It’s one of those moments where the excitement of shipping code meets the cold, hard reality of banking regulations. You look at your roadmap, full of cool features users actually want, and then there’s this massive block labeled “KYC/AML Integration.” It feels like a speed bump made of concrete.

If you get it wrong, the fines in fintech are brutal. But if you make the process too clunky, your users bounce before they even finish signing up. It’s a tricky balance.

That’s the thing about KYC (Know Your Customer) and AML (Anti-Money Laundering) software. It looks simple on the surface—verify ID, check against lists, done. But under the hood? It’s messy. Data formats change, regulations shift depending on where your users live, and false positives can drive your support team crazy.

You might be thinking, “Can’t we just buy an off-the-shelf API?” Sure, you can. But does it fit your specific user flow? Does it handle the edge cases for your niche? Sometimes yes, sometimes no. And building it yourself? Well, that’s a whole other beast.

So, let’s cut through the noise. Whether you’re a founder trying to keep burn rate low or a product owner worried about user drop-off, this stuff matters. We’ll talk about the real pain points, the hidden costs, and how to actually approach KYC software development without losing your mind.

What Is KYC/AML Software?

When people say “KYC software,” they’re usually talking about the onboarding gatekeeper. It’s that moment when a user uploads a photo of their passport and takes a selfie. The software’s job is to answer two questions: Is this document real? And does the person holding the phone match the photo on the document? That’s identity verification. Simple enough, right? But in product terms, it’s really just data ingestion and biometric matching. You’re turning a physical human into a digital trust score.

Now, AML systems are different. They don’t care so much about who you are at the start; they care about what you do over time. If KYC is the bouncer at the club checking your ID, AML is the security camera watching to see if you’re selling illegal stuff in the bathroom. It’s a transaction. monitoring. It looks for patterns. Weird spikes in volume. Money moving to high-risk jurisdictions. Structuring deposits to avoid reporting thresholds. It’s less about a single check and more about ongoing surveillance.

Here is where KYC software development gets messy and where founders often mix up the acronyms.

KYC vs. KYB

KYC is for individuals. KYB (Know Your Business) is for companies. If you’re onboarding a freelance designer, it’s KYC. If you’re onboarding a marketing agency, it’s KYB.

KYB is harder. Much harder. With an individual, you check one ID. With a business, you have to verify the company exists, find out who owns it (the Ultimate Beneficial Owners, or UBOs), and then verify those people. It’s a rabbit hole. Some products stall for months because they underestimated how hard it is to extract ownership data from obscure corporate registries in different countries.

CDD and EDD

These aren’t separate software modules, really. They’re levels of intensity. CDD (Customer Due Diligence) is your baseline. You verify identity and understand the nature of the customer’s activities. This is what FinCEN expects as a minimum under their CDD Rule. You need to know who you’re dealing with.

EDD (Enhanced Due Diligence) is what happens when the risk meter goes up. Maybe the customer is from a high-risk country, or they’re moving huge sums. EDD means digging deeper. Source of funds. Source of wealth. Why are they doing this transaction? In product terms, EDD usually means triggering a manual review workflow. The software flags it, but a human compliance officer has to step in and ask questions. It’s a friction point, sure, but necessary.

Sanctions Screening and PEPs

Sanctions screening is checking names against lists. OFAC in the US, UN lists, and EU lists. If someone is on these lists, you generally can’t do business with them. It’s a binary check. Match or no match.

PEP (Politically Exposed Person) screening is subtler. Being a PEP isn’t illegal. But politicians, their families, and close associates are higher risk for bribery and corruption. So you flag them. You don’t reject them automatically, but you watch them closer. This ties back into EDD.

Ongoing Monitoring

This is the part most MVPs skip. They build a great onboarding flow, launch, and forget about it. But regulations—specifically the FATF (Financial Action Task Force) standards—require ongoing monitoring. FATF Recommendation 10 is pretty clear: due diligence isn’t a one-time event. You have to keep customer data updated and scan transactions continuously. If a user’s risk profile changes (say, they suddenly start receiving wires from a sanctioned entity), your system needs to catch it.

So, practically speaking?

- KYC Software: Handles ID verification, biometrics, and initial data capture.

- AML Systems: Handle transaction monitoring, rule engines, and alert generation.

- Screening Tools: Check names against sanctions and PEP lists.

- Case Management: The interface where your compliance team reviews alerts, documents decisions, and files SARs (Suspicious Activity Reports) if needed.

You can buy these as separate APIs or as a bundled suite. But they all need to talk to each other. If your KYC provider says a user is low risk, but your AML engine sees suspicious transactions, your product needs to reconcile that. Otherwise, you’re flying blind.

FinCEN’s expectations around CDD are basically about having a clear picture of who your customer is and why they’re using your service. If you can’t explain that to an examiner, you’re in trouble. It’s about having the data organized and accessible.

Risk profiling in ZAD app

Core Features of KYC/AML Software

Identity Verification and Document Checks

This is the bread and butter of KYC and AML software development. If you’re looking at KYC software, this is usually the first module you evaluate. The system needs to ingest images of passports, driver’s licenses, or national IDs. But it’s not just about reading the text via OCR (Optical Character Recognition). It has to check for forgery. Is the font right? Are the holograms reflecting light correctly? Did someone Photoshop the expiration date?

The best tools give you confidence scores. Maybe the document is real, but the image quality is poor. Your product team needs that nuance. You don’t want to auto-reject a legitimate user just because they took the photo in a dimly lit room. You want to prompt them to try again. That’s a UX detail that saves conversion rates.

Biometric/Liveness Checks

Okay, so the document is real. But is the person holding it actually the person on the ID? And are they alive? (Sounds morbid, but “presentation attacks” using masks or high-res photos are a real thing.)

Liveness detection is where the camera analyzes micro-movements. Blinking, head turns, maybe even asking the user to read a random number aloud. It’s tricky to get right. If it’s too strict, users get frustrated. Too loose, and fraudsters slip through. Modern AML/KYC tools use AI to detect depth and texture, ensuring it’s a 3D face and not a 2D screen. It feels a bit invasive to users sometimes, so how you frame this in your UI matters. Tell them why you’re asking them to blink. It builds trust.

KYB and Beneficial Ownership Verification

As I mentioned before, KYB is the hard part. When you’re onboarding a business, you can’t just verify one person. You need to map out the corporate structure. Who owns more than 25%? Who has control?

Good Know Your Customer software connects to global registries to pull this data automatically. But let’s be real—data quality varies wildly. In some countries, the registries are digital and clean. In others, you’re dealing with scanned PDFs from 1998. The software needs to handle this mess. It should flag Ultimate Beneficial Owners (UBOs) and then run them through the same KYC checks. It’s a nested process. If your tool can’t handle multi-layered ownership structures, you’re going to end up doing a lot of manual digging. And nobody wants that.

Risk Scoring

You can’t treat every customer the same. A local teacher opening a savings account is different from a crypto exchange moving millions across borders. Risk scoring engines take all the data points—location, industry, transaction volume, and PEP status—and spit out a number. Low, medium, high.

This score drives everything else. Low risk? Auto-approve. High risk? Trigger EDD. The key here is transparency. Your compliance team needs to understand why a score was assigned. If the black box says “high risk” but doesn’t tell you why, it’s useless. You need explainable AI. Otherwise, you can’t defend your decisions to regulators.

Sanctions, PEP, and watchlist screening

This is the non-negotiable part. You have to check names against lists. OFAC, UN, EU, HMT. And PEP lists. The software needs to do fuzzy matching. Because criminals rarely spell their names exactly as they appear on the list. They use aliases, nicknames, or slight misspellings.

If your AML/KYC tools only do exact matches, you’re vulnerable. But if it’s too sensitive, you’ll get thousands of false positives. Your compliance team will drown in alerts. Tuning this engine is an art. You want to catch the bad guys without flagging every “John Smith” in your database. It’s a constant balancing act.

Transaction Monitoring and Suspicious Activity Alerts

KYC gets them in the door. AML keeps watch while they’re inside. This module looks at behavior. Is there a sudden spike in volume? Are funds moving in circular patterns? Are they structuring deposits to stay under reporting limits?

The software uses rules and machine learning models to detect these anomalies. When something looks off, it generates an alert. But here’s the thing: most alerts are false alarms. The system needs to be smart enough to prioritize. Not all alerts are created equal. A $10,000 transfer to a high-risk country is more urgent than a $50 coffee purchase. Your system should reflect that priority.

Case Management Dashboard

When an alert fires, where does it go? Into an email inbox? God forbid. You need a centralized case management dashboard. This is where your compliance officers live. They need to see the alert, the user’s profile, their transaction history, and any previous notes—all in one place.

They need to be able to add comments, upload additional documents, and make a decision: dismiss, escalate, or file a SAR. Workflow automation helps here. If a junior analyst dismisses a case, maybe a senior needs to approve it. If it’s a clear false positive, maybe it’s auto-closed. The dashboard should reduce clicks, not add them. Time is money in compliance.

Audit Logs and Compliance Reporting

Finally, the boring but critical part. Auditors love paper trails. Every action taken in the system—who viewed what, who changed a risk score, who approved a transaction—needs to be logged. Immutable logs.

And when regulators ask for reports, you shouldn’t have to spend weeks pulling data from spreadsheets. The software should generate standard reports (like SARs or CTRs) with a few clicks. If you can’t prove you did your due diligence, you’re liable. So, make sure your KYC software keeps a meticulous diary. You’ll thank yourself later when the examiners come knocking.

ZAD app by Shakuro

KYC/AML Software Architecture

The Frontend: Where Trust is Built (or Broken)

KYC software development starts with the user. The onboarding flow needs to be frictionless. If it takes ten minutes and five page reloads, you’ve lost them. Modern architectures use lightweight SDKs or embedded widgets that handle the heavy lifting—camera access, image capture, and liveness checks—right in the browser or app. But here’s the trick: the frontend shouldn’t make the final decision. It just collects data and sends it off. It’s a dumb terminal, essentially. Smart UI, dumb logic. That keeps it secure and fast.

Then there’s the admin side. Your compliance team needs a dashboard that doesn’t look like it was built in 2005. It needs to be responsive, clear, and fast. They’re juggling hundreds of cases; they don’t have time for laggy interfaces. This part of the architecture is usually a separate single-page application (SPA) that talks to your backend APIs.

The Middleware: The Brain and the Bouncer

This is where the magic happens. You’re not building everything from scratch. You’re likely integrating with verification providers—companies that specialize in document checks or biometrics. Your architecture needs to be API-first here. You send a request, they send back a result. But what if their API goes down? What if it’s slow?

This is why I’m a big fan of event-driven architecture. Instead of waiting for a synchronous response, you drop an event into a queue. “User submitted ID.” Then, a worker picks it up, calls the provider, gets the result, and updates the database. It decouples your system. If the verification provider is having a bad day, your app doesn’t crash. It just waits. Queue-based processing is a lifesaver for scalability. You can spike to thousands of signups on a Monday morning, and the queue just absorbs the load.

Inside this middleware, you have two critical components: the rules engine and the risk scoring model.

The rules engine is deterministic. If X happens, do Y. “If country is North Korea, block.” Simple. But the risk-scoring model is probabilistic. It uses machine learning to weigh dozens of factors. Is this IP address suspicious? Has this device been used for fraud before? These two need to work together. The rules engine might flag something immediately, while the risk model provides a nuanced score over time.

Transaction Monitoring: The Pipeline

For AML software development, you’re dealing with streams of data. Every transaction is an event. You can’t process these one by one in real-time without slowing everything down. So, you build a pipeline. Transactions flow in, get enriched with customer data (from your KYC store), run through monitoring rules, and then either pass or generate an alert.

This needs to be fast. Really fast. If a fraudulent transaction slips through because your pipeline was backed up, that’s on you. Technologies like Kafka or Kinesis are common here. They handle high-throughput data streams efficiently. It’s not just about storing data; it’s about moving it quickly so you can act on it.

Data Storage and Security: The Vault

Now, let’s talk about where you put all this sensitive info. Passports, selfies, financial records. This isn’t just any data; it’s PII (Personally Identifiable Information) and financial data. You need encryption at rest and in transit. No exceptions.

But encryption isn’t enough. You need strict access control. Who can see a user’s passport? Only specific compliance officers, and only when they’re working on a case. Role-Based Access Control (RBAC) is standard, but Attribute-Based Access Control (ABAC) is better. It allows for finer-grained permissions. “Can view if risk level is high AND assigned to my team.”

And don’t forget audit trails. Every single access, every view, every change needs to be logged. Not just for compliance, but for security. If someone’s data leaks, you need to know exactly who touched it last. Immutable logs are key here. Once written, they can’t be changed.

Observability: Keeping the Lights On

Finally, how do you know if it’s working? You need observability. Not just basic logging, but metrics and tracing. How long does a verification take? What’s the false positive rate on your AML alerts? Are there errors in the queue?

In a distributed system like this, things break. APIs timeout. Queues get stuck. You need dashboards that show you the health of the entire system in real-time. If your verification provider’s latency spikes, you need to know before your support team gets flooded with tickets.

Putting It All Together

So, you’ve got a frontend that captures data, an event-driven backend that processes it asynchronously, a rules engine and ML model that assess risk, a streaming pipeline for transactions, and a secure vault for data. All tied together with robust APIs.

KYC software development sounds complicated because it is. But when it works, it’s invisible. The user signs up smoothly, the compliance team manages risks efficiently, and the regulators are happy. Well, as happy as regulators ever get.

Getting the architecture right from day one saves you so much pain later. Refactoring a KYC system while under regulatory scrutiny? Not fun.

Symbolik case by Shakuro

The KYC/AML Software Development Process

Every company has its own way of building, but the process usually follows a few practical stages.

1. Compliance Discovery and Risk Mapping

Before design or code, the team needs to understand the product model. Who are the users? Which countries are involved? What money movement exists? Are there personal customers, business customers, or both? What are the regulatory obligations? What risks are most likely?

This stage should involve product, compliance, engineering, legal, operations, and sometimes support. Yes, that is a lot of people in one room. But it is cheaper than discovering in month four that your onboarding flow does not collect a field the compliance team needs.

2. UX/UI Design for Onboarding

The onboarding flow should feel clear and calm. Ask for the minimum needed at each step. Explain why sensitive information is required. Show progress. Give useful retry instructions. Save partially completed flows when possible.

This is where design work really helps. A small change in copy, field order, or photo guidance can reduce drop-offs. It is not glamorous work, maybe, but it pays back.

3. Architecture and Vendor Selection

Most teams will use third-party services for at least part of the KYC/AML stack. The question is not “vendor or custom” so much as “which parts should be vendor-based, and where do we need control?”

Identity verification, document checks, sanctions lists, business registries, and biometric checks are often vendor-backed. The custom layer usually handles orchestration, business logic, user experience, internal review, reporting, and integration with the core product.

4. Core Development

This is where the product becomes real: onboarding forms, backend APIs, provider integrations, risk scoring, admin panels, case queues, document storage, permissions, notification logic, and logs.

For KYC software development services, the difference between a decent implementation and a painful one often shows up in edge cases. What happens when a provider is down? What if a user has two documents? Can a reviewer override a decision? Is the reason captured? Can support see enough to help, but not too much sensitive data?

Small questions. Big consequences.

5. Testing and Validation

Testing KYC/AML software is not only “does the button work?” You need to test provider failures, duplicate users, manual review states, permissions, audit log integrity, document upload limits, risk rule changes, and reporting exports.

Security testing also matters. Access control bugs in admin tools can be nasty. Data retention and deletion flows should be checked carefully. And if you use biometric data, be extra cautious about storage and permissions.

6. Launch, Monitor, Improve

After launch, the system needs monitoring. Approval rates, rejection reasons, false positives, manual review time, provider errors, customer drop-off, and alert volume should be watched closely.

The first few weeks can be a little uncomfortable. Real users have a talent for finding cases nobody wrote in the spec. You adjust, fix, and tune, and gradually the system gets steadier.

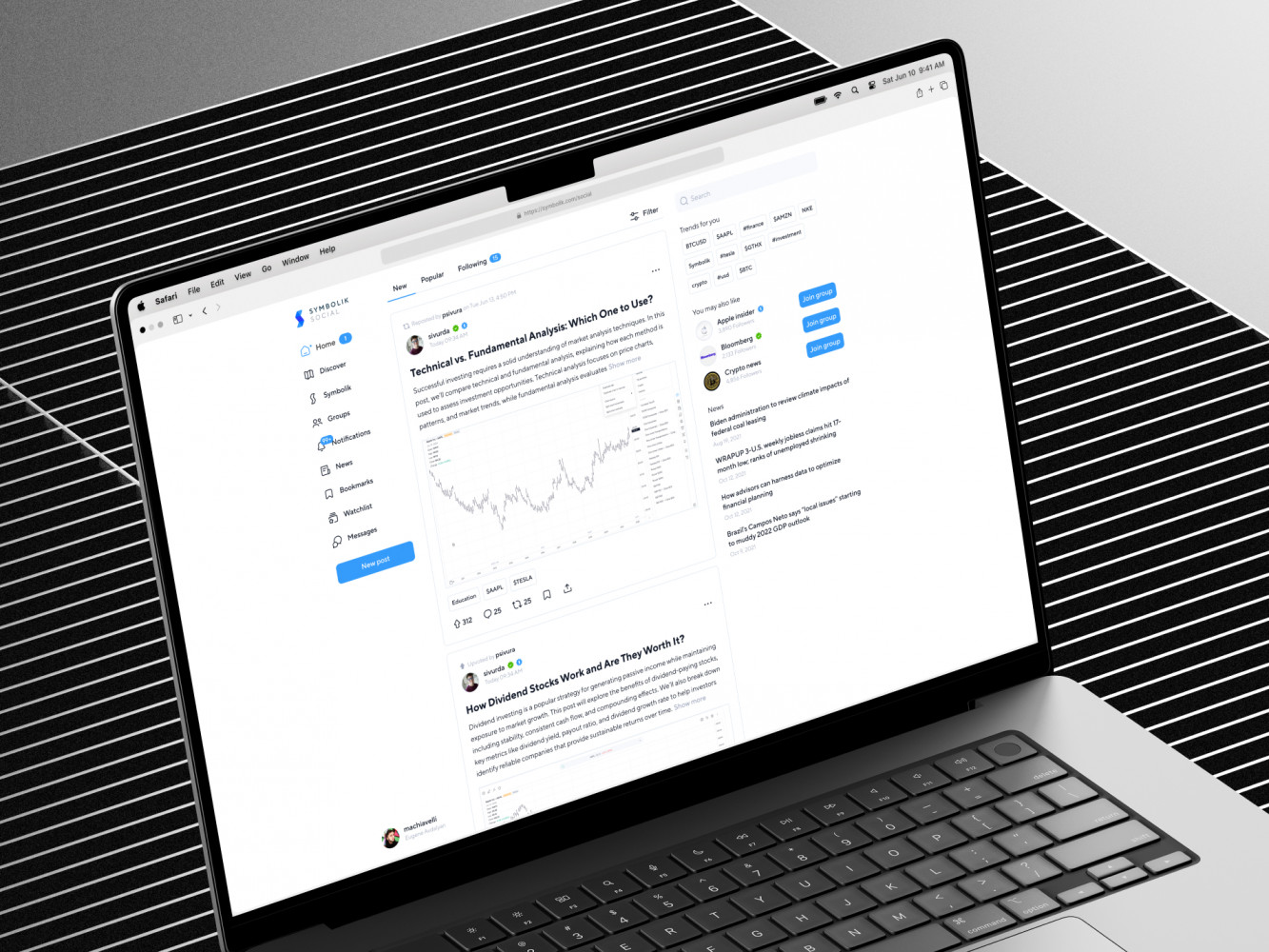

TraderTale: Social Platform for Traders by Shakuro

Build vs. Buy: Which Option Makes Sense?

For KYC software development, there is no single right answer.

Buying a ready-made tool can be the best option if your workflow is standard, your market is narrow, and you need to launch quickly. Many vendors already cover document verification, sanctions screening, and basic AML checks. Why rebuild that from scratch?

Custom development makes more sense when your product has special risk logic, multiple jurisdictions, a complex onboarding path, high review volume, or unusual integrations. It also helps when compliance work needs to connect tightly with your core product experience.

Most serious fintech products land somewhere in the middle. They use vendors for data and checks, then build a custom layer for user flow, risk orchestration, case management, analytics, and internal operations.

That hybrid approach is often the best option. Not always, but often.

How Much Does KYC/AML Software Development Cost?

Costs vary a lot, because the scope can be small or huge.

An MVP might include basic customer onboarding, document verification through a provider, simple sanctions screening, admin review, and audit logs. That can be enough for an early-stage product proving its model.

A mid-level platform may add business verification, configurable risk rules, richer case management, reporting, multiple roles, support workflows, and better analytics.

An enterprise-grade system can include multi-region compliance logic, transaction monitoring at scale, advanced alerting, data pipelines, complex permissions, provider redundancy, custom risk models, periodic reviews, and regulator-ready exports.

The biggest cost drivers in KYC software development are usually integrations, compliance complexity, manual review workflows, transaction monitoring, security requirements, and the number of user types. Another quiet cost driver is change. Compliance rules and business requirements move, so the system should be easy to adjust without making engineers nervous every time a threshold changes.

| Feature / Component | MVP (Minimum Viable Product) | Mid-Level Platform | Enterprise Grade |

| Estimated Cost Range | $50k – $150k | $200k – $600k | $1M+ |

| Timeline | 3 – 6 months | 6 – 12 months | 12 – 24+ months |

| Core Scope | Basic ID verification, simple sanctions check, manual review dashboard. | Automated risk scoring, KYB support, transaction monitoring rules, case management. | Full AI/ML models, global coverage, complex workflows, high-volume processing. |

| Verification Providers | 1–2 basic APIs (e.g., document + selfie). | Multiple providers for redundancy, biometric liveness, KYB data sources. | Global network of providers, fallback logic, custom integrations with local registries. |

| Risk Engine | Simple rule-based (if/then). | Hybrid: Rules + basic ML scoring. | Advanced ML models, behavioral analytics, dynamic risk adjustment. |

| Transaction Monitoring | None or very basic static rules. | Real-time streaming, pattern detection, alert prioritization. | Complex network analysis, cross-border tracking, AI-driven anomaly detection. |

| Compliance & Reporting | Basic audit logs, manual SAR filing. | Automated reporting templates, role-based access control. | Full regulatory reporting suite, immutable audit trails, real-time compliance dashboards. |

| Infrastructure | Cloud-hosted, standard security. | Scalable cloud architecture, encryption at rest/transit, RBAC. | Multi-region deployment, disaster recovery, zero-trust security, dedicated compliance environments. |

| Team Size | Small team (2-4 devs, 1 PM). | Medium team (6-10 devs, QA, DevOps, Compliance expert). | Large team (15+ devs, data scientists, security engineers, legal/compliance officers). |

Remember, these numbers are for development. They don’t include:

- Vendor Fees: Every time you verify an ID, you pay a provider. That adds up fast.

- Compliance Staff: You still need humans to review alerts and manage the system.

- Legal Advice: Getting your policies right isn’t cheap.

- Maintenance: Software rots. Regulations change. You’ll spend 20-30% of your initial build cost annually just keeping it current.

So, when you’re budgeting, don’t just look at the dev bill. Look at the total cost of ownership. It’s a marathon, not a sprint.

Common Challenges in AML/KYC Development

The first challenge is false positives. If your system flags too much, reviewers drown in alerts and important cases get buried. If it flags too little, well, that is worse. Tuning this balance takes data and patience.

The second challenge is user friction. Every extra field, scan, retry, and waiting screen can reduce conversion. Sometimes that friction is necessary. Sometimes it is just a product team being overly cautious. The hard part is knowing the difference.

Data quality is another headache. Names, addresses, documents, registry data, and transaction histories do not always arrive clean. International products face extra fun here because formats, alphabets, and document types vary widely.

Then there is vendor dependency. Third-party verification providers can be excellent, but your product should not fall apart when one API slows down. Timeouts, retries, fallback states, and clear internal messages save a lot of stress.

Privacy is its own serious topic. KYC data is not casual analytics data. It needs strict access control, retention policies, encryption, and careful logging. You do not want sensitive identity details sprinkled through random support tools or debugging logs. Trust me, cleaning that up later is not a pleasant afternoon.

Abyss Crypto Management App by Conceptzilla

How to Choose KYC Software Development Companies

When comparing KYC software development companies, do not look only at polished case studies and hourly rates. Look for practical experience with regulated products, sensitive data, complex integrations, and admin workflows.

A good team should ask uncomfortable but useful questions early. Which customers are high risk? What review decisions need audit logs? Who can override an automated rejection? What happens if a vendor returns conflicting results? How will compliance update risk rules later?

You also want strong UX thinking. Compliance software is not just backend logic. The customer-facing flow matters, and the internal dashboard matters just as much. Reviewers need clarity, not a wall of raw JSON.

Technical maturity matters too: secure architecture, API design, testing, observability, access control, and post-launch support. If a team treats KYC as “just another form,” that is a warning sign.

Our Experience in KYC/AML Software Development

We have worked on several finance-related products where trust, data clarity, and careful UX mattered a lot.

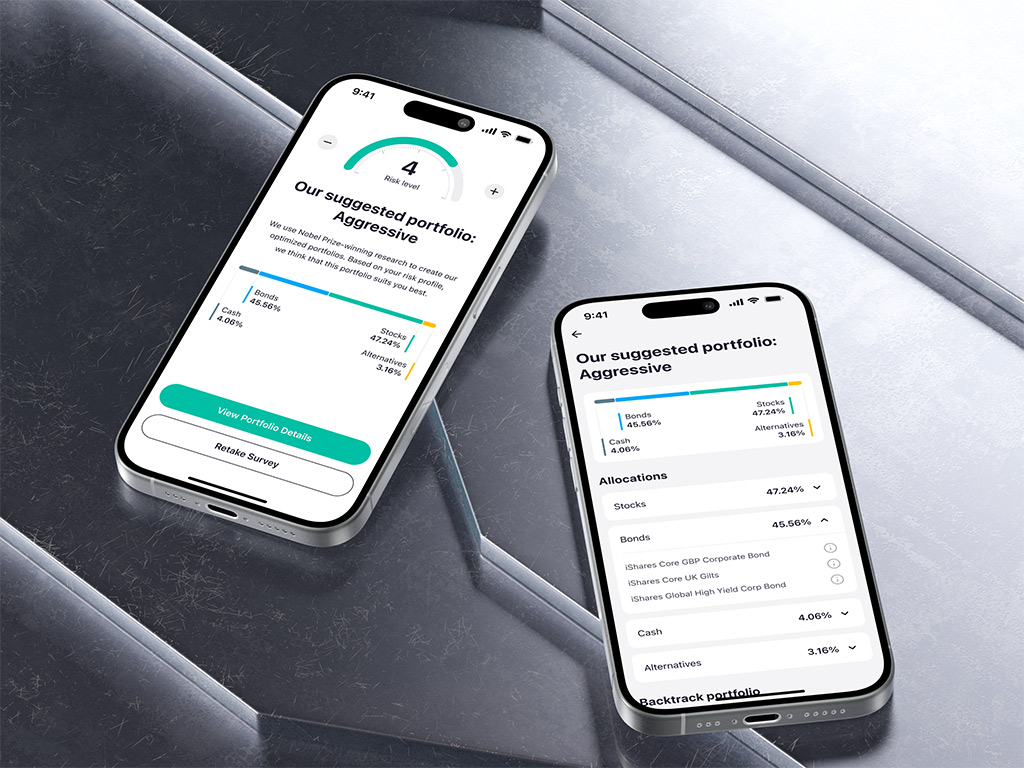

For example, ZAD, a mobile investment platform combining robo-advisor and trading features with Shariah-compliant financial flows. The product included risk profiling, trading screens, watchlists, portfolios, alerts, and a lot of financial data packed into a mobile interface. KYC/AML products have a similar design problem: serious information, high stakes, and users who still need the app to feel understandable.

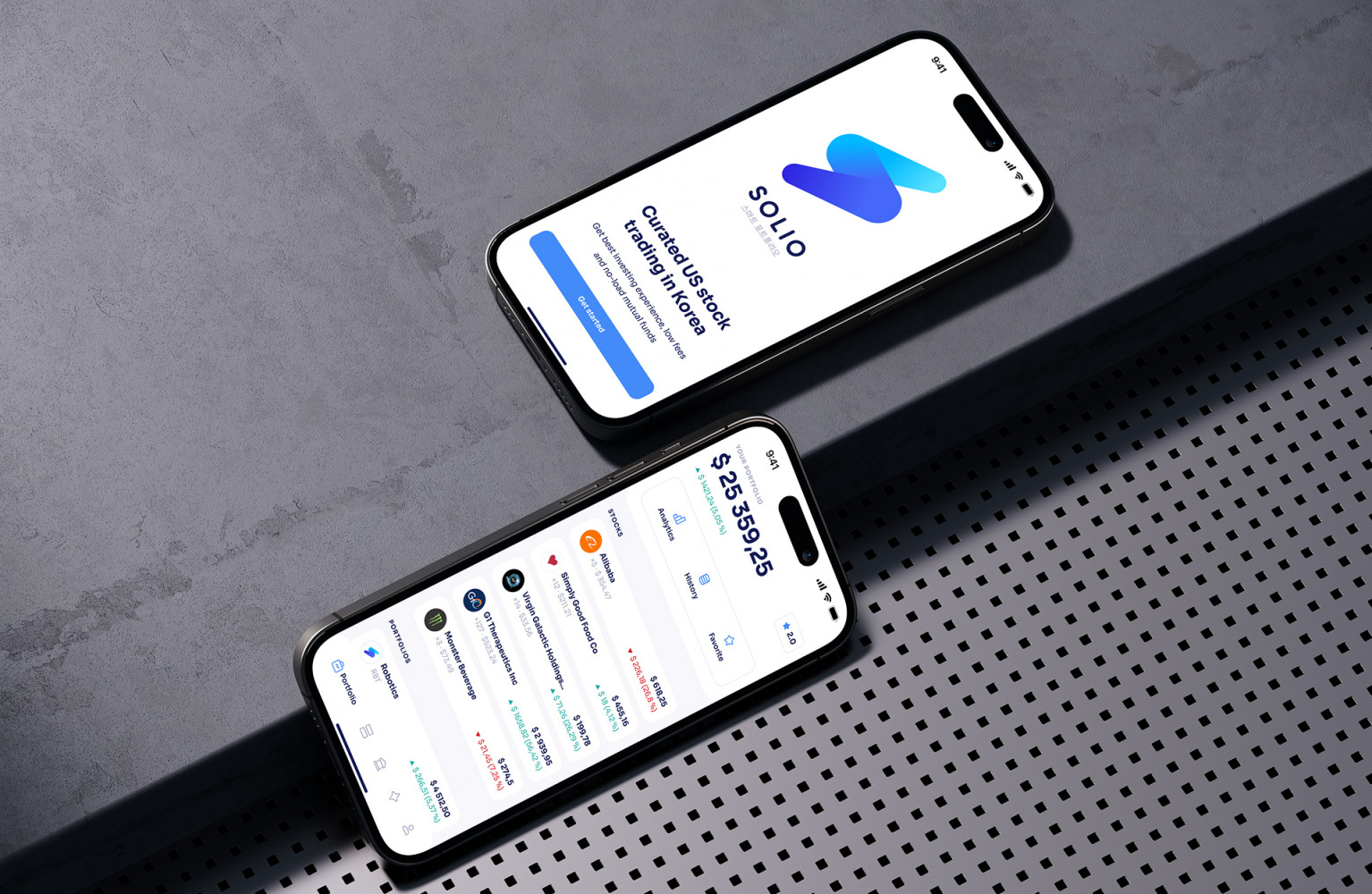

Another example is Solio, a Korean stock trading app. Here, not only did we have to follow KYC/AML standards but also adhere to local market requirements. Also, the target audience were beginners and your people who had little experience in stock trading. They needed a keen balance between usability and regulations. It shows the kind of work that matters in this space: data-heavy interfaces, fintech context, and product design for people who know exactly what they need.

Compliance tools benefit from the same habits: clear information architecture, careful workflows, scalable web and mobile development, and design that respects both experts and everyday users.

Solio App by Shakuro

Final Thoughts

KYC software development is one of those product areas where boring details are actually important. A missing audit log, a vague rejection reason, a weak admin permission model, or a poorly tuned alert rule can create real problems later.

At the same time, this software should not feel like punishment for the user. The best systems make the necessary checks feel calm, understandable, and as short as possible. You agree, that sounds good, doesn’t it?

If you are planning AML software development for a fintech, lending, payments, crypto, marketplace, or investment product, start with the risk model and user journey. Then choose the right mix of vendor tools and custom development. Keep compliance people close to the product team. And please, test the weird cases. The weird cases always show up.

Shakuro can help design and build custom KYC/AML flows, internal dashboards, fintech mobile apps, and web platforms where security and usability both matter.

FAQ

What is KYC Software Development?

It is the process of building tools that verify customer identity, collect required information, screen users against risk sources, support manual review, and store compliance records. In many products, it also includes business verification, beneficial ownership checks, and ongoing monitoring.

What Features Should AML/KYC Tools Include?

Common features include identity verification, document checks, biometric checks, KYB, sanctions and PEP screening, risk scoring, transaction monitoring, case management, audit logs, reporting, and role-based access control.

How Long Does KYC/AML Software Development Take?

A simple MVP can take a few months if the scope is narrow and third-party providers cover most checks. A more complete platform with transaction monitoring, KYB, detailed dashboards, and multi-region workflows can take longer. The honest answer is: it depends on risk, integrations, and how much internal workflow you need.

Should We Build Custom KYC Software or Use a Vendor?

For many teams, the best route is a mix. Use vendors for document verification, screening data, and specialized checks, then build a custom layer for onboarding UX, risk logic, case management, analytics, and product-specific workflows.

How Do KYC Software Development Services Support Compliance Teams?

They turn compliance requirements into usable product flows and internal tools. That means clearer review queues, better audit trails, faster investigations, safer data handling, and fewer manual steps. Well, when built properly, at least. The process still needs good compliance input from the company itself.