You know that feeling when you’re trying to log into a government portal, or maybe just checking your bank balance, and the system asks for three different passwords, a code from an app and then suddenly decides it doesn’t recognize your face? It’s frustrating. Makes you wonder if the whole digital world is working against us.

For product leaders and public-sector folks alike, the pressure is real. You need security, sure, but you also need speed. You need trust. But how do you build that when every new regulation seems to add another layer of complexity?

That’s where digital identity platforms come in. In my experience, most people hear “digital identity” and think of passwords or biometrics. But it’s way bigger than that. It’s about creating a seamless, secure way for people to prove who they are online without jumping through hoops. And if you’re leading a team, whether in tech or public service, ignoring this shift isn’t really an option anymore.

So, let’s dig into it. What exactly is a digital identity platform development? Why does it matter now more than ever? And how can it help you stop losing sleep over compliance issues and user drop-offs? Stick around—I promise it’s worth the read.

What Is a Digital Identity Platform?

It is software infrastructure that helps an organization verify, authenticate, manage, and protect a person’s identity across digital services. In plain English, it helps answer three questions: who is this person, are they allowed to do this, and can we prove what happened later if something goes wrong?

That usually includes identity proofing, account creation, authentication, access control, consent, audit logs, recovery flows, and integrations with other systems. In more advanced setups, it may also include biometrics, fraud scoring, digital wallets, passkeys, federation, and reusable verified credentials.

So, when someone asks what is a digital identity platform, the best short answer is this: it is the trust layer between people and digital services. It is not only a login screen, and it is not only an ID scan. It is the system that connects verification, access, privacy, and accountability.

By the way, the “accountability” part is easy to underestimate. A login page can look calm and tidy on the surface, while the background is full of awkward exceptions. Manual reviews in spreadsheets. Admin roles nobody remembers creating. Old users migrated from another system with half-complete profiles. We have all seen some version of this. It works until it does not.

Verification, Management, and the Full Identity Layer

A digital identity verification platform focuses on proving that a person is who they claim to be. It may check a government ID, compare a selfie to a document photo, run liveness detection, verify an address, check databases, or look for risk signals. Fintech teams often connect this to KYC and AML workflows. Marketplaces may use it to screen sellers. Healthcare systems may use it before giving access to sensitive patient data.

A digital identity management platform has a different job. It manages identities over time. Think user lifecycle, roles, permissions, multi-factor authentication, single sign-on, account linking, passwordless login, device management, and account recovery. It is less about the first proof and more about daily access.

The fuller platform brings both sides together. A user may verify once, then authenticate many times. Their access may change when they become an admin, move to a new department, lose eligibility, or request a sensitive action. Their consent may need to be recorded. Their activity may need to be audited. One piece without the others can leave gaps.

This is one of those things that sounds obvious only after you have dealt with the mess. Verification without good access management creates friction later. Access management without proper proofing can be risky. And both, without a decent user experience, can make honest users feel punished.

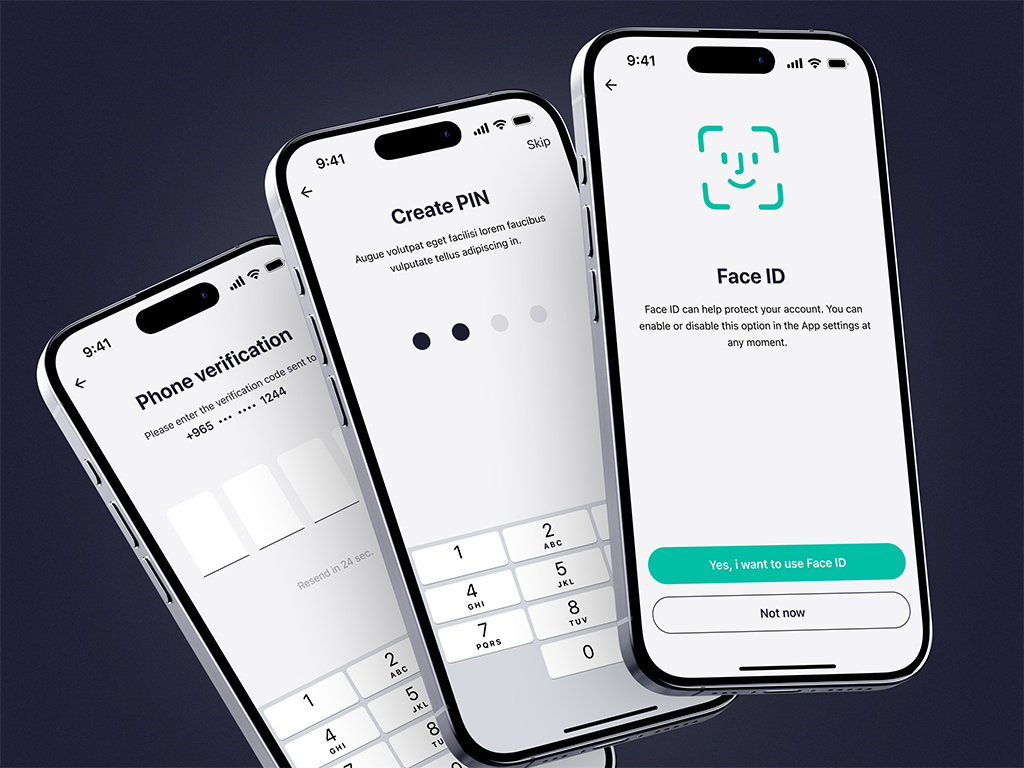

ZAD app by Shakuro

Who Needs Digital Identity Infrastructure?

Fintech and banking teams usually feel the pressure first. They need onboarding, KYC, fraud checks, strong authentication, transaction risk controls, and clear audit trails. If a user cannot open an account, the business loses revenue. If the wrong person gets access, the damage can be much worse.

Healthcare has its own version of the problem. A patient portal, telehealth app, or insurance workflow has to balance convenience with sensitive records. People forget passwords. Family members help older relatives. Providers need different levels of access. There is emotion in this too, because nobody wants to fight with an identity flow while dealing with a medical issue.

SaaS products and marketplaces need identity as they grow. At first, a simple email login may be enough. Later, customers ask for SSO, audit logs, admin roles, user provisioning, session controls, and compliance reports. If enterprise clients are involved, identity becomes part of the sales conversation.

Education, certification, and membership products also benefit from digital identity platforms. Diplomas, licenses, exam results, paid access, event credentials, and professional profiles all need some level of trust. Even a small membership app can run into awkward cases: shared accounts, expired access, fake profiles, or benefits used by the wrong person.

And then there is the public sector. A digital identity platform for government agencies has to handle scale, accessibility, privacy, legacy systems, and a wide variety of life situations. Someone may be applying for benefits, renewing a license, accessing tax records, or proving eligibility for a local service. The stakes are not abstract. If the flow fails, a real person may lose time, money, or access to something important.

Core Features to Plan From the Start

The exact feature set depends on the product, but a serious identity system usually includes a few common parts.

First comes identity proofing. This may include document capture, OCR, biometric comparison, liveness checks, database validation, address checks, or manual review. The point is not to collect as much information as possible. The point is to collect enough evidence for the risk level and no more than needed.

Then comes authentication. Passwords are still around, of course, but many teams are moving toward multi-factor authentication, passkeys, magic links, hardware keys, authenticator apps, or enterprise SSO. NIST’s current digital identity guidelines separate requirements for proofing, authentication, and federation. That split is useful because these are related concerns, but they are not the same job.

Access control is the next big piece. Role-based access control works for many products, at least at the beginning. More complex systems may need attribute-based rules, approval workflows, delegated access, or fine-grained policies. A hospital admin, a doctor, a billing clerk, and a patient should not see the same things. Sounds basic. It gets tricky in real interfaces.

A good platform also needs consent and privacy controls. Users should understand what data is being requested and why. Admins should know what they can store, what they must delete, and what they need to keep for audit or compliance. Data retention is not glamorous work, but it saves headaches later.

Finally, do not forget the boring screens. Admin dashboards, review queues, audit logs, support tools, reporting, alerts, and account recovery flows are where the platform becomes usable in real life. I have a soft spot for these “boring” parts because they are often what keep operations sane.

Symbolik case by Shakuro

How the Architecture Usually Works

At the front of the digital identity platform, users see onboarding screens, login flows, verification prompts, consent dialogs, recovery forms, and profile settings. This layer has to be clear. If people do not trust the interface, they may abandon the process or call support before anything even breaks.

Behind that sits the verification and risk layer. It may connect to document verification providers, biometric services, fraud tools, sanctions screening, government or commercial data sources, and manual review systems. Some organizations build more of this themselves. Others use vendors and focus on orchestration, user experience, and integration.

The identity orchestration layer is where the product decides what should happen next. Does this user need a document check? Is the risk score high enough for manual review? Should the system ask for MFA before a sensitive action? Can this credential be reused, or does it need fresh verification? This rules engine does not need to be fancy at first, but it should be understandable.

Next—authentication and federation. OAuth 2.0, OpenID Connect, and SAML are common here. Enterprise products may need all three at some point, because customers have their own identity providers and no one wants a second login just for your tool. Government-facing systems may also need strict assurance levels and clear integration rules.

The admin layer brings it all together: dashboards, reports, logs, alerts, support workflows, analytics, and compliance exports. This is where a team can spot unusual activity, handle edge cases, and prove that the system behaved as expected.

It sounds like a lot because it is a lot. But it does not have to arrive in one giant release. The better approach for developing a digital identity verification platform is usually to map the risk, build the necessary foundation, and add stronger controls as the product and user base grow.

Security, Privacy, and Compliance Are Product Decisions Too

Security in identity products is not just encryption and a checklist. Those matter, yes. But the product decisions matter just as much. How many retries does a user get? What happens when liveness detection fails? Can support reset an account? Who can see verification documents? How long are images stored? Can users appeal a failed check?

These are not small questions. They shape trust.

NIST SP 800-63-4 is useful here because it talks about assurance levels for identity proofing, authentication, and federation, plus security, privacy, fraud, and user experience considerations. The latest revision also addresses things like syncable authenticators, subscriber-controlled wallets, and forged media. In normal human language: passkeys, wallets, and deepfake-style risks are now part of the identity conversation.

For government and public-service work, Login.gov is a helpful reference point. Its partner materials describe authentication, identity verification, multilingual support, MFA, encryption, SAML or OIDC integration, and FedRAMP Moderate authorization. That list tells you something important: public-sector identity is not just about checking an ID. It is about operating a service people can actually use.

In Europe, the EU Digital Identity Wallet framework is pushing the topic even further. The European Commission describes wallets that let people and organizations access services across member states while protecting personal data and privacy. It also talks about interoperability, relying parties, revocation, certification, and wallet lifecycle management. The details are dense, but the direction is clear: digital identity is moving from isolated accounts toward reusable, controlled credentials.

Solio App by Shakuro

What Makes Government Identity Different?

A digital identity platform for government agencies has less room for casual assumptions. A private app can sometimes say, “This feature is for our core users.” A public service cannot think that way. It has to work for people with old phones, limited documents, disabilities, language barriers, unstable addresses, or low digital confidence.

That makes UX more important, not less. Error messages have to be humane. Support paths have to exist. Accessibility cannot be sprinkled on later. Recovery flows need careful abuse protection, but they also need empathy. Locking someone out of a shopping app is annoying. Locking someone out of unemployment benefits is different.

Government systems also tend to carry old integrations. Mainframes, case-management tools, registries, payment systems, document archives, and agency portals may all need to talk to the identity layer. That is not glamorous work. Sometimes it is slow. But if the system cannot fit into the actual operating environment, the shiny onboarding flow will not save it.

The best public-sector identity projects usually treat trust as a service design problem. People need to know what is happening, why their data is needed, what alternatives exist, and how to get help. Still, it is where many systems stumble.

How to Build a Digital Identity Platform

Step 1. Discovery and Risk Mapping

Who are the users? What actions are sensitive? What proof is enough? Which regulations apply? What systems need to connect? What happens when a user fails a check? This is where product, engineering, legal, security, support, and operations should be in the same room. Maybe not forever. Just long enough to avoid expensive surprises.

Step 2. Design the User Experience

Identity flows are emotional in a quiet way. People are handing over documents, faces, addresses, phone numbers, or access to personal records. A clumsy flow can feel invasive even when the technology is fine. Clear copy, calm screens, progress states, recovery options, and accessible forms really help.

Step 3. Plan the Architecture

Decide what you will build, what you will buy, and where the boundary sits. Many teams use third-party services for document verification or biometrics but still build custom orchestration, admin tooling, business logic, dashboards, and integrations. That can be the best option because it avoids rebuilding specialized verification tech while preserving control over the product experience.

Step 4. Core Development

It usually includes account logic, onboarding, authentication, verification workflows, access rules, user profiles, admin tools, audit logs, reporting, and notifications. Integrations come next, though honestly, they should be discussed from day one. CRM, EHR, core banking, case-management tools, analytics, data warehouses, support tools, and identity providers can all shape the platform.

Step 5. Testing

It needs more than happy paths. Try bad documents. Slow connections. Duplicate accounts. Name changes. Lost phones. Accessibility tools. Fraud attempts. Account recovery abuse. High traffic. Vendor outages. It is a little annoying, but you get used to it over time, and it is better than discovering these cases through angry tickets.

Step 6. Deployment

Identity platforms need monitoring, incident response, vendor checks, compliance reports, support playbooks, and regular reviews of access policies. Users change. Fraud changes. Regulations change. The platform has to keep up.

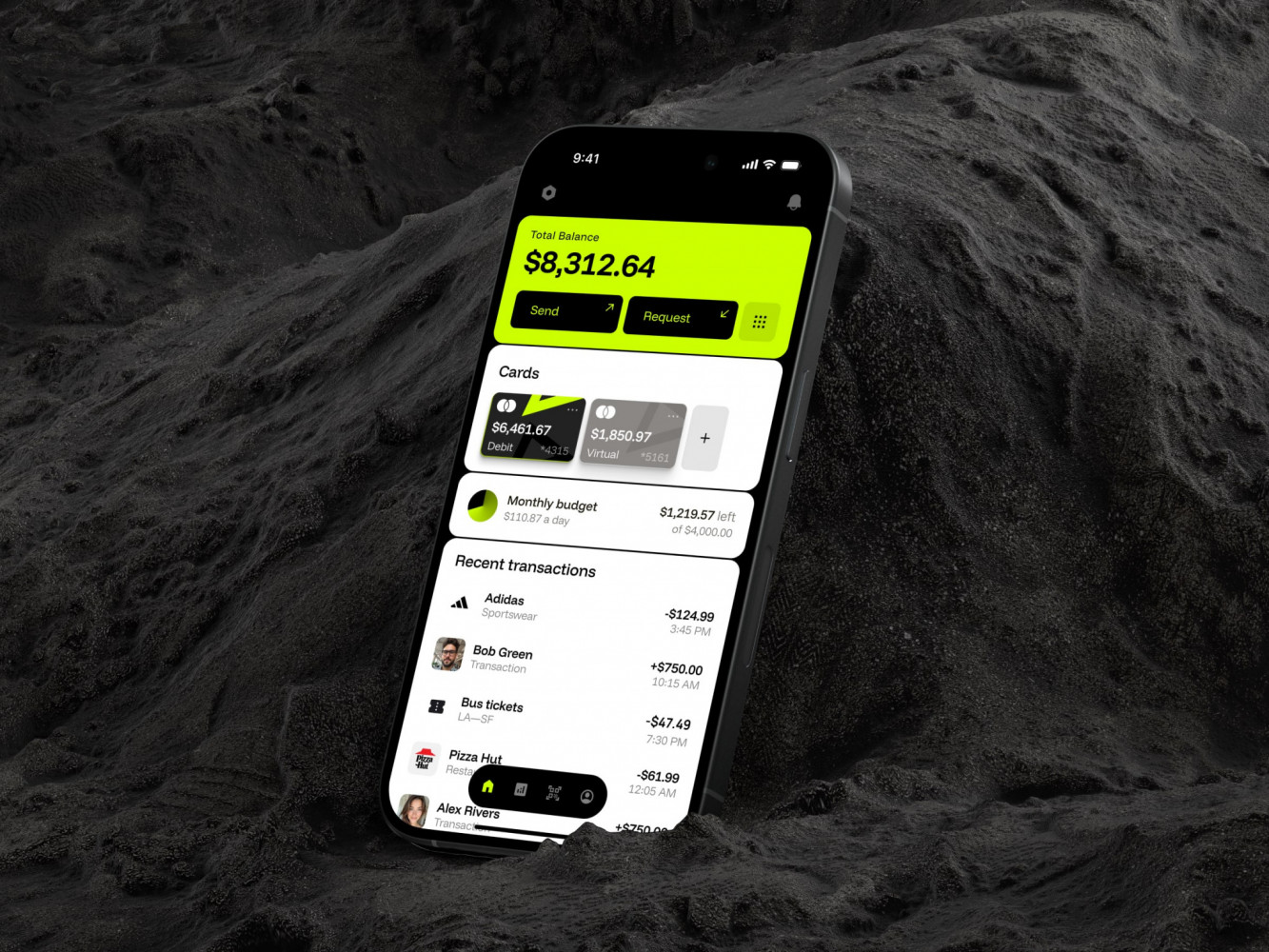

Mobile banking app by Conceptzilla

How Much Does a Digital Identity Platform Cost?

Digital identity platforms aren’t one-size-fits-all. The cost depends heavily on what you’re building, how many users you have, and how much risk you’re willing to take on yourself. A small MVP may include basic account management, one verification provider, MFA, a simple admin dashboard, audit logs, and a few integrations. That is a very different project from a national public-service identity layer or an enterprise system with federation, high availability, and complex compliance.

The main cost drivers are assurance level, number of user types, verification methods, third-party vendor fees, data storage rules, integrations, reporting, admin workflows, accessibility requirements, compliance scope, and support operations. Mobile apps add another layer. Legacy systems add another. Manual review tooling can also become bigger than expected.

In my experience, the most expensive mistake in creating a digital identity verification platform is not choosing the wrong color for a screen or even picking the wrong provider. It is starting without a clear risk model. If nobody agrees which actions require strong proof, the team ends up adding friction everywhere or trusting too much in the wrong places.

For planning, it helps to separate the work into three levels:

- MVP: account system, basic verification, MFA, admin review, logs, and one or two integrations.

- Mid-level product: stronger orchestration, risk scoring, SSO, richer dashboards, more support workflows, and analytics.

- Enterprise or government-grade system: high availability, federation, compliance reporting, accessibility, multilingual support, deep auditability, fraud operations, and careful data governance.

That is not a perfect pricing model, but it gives the conversation a better shape.

| Feature / Tier | MVP / Startup | Mid-Level / Growing Business | Enterprise / Large Scale |

| Approx. Monthly Cost | $500 – $2,500 | $3,000 – $15,000 | $20,000 – $100,000+ |

| Verification Volume | Up to 1,000 verifications/mo | 5,000 – 50,000 verifications/mo | 100,000+ verifications/mo |

| Core Features | Basic ID document scan, selfie check, simple API access | Advanced liveness detection, fraud signals, basic analytics, multiple ID types | Full biometric suite, AI-driven risk engine, custom workflows, deep analytics |

| Compliance & Support | Standard GDPR/CCPA, email support | SOC 2 Type II, dedicated account manager, SLA guarantees | ISO 27001, HIPAA/FedRAMP ready, 24/7 phone support, custom legal reviews |

| Integration Effort | Low (pre-built plugins for common stacks) | Medium (custom API integration, some dev work needed) | High (full custom integration, dedicated engineering support from vendor) |

| Best For | Early-stage fintechs, small e-commerce sites testing KYC | Scaling startups, mid-sized banks, regional government services | Global banks, large telecoms, national identity programs, big tech |

A Few Things to Watch Out For

First off, don’t just look at the sticker price. Some vendors charge per verification, others have flat fees with overage charges. If you’re expecting a viral moment or a sudden spike in sign-ups, that “cheap” MVP plan could get expensive fast. Many founders get bitten by hidden overage fees. It’s not pretty.

Second, think about the *hidden* costs. An enterprise digital identity platform might seem steep, but if it saves your team 20 hours a week in manual reviews or prevents a single major fraud incident, it pays for itself. Conversely, an MVP plan might save cash now but require your devs to build custom fraud rules later. That’s time you aren’t spending on your core product.

The biggest cost isn’t always money. It’s trust. If you pick a platform that’s clunky or fails often, your users will bounce. And losing customers is way more expensive than any subscription fee.

So, when you’re evaluating these, ask yourself: What’s my actual volume going to be in six months? Not today, but then. Because scaling pains are real, and switching providers midstream is a headache nobody wants.

Common Development Challenges

False positives are painful. A real user fails a check and feels rejected by the product. False negatives are worse. A risky user slips through. Tuning this balance is not a one-time setting. It takes monitoring, review, and sometimes uncomfortable tradeoffs.

Biometric and document checks also need care. Lighting, camera quality, document types, name formats, cultural naming patterns, and accessibility needs can all affect the flow. A system that works beautifully for one user group may frustrate another.

Privacy is another challenge. Teams often want to store everything “just in case.” I get the impulse. Data feels useful. But identity data is sensitive, and keeping more of it creates more responsibility. Collect less when you can. Protect what you keep. Delete what you no longer need.

Integrations can slow the project down too. Old systems rarely behave like neat API examples. They have missing fields, strange formats, timeout problems, and business rules hidden in someone’s memory. Build time for this. It is not pessimism. It is just Tuesday in software.

And one more point for developing a digital identity platform: account recovery deserves special attention. It is both a user support feature and an attack path. Make it too strict, and honest users get stuck. Make it too loose, and attackers smile. Neither is great.

Our Experience in Building Secure Fintech Products

For more than 19 years, we have been developing fintech products of different complexity. Here are a couple of examples.

ZAD is a Shariah-compliant investment app that combines robo-advisor and trading features. The project included risk profiling, complex financial screens, stock data, watchlists, orders, and a user experience meant to feel secure rather than intimidating. That matters for identity work because verification is not only technical. It is also psychological. If users feel lost or suspicious during onboarding, they may leave before the platform ever gets a chance to prove itself.

Symbolik Social is a financial analytics tool with social platform features where people can share their strategies and learn new things. For both professionals and beginners, the tool brings real value as they can manage their assets more efficiently. Clear UX, restructured information architecture, and solid design ensure the trust that is so much needed in the fintech industry.

I like these examples because they are not abstract. They show the ordinary work behind trustworthy platforms: clear UX, complex data, mobile and web touchpoints, integrations, and careful migration.

Silent authentication for ZAD app by Shakuro

Why Not Just Buy an Identity Vendor?

Sometimes buying is the best option. Honestly, many teams should not build document verification, biometric checks, or fraud databases from scratch. Specialized vendors exist for a reason.

But buying a vendor does not automatically give you the whole product. You may still need custom onboarding, business rules, admin dashboards, review queues, SSO integration, analytics, support tooling, migration, branding, mobile flows, or a special workflow for a specific industry. This is where custom development makes sense.

The best setup is often a mix: use proven services for specialized identity checks, then build the platform layer around your product, users, and operations. It is less glamorous than saying “we built everything ourselves,” but usually more practical.

Final Thoughts

A digital identity platform is not just a place where people log in. It is the part of the product that decides how trust works. It helps verify people, protect accounts, manage access, record consent, support audits, and keep sensitive workflows from turning into guesswork.

If you are planning one, start with risk. Then design the user journey with care. Then choose the architecture and vendors that fit the product, not the other way around. Well, you know, that really helps. The technology matters, but the shape of the service matters just as much.

And if the project already feels bigger than expected, that is normal. Identity touches more parts of a business than people think at first. Better to admit that early and build with patience.

If you are exploring a secure identity product, a government service, a fintech onboarding flow, or a platform with complex access rules, Shakuro can help with product design, web and mobile development, integrations, and long-term support.

Mobile Banking App by Conceptzilla

FAQ

What is a digital identity platform?

It is software that helps verify, authenticate, manage, and protect user identities across digital services. It usually includes proofing, login, permissions, consent, audit logs, recovery flows, and integrations.

How is a digital identity verification platform different from identity management?

Verification proves that a person is who they claim to be. Identity management controls that person’s account, access, authentication, roles, and lifecycle after the first proofing step.

What features should a digital identity platform include?

Common features include identity proofing, MFA, passkeys or passwordless login, SSO, role-based access, consent tracking, audit logs, admin dashboards, fraud checks, reporting, and support workflows.

Can government agencies use a custom identity platform?

Yes, but public-sector identity work needs careful planning around accessibility, privacy, assurance levels, legacy integrations, support, security, and compliance. A custom platform may also use existing government or third-party identity services where that makes sense.

How long does it take to build a platform like this?

A focused MVP can take a few months. A more complex enterprise or government system can take much longer, especially when it involves legacy integrations, compliance reviews, high assurance levels, or large-scale migration.