Fraud is one of those problems that looks simple from far away. A suspicious payment comes in, the system blocks it, and everyone moves on. Nice and clean.

Then you start building the actual product and, well, it gets messy fast.

A customer buys a gift card while traveling. A loyal user changes phones. A new merchant receives a sudden spike in orders after a TikTok post. Are these normal events, or are they signs of abuse? That is the uncomfortable little space where fraud detection software has to work every day.

So here’s the dilemma many founders and product owners face right when creating fraud detection software. Do you buy an off-the-shelf solution? Sure, it’s faster, but then you’re stuck with their black box algorithms, paying per API call, and hoping their model understands your specific niche quirks. Or do you build it in-house? That gives you control, sure, but the complexity is staggering.

In this article, I want to walk you through what actually matters when evaluating or building fraud detection systems. Just the real talk about what works, what’s a waste of money, and how to stop letting the bad guys win without turning your checkout flow into a fortress that no one can get through.

What Is Fraud Detection Software?

Fraud detection software is a system that watches digital activity and flags behavior that looks risky. It can monitor payments, logins, account changes, device signals, location patterns, marketplace activity, promo code use, or anything else that might show suspicious intent.

In plain English, it helps answer one question: does this action look safe enough to allow?

That answer is rarely a simple yes or no. A good fraud platform usually gives a risk score, explains the reason behind it, and sends questionable cases to a human review flow. Some actions can be blocked automatically. Others need a softer response, like asking for extra verification or limiting part of the transaction.

It is also worth separating three phrases that often get mixed together.

Fraud detection tools identify suspicious activity. Prevention software tries to stop damage before it happens. Compliance monitoring checks whether activity fits legal, regulatory, or internal policy requirements. They overlap, of course, because real products are not neatly labeled boxes. But the distinction matters when planning a system.

If you only build detection, your team may still spend too much time cleaning up losses after the fact. If you only build prevention, you may block good users and quietly hurt revenue. The best option usually sits somewhere in the middle.

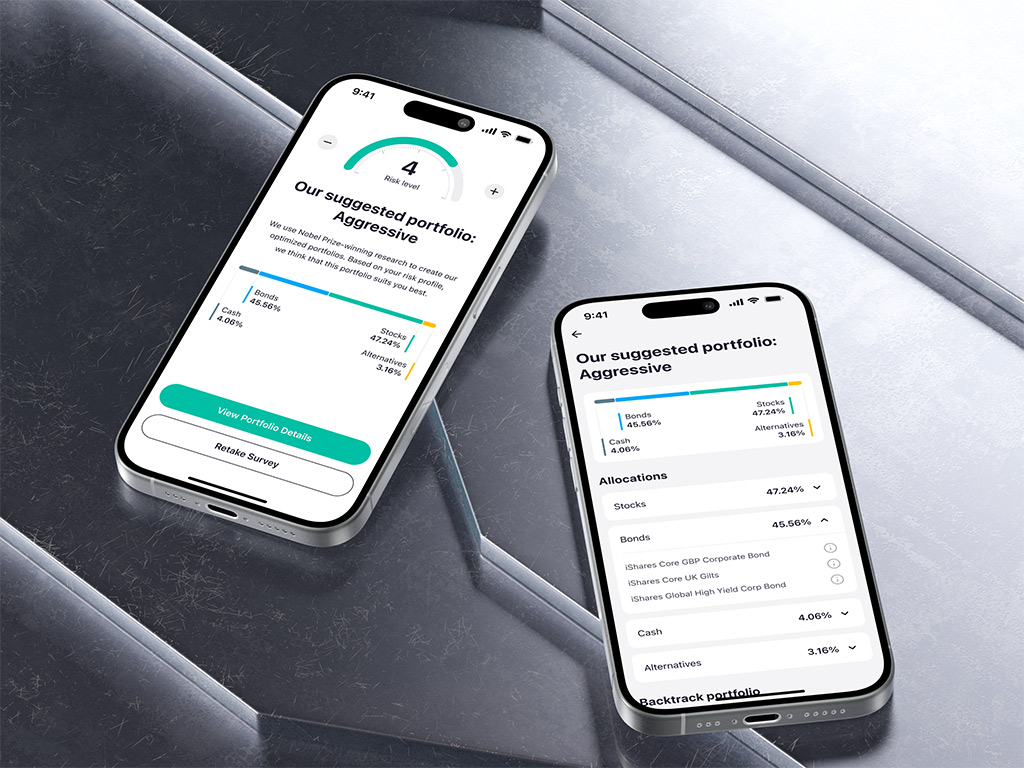

Risk profiling in ZAD app

Why Businesses Need Fraud Detection Software

Fraud hurts more than the balance sheet. That sounds a bit dramatic, but it is true.

There are direct losses: stolen funds, chargebacks, refunds, bonuses abused by fake accounts, inventory shipped to bad actors. But there are also the softer costs. Support teams spend hours explaining locked accounts. Product managers argue with risk teams about conversion drops. Marketing campaigns get distorted by fake signups. Real users start feeling watched or distrusted.

For fintech products, fraud can threaten the whole operating model. For ecommerce, it eats margins that were already thin. For SaaS platforms, account takeover can lead to data exposure and churn. Marketplaces have their own flavor of trouble: seller fraud, buyer fraud, collusion, fake reviews, refund abuse. It is a surprisingly creative area, and not in a fun way.

In my experience, the hardest part is not spotting the obvious scam. A stolen card used ten times in five minutes from different locations is not exactly subtle. The hard part is catching the gray-area behavior without making normal customers feel like they are passing airport security just to buy socks.

That is why a product approach to creating fraud prevention software matters. Fraud detection should not be treated as a hidden backend script. It needs thoughtful user flows, admin tools, reporting, escalation paths, and a clear idea of what happens when the system is unsure.

Core Features of Fraud Detection Software

Most fraud products start with a few simple rules. That is fine. Honestly, rules are underrated when they are used carefully. The trouble begins when the product grows and the rule list turns into a museum of old incidents nobody remembers.

Here are the features that usually matter.

Real-time Transaction Monitoring

Real-time monitoring checks events as they happen. In payment fraud detection software, that might mean scoring a card transaction before approval. In a marketplace, it could mean reviewing a seller payout request. In a SaaS product, it may be a suspicious login or a sudden permission change.

Speed matters here. If the decision takes too long, the product feels broken. If the decision is too shallow, fraud slips through. So the system has to be quick, but not dumb. A lovely engineering headache.

Risk Scoring

Risk scoring turns many signals into one decision-friendly number or level. For example, a transaction may be low, medium, or high risk based on amount, device, user history, IP address, behavior pattern, and past disputes.

A score alone is not enough, though. Reviewers need to know why something was flagged. “High risk” is not very helpful when a support agent has a frustrated customer on the line.

Rules Engine

A rules engine lets teams define conditions without redeploying code every time. For example:

- Block withdrawals above a certain amount from newly created accounts.

- Send first-time international orders to review.

- Ask for verification when a login comes from a new device and a high-risk location.

The trick is governance. Someone has to own the rules, test them, retire stale ones, and check whether they are hurting legitimate users. It is a little annoying, but you get used to it over time.

Machine Learning and Anomaly Detection

Machine learning fraud detection can find patterns that are too complex for manual rules. It can learn from historical transactions, user behavior, known fraud cases, and feedback from reviewers.

This really helps when fraud patterns shift. But models are not magic. They need data quality, monitoring, retraining, and a way for humans to understand their output. Otherwise, the model becomes a mysterious box that everyone fears but nobody trusts.

User Behavior Analytics

Behavior tells interesting stories. How fast does a user complete checkout? Do they paste data into every field? Are they switching addresses, cards, and devices in unusual combinations? Have they used the product before, or did they appear five minutes ago with perfect confidence and a very expensive order?

None of these signals proves fraud by itself. Together, they can paint a useful picture.

Device and Identity Signals

Device fingerprinting, IP intelligence, email reputation, phone verification, KYC checks, and document verification can all support online fraud detection. The important word is support. Identity checks are not a silver bullet, and too much friction can push away good users.

Many teams get excited about adding more verification steps, then act surprised when conversion drops. Users do not care that the risk model needed one more signal. They just know the product suddenly feels harder to use.

Alerts and Case Management

A fraud alert without a workflow is just noise. For transaction fraud detection, reviewers need queues, filters, evidence, notes, status labels, assignment rules, escalation, and audit history. If your team is handling reviews in spreadsheets, that may work for a short while, but it will start creaking.

Good case management also improves the model because review decisions become feedback. This is where the system starts learning from the people using it.

Dashboards and Reporting

Dashboards should show more than blocked fraud. They should help teams understand false positives, approval rates, review volume, loss trends, rule performance, chargebacks, and user friction.

A dashboard that only says “we blocked 1,000 risky actions” can feel satisfying. But what if 400 of them were good customers? That is the number people need to see too.

Integrations

Fraud systems rarely live alone. They connect to payment processors, KYC vendors, CRM tools, customer support systems, data warehouses, analytics platforms, admin panels, and sometimes law enforcement reporting flows.

The integration layer is not glamorous, but it often decides whether the product works in real life.

ZAD app by Shakuro

How AI and Machine Learning Improve Fraud Detection

AI fraud detection is useful because fraud is dynamic. Attackers test systems. They adapt. They notice when a rule blocks one pattern and then they try another.

Machine learning can help with several things:

- Finding unusual patterns across large datasets.

- Predicting risk based on past confirmed fraud.

- Grouping related accounts or transactions.

- Reducing false positives by learning what normal behavior looks like.

- Prioritizing review queues so humans see the riskiest cases first.

Graph-based approaches can be especially useful. Fraud often moves through networks: shared devices, repeated addresses, linked cards, common payout accounts, overlapping behavior. Looking at one transaction may not reveal much. Looking at the network around it can be a different story.

Still, I would be careful with any claim that AI will “solve fraud.” It will not. It can make the system sharper, faster, and more adaptive, but fraud detection is still a product and operations problem. Someone has to review edge cases. Someone has to tune thresholds. Someone has to ask, “Are we blocking the people we actually want to keep?”

Fraud Detection Software Architecture

Fraud detection software usually has several layers. The exact shape depends on the business, but the bones are fairly consistent.

First, there is data ingestion. The system collects events from product flows, payment systems, login services, user profiles, device tools, and third-party providers. In a busy product, this might require streaming infrastructure so events can be processed quickly.

Then comes storage. You may need a transactional database for live decisions, a warehouse for analytics, and a feature store for machine learning. Some teams start smaller, and that is fine, but the architecture should not trap them later.

Next is the decision layer. This includes the rules engine, model service, risk scoring API, and business logic for what happens after a score is produced. Approve, block, review, step-up verification, delay payout, limit account activity. Those choices should be explicit.

The admin layer is where humans enter the picture. Reviewers need dashboards, case queues, notes, decision history, permissions, and audit logs. Managers need reports and rule performance views. Engineers need monitoring.

Security sits across all of this. Fraud systems handle sensitive data, so access control, encryption, logging, retention policies, and privacy rules cannot be added casually at the end. Well, they can, but everyone will regret it.

Fraud Detection Software Development Process

Building fraud detection software is not just a coding task. It is part product strategy, part data work, part risk management, and part UX design.

1. Discovery and Risk Mapping

Start by mapping the fraud patterns that matter most. Payment fraud? Account takeover? Fake sellers? Bonus abuse? Refund fraud? Internal abuse? It is tempting to say “all of them,” but focus helps.

The team should also define what success means. Lower chargebacks, fewer manual reviews, faster approvals, better detection, a lower loss rate, and less user friction. These goals can conflict, so it is better to talk about them early.

2. Data Source Audit

Fraud prevention software is only as good as the signals it receives. Product events, payments, account history, device data, support tickets, dispute outcomes, KYC results, and manual review decisions all matter.

This is often where projects slow down. Data exists, but it is scattered. Labels are inconsistent. Past decisions were not recorded cleanly. Nobody loves this part, but it is where the real foundation gets built.

3. UX and Workflow Design

Fraud teams need interfaces they can actually use under pressure. A reviewer should not have to open six tabs to understand why an account was flagged. Product users also need thoughtful flows when verification is required.

Small UX details matter here. The wording of a verification message can change whether a good customer stays calm or gets annoyed and leaves.

4. Architecture Planning

The team defines event flow, scoring logic, databases, APIs, integrations, permissions, security rules, and monitoring. This is also the point to decide whether the MVP needs machine learning or whether rules plus analytics are enough at first.

Often, rules are the better starting point. Not forever. Just long enough to collect cleaner data and understand the business patterns.

5. Core Development

An MVP might include event tracking, a rules engine, risk scoring, alerts, a review dashboard, user actions, audit logs, and basic reporting. For some businesses, that already creates a lot of value.

The product should be built so it can grow into more advanced transaction fraud detection later, including model services and deeper analytics.

6. Integrations

Payment processors, KYC tools, email reputation services, device intelligence, customer support platforms, data warehouses. This part can be more time-consuming than expected because every vendor has its own quirks.

By the way, integration quality affects trust. If dispute data arrives late or event fields are inconsistent, the system may learn the wrong lessons.

7. Testing and Validation

Fraud systems need functional testing, security testing, load testing, and decision testing. Teams should simulate normal users, suspicious users, edge cases, and high-volume traffic.

For machine learning models, validation means checking precision, recall, false positives, drift, and how decisions perform across user groups. It is not just “the model score looks good.”

8. Launch and Continuous Improvement

After launch, the work continues. Fraud patterns change, rules age, models drift, products add features, and attackers poke around. Monitoring and iteration are part of the product, not an optional maintenance chore.

TraderTale: Social Platform for Traders by Shakuro

How Much Does Fraud Detection Software Cost?

There is no honest single price for custom fraud software. Anyone who gives one without asking questions is probably guessing.

A focused MVP can be relatively contained if it includes rules, scoring, basic alerts, a review dashboard, and a few integrations. A mid-level product costs more because it adds richer workflows, better reporting, more data sources, and stronger security. Enterprise systems can get expensive because they need real-time processing at scale, machine learning, compliance controls, complex permissions, and support for multiple teams or markets.

The main cost drivers are:

- Number and quality of data sources.

- Real-time decision requirements.

- Payment, KYC, and internal tool integrations.

- Admin dashboard complexity.

- Machine learning scope.

- Security and compliance requirements.

- Review workflows and reporting.

- Volume of transactions or events.

One practical thought: do not build the fanciest version first. Build the smallest version that helps the team make better decisions, then improve it with real feedback. It sounds less exciting, but it works.

If you’re building in-house, the costs are scattered across infrastructure, salaries, and data licenses. It’s frustrating, I know.

Below is a rough comparison. Keep in mind these are ballpark figures—your mileage will absolutely vary depending on transaction volume, geography, and how messy your legacy systems are.

| Feature / Cost Factor | MVP | Mid-Level Product | Enterprise Solution |

| Monthly Platform Fee | $0 – $500 (often usage-based only) | $1,500 – $5,000 | $10,000 – $50,000+ (custom negotiated) |

| Per-Transaction / API Cost | $0.10 – $0.30 | $0.03 – $0.10 (volume tiers kick in) | <$0.02 or bundled into flat fee |

| Setup / Onboarding Fee | $0 (self-serve) | $2,000 – $10,000 | $25,000 – $100,000+ |

| False Positive Rate Tolerance | Higher (3–8%) — acceptable trade-off | Moderate (1–3%) — actively tuned | Very Low (<1%) — custom models + human review |

| Integration Time | Days to 2 weeks | 4–12 weeks | 3–9 months |

| Dedicated Support / Analyst | Community docs / email ticketing | Shared account manager, SLA-backed | Dedicated fraud analyst team, 24/7 coverage |

| Custom Model Training | Not available (generic model only) | Limited tuning, periodic retraining | Continuous learning on your proprietary data |

| Best For | Validating product-market fit | Scaling safely | High-volume, regulated, or high-risk verticals |

Common Challenges in Fraud Detection Software Development

Fraud detection has some classic traps.

False positives are the obvious one. Blocking fraud is good. Blocking good customers is expensive in a quieter way. A system that is too aggressive may look effective on paper while damaging growth.

Data imbalance is another issue. Fraud is usually a small percentage of total activity, which makes model training tricky. If the dataset is messy, the model may learn patterns that do not generalize.

Delayed feedback is painful for fraud prevention software too. Chargebacks and confirmed fraud reports may arrive days or weeks later. By then, the attacker has changed tactics, and the model is learning from old news.

Explainability matters. Risk teams, support agents, compliance people, and sometimes customers need to understand decisions. “The algorithm said so” is not a great sentence to build trust around.

Scalability is easy to underestimate. A scoring service that works during normal traffic may struggle during sales events, payroll days, trading spikes, or promotional campaigns. Funny how fraud also enjoys peak traffic.

And then there is maintenance. Rules need owners. Models need monitoring. Reviewers need training. Reports need interpretation. Fraud detection is not a set-it-and-forget-it feature.

Our Experience in Creating Fraud Detection Sofware

Fraud detection software often lives in the same neighborhood as fintech, data-heavy dashboards, identity flows, and complex decision interfaces.

For ZAD, Shakuro designed a Shariah-compliant mobile investment platform with robo-advisor and trading features. The work included risk profiling, trading flows, portfolio views, watchlists, alerts, and dense financial screens that still had to feel manageable for everyday users. That kind of experience matters when building review dashboards or risk interfaces, because fraud teams also need to understand complex data quickly.

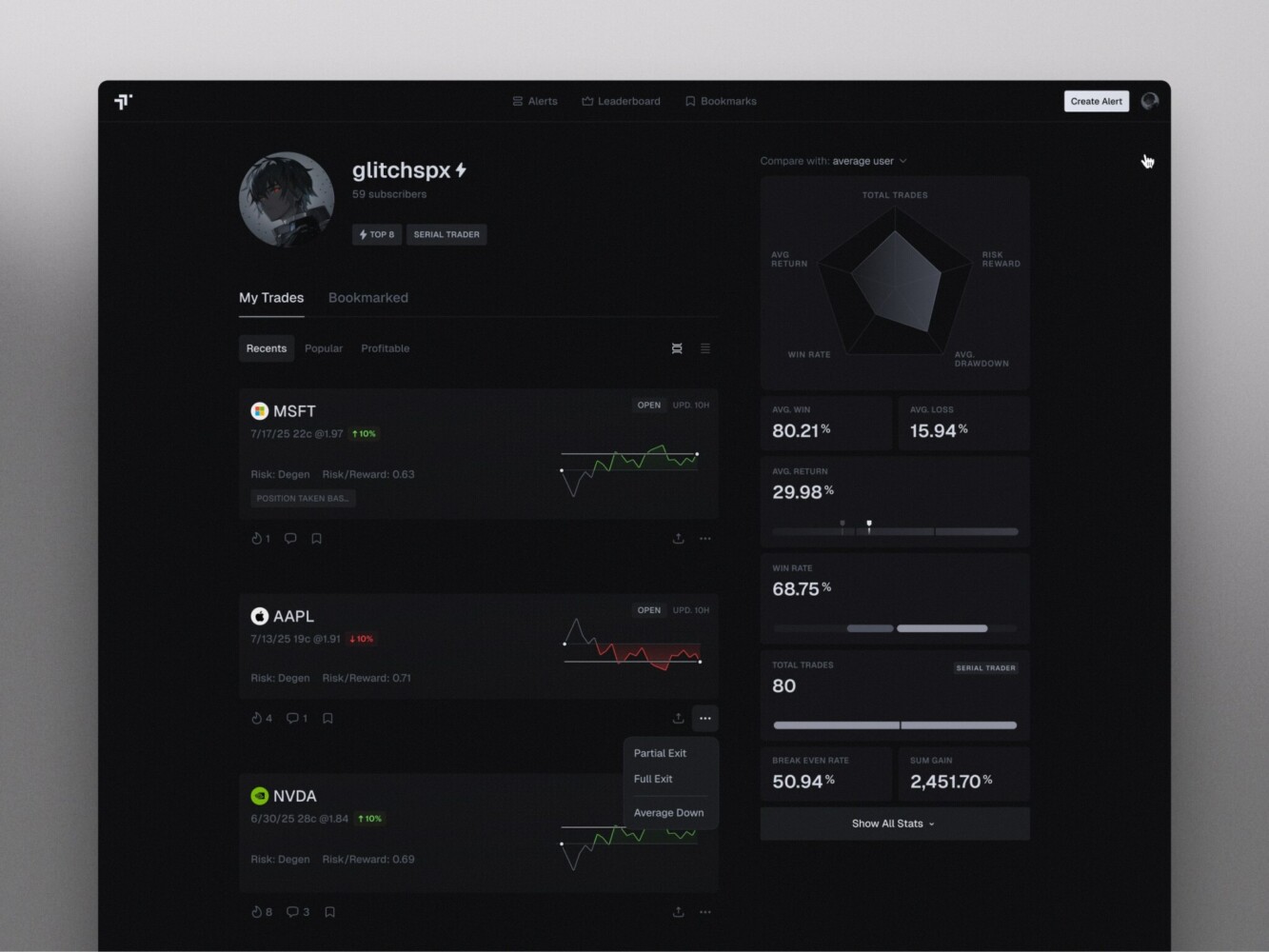

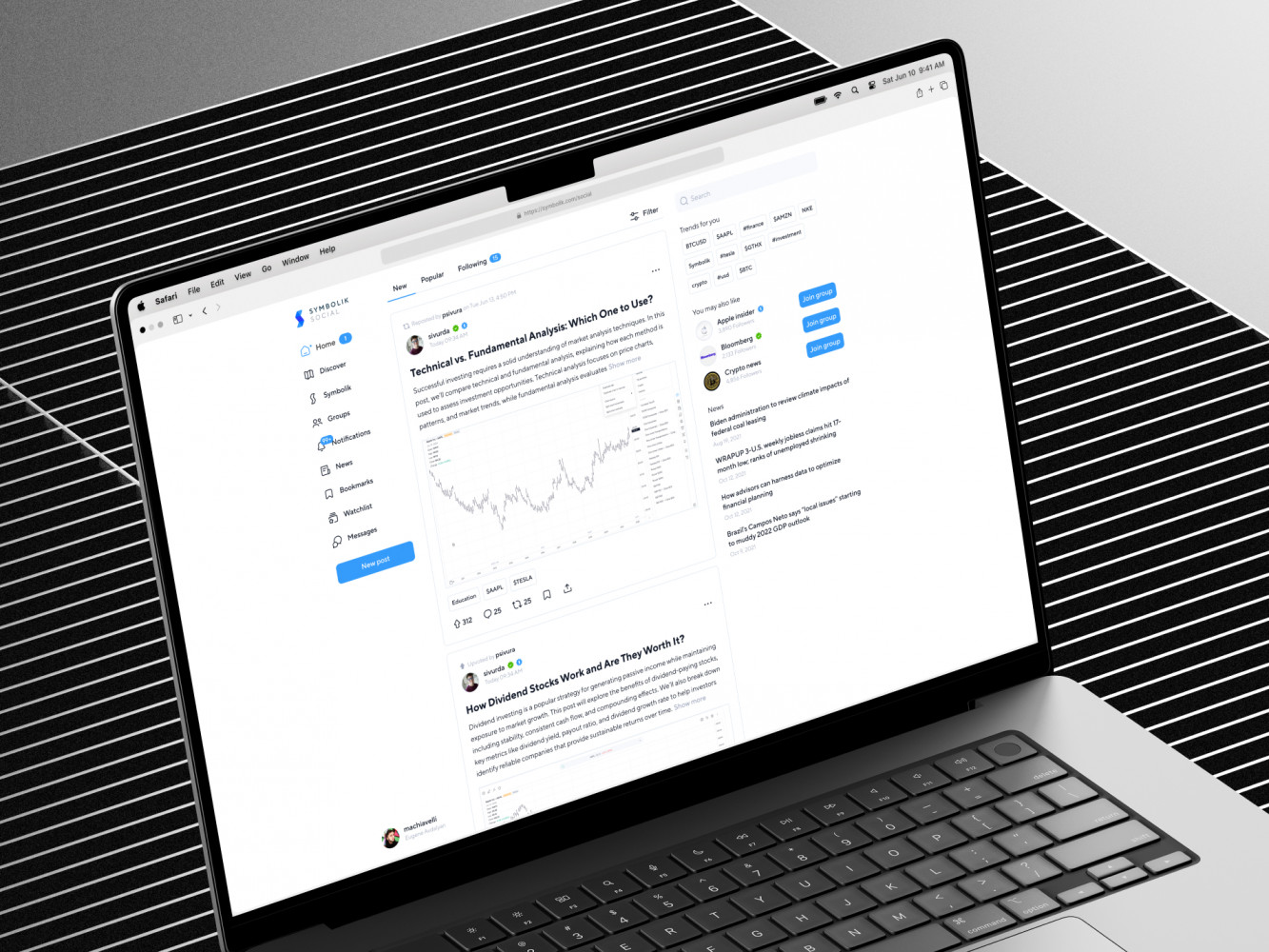

Symbolik is another relevant case. It is a trading analysis platform and investment tool centered on charting, financial analytics, and a broader product ecosystem. The project involved UI/UX work around structured financial data, social functionality, and a product experience where clarity is not decoration. It is the thing that lets people make decisions.

And if the fraud product includes AI, the same idea applies. The model may be smart, but the interface has to make its output useful. Otherwise, people will ignore it, mistrust it, or use it inconsistently.

Symbolik case by Shakuro

Why Work With a Fraud Detection Software Development Company

Some teams can build fraud tooling internally, and that is perfectly valid. But many companies reach a point where a few scripts, vendor dashboards, and spreadsheet reviews are not enough.

A development partner can help connect the moving pieces: architecture, data engineering, machine learning, UX, integrations, security, and long-term support. The value is not just writing code. It is asking annoying questions early, the kind that save money later.

What happens when the scoring service goes down? Who can edit rules? Can reviewers explain a decision? How do you measure false positives? What data is allowed to be stored? How will the system behave in a new country or with a new payment method?

These are not glamorous questions. They are, however, the questions that make the product sturdy.

Final Thoughts

Fraud detection software is not only a model, and it is not only a rules engine. It is a living product made of data, decisions, workflows, interfaces, security, and feedback loops.

The goal is not to block everything suspicious. That would be easy, and also terrible for business. The real goal is to make better decisions faster, with enough context to protect the company and still treat good users like humans.

Three takeaways are worth keeping close:

- Start with the fraud risks that hurt your business most.

- Build workflows for people, not just algorithms.

- Treat monitoring and improvement as part of the product from day one.

If you are planning to create a fraud detection platform or trying to improve one that already exists, reach out to us. Our fintech development team will help you build a reliable product.

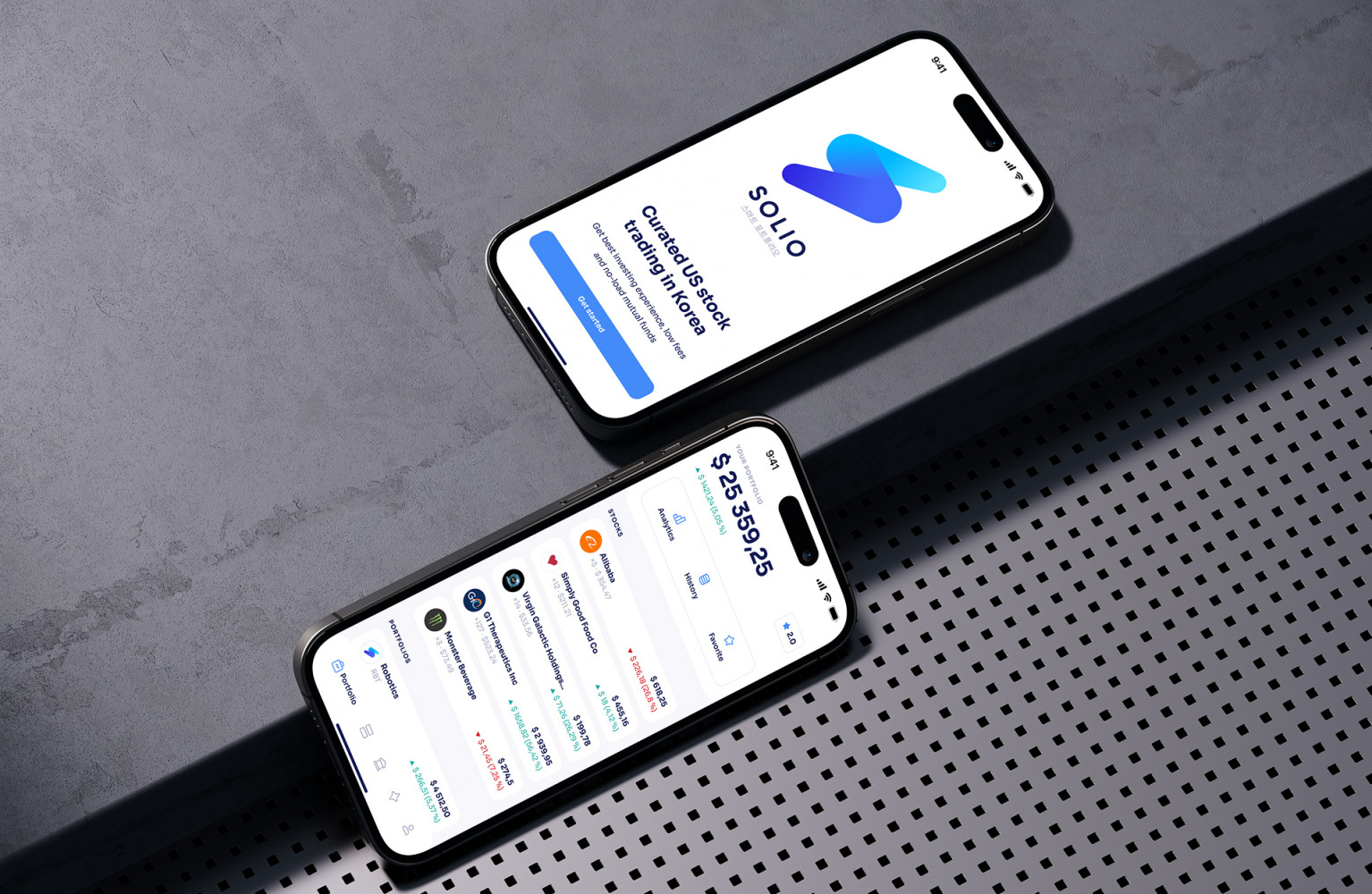

Solio App by Shakuro

FAQ

What is fraud detection software?

Fraud detection software monitors digital activity, scores risk, and flags suspicious behavior. It can be used for payments, accounts, marketplaces, SaaS platforms, banking products, ecommerce stores, and many other systems where abuse can happen.

How does AI help with fraud detection?

AI can find unusual patterns, predict risky behavior, connect related events, and help reduce false positives. It works best when paired with clean data, human review, clear workflows, and ongoing monitoring.

How long does it take to build fraud detection software?

A focused MVP may take a few months, depending on integrations and scope. A more advanced system with real-time scoring, machine learning, case management, and compliance features will take longer. The honest answer is that data readiness often affects the timeline as much as coding.

Can fraud detection software reduce false positives?

Yes, if it is designed carefully. Better data, model tuning, review feedback, explainable risk scores, and thoughtful thresholds can all help. But false positives rarely disappear completely. The goal is to manage them intelligently.

What integrations are usually needed?

Common integrations include payment processors, KYC providers, device intelligence tools, CRM systems, customer support platforms, analytics tools, data warehouses, notification services, and internal admin systems.