilla

Final Thoughts

If you’ve made it this far, you probably realize that building a neobank is orchestrating a complex symphony of regulations, technology, and human trust. It’s a journey that starts with a spark of an idea—maybe solving a specific pain point for freelancers or making cross-border payments actually make sense. But that idea is just the beginning.

Successful neobank app development relies on three non-negotiable pillars. First, a seamless user experience. If your app feels clunky or confusing, users will bounce before they even deposit a dollar. It has to be easy to use and easy to navigate. Second, strong security. Without ironclad protection against fraud and breaches, you have a liability. And third, scalable infrastructure. You need a system that can handle ten users today and ten million tomorrow without breaking a sweat.

You don’t have to figure all this out alone, though. In fact, trying to do it all in-house without any fintech experience is exactly how projects stall or fail. The landscape is too tricky, the regulations too dense, and the tech stack too specialized. That’s why my biggest piece of advice is simple: partner up with a neobank app development company. They bring the battle-tested knowledge, the security protocols, and the architectural blueprints you need to skip the painful trial-and-error phase.

So, if you’re ready to turn that idea into reality, reach out to a team that’s already walked this path. Let’s build something that actually transforms how people handle their money.