For those who prefer to listen rather than read, this article is also available as a podcast on Spotify.

Contents:

Introduction

The numbers are hard to argue with. The Islamic finance sector is growing way faster than conventional banking in many regions, and there’s this huge, underserved population of Muslims who want modern banking apps but also need to stick to their faith.

If you’re a CTO or a product manager trying to wrap your head around this, you might feel a bit overwhelmed. You can’t just simply slap a “Halal” label on an existing core banking system and call it a day. That won’t work. Instead of lending money for a fee, you end up creating models based on risk-sharing or asset-backed financing like Murabaha or Musharakah.

The challenge is making complex profit-sharing calculations feel as smooth as a standard transfer. It’s a little annoying at first when you realize your usual libraries for modern digital banking platforms don’t quite fit, but you get used to it over time.

That’s exactly what we’re going to dig into here. We’ll walk through the actual principles of Shariah-compliant banking software development. We’ll look at the key features that make a platform truly Shariah-compliant, because trust me, users can spot a fake from a mile away. Then we’ll get our hands dirty with the development architecture and tech stack choices that actually work for this specific domain. And finally, we can’t skip the regulatory headache.

What Is Shariah-Compliant Banking Software?

If you ask a developer who’s only worked with Western banks, they might tell you it’s just a regular app with a few extra filters. Far from the truth, though.

In reality, this software is the digital backbone for Islamic financial institutions. It’s an entire ecosystem designed to ensure every single byte of data and every algorithmic decision aligns with Islamic law (Shariah).

The role of Shariah-compliant financial software is critical because, unlike conventional systems where compliance is often a final checkpoint, here, the compliance logic is the product logic. If the code allows an interest calculation to slip through, the whole transaction becomes invalid religiously. That’s a level of stakes you don’t usually see in standard fintech.

The biggest difference between this and conventional banking is the fundamental philosophy of money. Conventional banking treats money as a commodity itself: you can rent it out (that’s interest) and make money from money. Here, financial monitoring and reporting systems say, “Hold on.” Money is just a medium of exchange. You can only make a profit by trading real assets or sharing in actual business risks. This shifts the entire financial model from debt-based to equity- or trade-based. Trying to retrofit a conventional core banking system to handle this is like trying to put square pegs in round holes. You really need systems built from the ground up with these differences in mind.

Let’s break down the core pillars that drive how a Shariah-compliant banking platform actually functions.

Key principles of Islamic finance

At the heart of everything is the absolute prohibition of riba, which translates to interest. Your standard loan origination module? Useless. You can’t have a system that automatically accrues interest over time based on a principal amount.

Financial systems here must be architected to avoid interest-based lending entirely. Instead of charging a fee for the time value of money, the software has to facilitate trade or leasing arrangements.

For example, if a customer wants to buy a car, the bank (via the software) buys the car first and then sells it to the customer at a markup, payable in installments. The code needs to track the asset ownership transfer, not just a balance sheet adjustment. It’s a completely different workflow. If your database schema assumes interest is a native field, you’re going to have a bad time refactoring it later.

Profit-and-loss sharing models

Since you can’t charge guaranteed interest, Islamic finance relies heavily on risk-sharing. The bank and the customer become partners. If the business venture succeeds, they share the profits. If it fails, they share the loss.

Two main models you’ll see constantly in the requirements docs for islamic banking software development are Mudarabah and Musharakah.

Mudarabah is like a silent partnership. One party provides the capital (the bank), and the other provides the expertise and labor (the entrepreneur). The application needs to track profit distribution ratios meticulously, but crucially, it also has to handle scenarios where there’s no profit. In a conventional loan, the bank gets paid regardless. Here, if the venture loses money due to market forces, the bank absorbs the financial loss. Coding the logic to handle variable returns instead of fixed amortization schedules is a whole different beast.

Musharakah is a joint partnership where both parties contribute capital and share management. Like a joint venture. Shariah-compliant financial software must dynamically calculate returns based on actual performance and agreed-upon ratios. It’s less predictable than a fixed-interest loan, which means your reporting modules need to be way more flexible.

Asset-backed financing

Transactions must involve real assets. You can’t just trade paper or speculative instruments like derivatives for the sake of speculation, which is called Gharar, or excessive uncertainty, and is also prohibited.

Every transaction in the system needs to be tethered to something tangible: a house, a car, gold, or commodities. The software architecture has to maintain a clear audit trail linking the financial flow to the underlying asset. You can’t just move numbers from Account A to Account B; the system needs to verify that an asset changed hands or is being leased.

In shariah-compliant banking software development, this often means integrating with inventory management or property registries in ways that conventional banking apps never do. It adds layers of complexity, sure, but it also creates a natural safeguard against the kind of speculative bubbles we’ve seen crash global markets before.

Ethical investment restrictions

Even if it appears lucrative and asset-backed, it’s a non-starter if it’s financing industries that Shariah does not allow. The software must have robust mechanisms for screening and stopping investments from going into sectors such as:

- Gambling (casinos, betting sites)

- Alcohol production or distribution

- Weapons manufacturing (especially non-defensive or controversial weapons)

- Unethical financial activities (such as conventional insurance with elements of uncertainty, or pork products)

In some cases, these screenings could be done in real-time. If an attempt is made by the fund manager to invest in an entity that derives some portion of their revenue from these sectors, it should be immediately flagged or prevented.

You know, when you look at all these requirements together, it’s clear that this type is a fundamentally different approach to handling value. It forces transparency, ties finance to the real economy, and bakes ethics into the code.

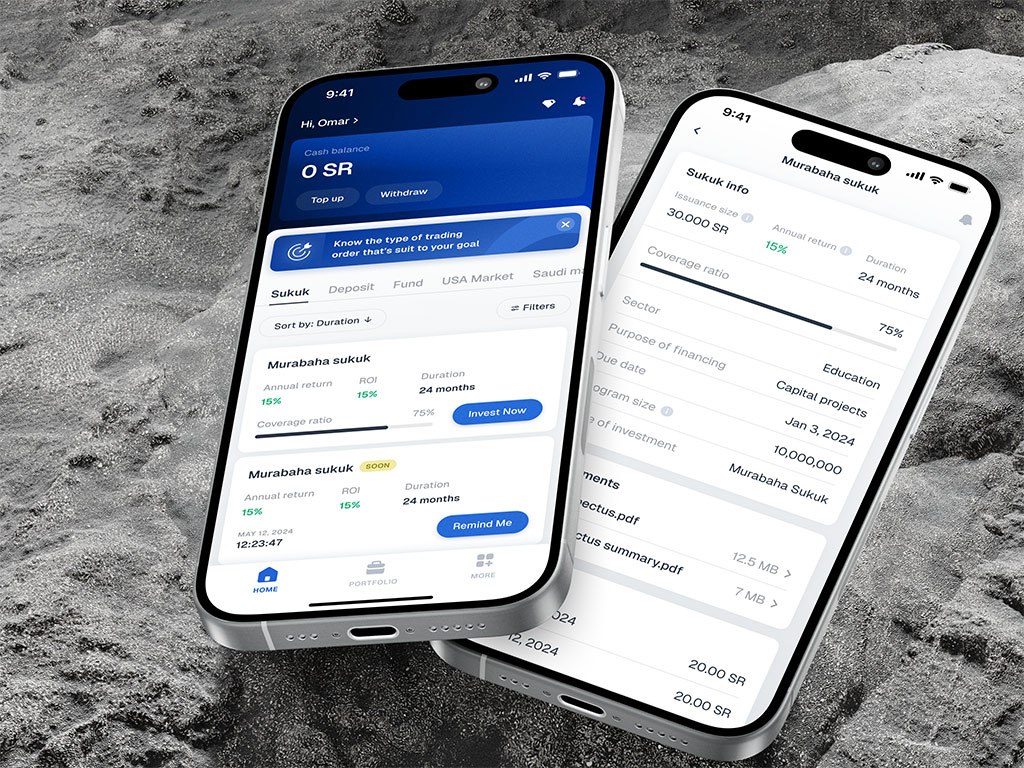

Dinar app by Shakuro

Core Features of Shariah-Compliant Banking Platforms

Islamic Finance Product Management

First off, your product module can’t just handle generic “loans” or “savings accounts.” Those terms don’t even exist in the same way here. The product needs native support for specific Islamic contracts. If you try to force these into a standard lending template, you’re going to run into compliance walls pretty fast.

You need digital workflows for contracts like Murabaha (cost-plus financing), where the system has to manage the bank buying an asset and selling it to the customer at a markup. The software has to track two distinct sale events.

Then there’s Musharakah and Mudarabah, which we touched on earlier. These require the system to calculate variable profit distributions based on actual performance, not fixed interest rates. And don’t forget Ijara (leasing). The platform needs to handle asset ownership, lease payments, and eventual transfer of title.

The trickiest part in Shariah-compliant fintech development is the state machine. A Murabaha transaction has very specific steps: offer, acceptance, purchase, sale, and delivery. If step 3 happens before step 2 in the database logs, the whole contract is void. Your product management module needs to enforce this sequence rigidly. It’s a bit more complex than a standard “approve and disburse” flow, but once you model it right, it actually reduces legal risk significantly.

Compliance and Shariah Governance

In conventional banking, compliance is often about avoiding fines. In Islamic banking, it’s about religious validity. If the software fails here, the product is literally useless to the target audience.

You need built-in integration for the Shariah advisory board. Think of it as a governance module where scholars can review and approve new product structures digitally. But it goes deeper. You need immutable audit trails. Every single transaction needs a timestamped log showing exactly how it adhered to Shariah principles. Was the asset verified? Was the profit rate calculated correctly without compounding interest? The system must answer “yes” instantly.

Manual checks don’t scale. You need AI-powered compliance monitoring running in real-time. Imagine a rule engine that blocks a transaction the millisecond it detects an interest calculation or a prohibited counterparty. Islamic fintech software development sounds intense, but users trust platforms that can prove their compliance with a click.

Ethical Investment Screening

Let’s say you’re building a wealth management or investment module. You can’t just pull data from any old stock API. The platform needs a robust ethical investment screening engine.

This feature has to filter potential investments based on strict Shariah criteria. It’s not enough to check the company’s main business; the software often needs to analyze financial ratios too, like debt-to-equity levels, to ensure the company isn’t overly leveraged. The system should automatically flag or exclude companies involved in gambling, alcohol, weapons, or other prohibited activities.

At the same time, you have to integrate continuous portfolio monitoring. Companies change. A tech firm might start investing heavily in interest-bearing bonds or acquire a subsidiary in a prohibited sector. Your platform needs to detect these shifts and alert the user or automatically trigger a divestment process. Missing this feature is a quick way to lose user trust.

Payment and Transaction Infrastructure

Under the hood, the payment rails need to be clean. This means supporting halal financial transactions end-to-end. For islamic banking platform development, it’s crucial that money transfers don’t involve impermissible elements.

For instance, late payment penalties are tricky. In conventional banking, you charge interest on late payments. In Islamic finance, you might charge a penalty to discourage delay, but that money cannot be recognized as income for the bank. It usually has to be donated to charity. Your payment infrastructure needs to handle this logic automatically by segregating penalty funds and routing them to charitable accounts without touching the bank’s P&L. If you miss this detail, you’ve accidentally generated riba.

Plus, you’ll need deep integration with payment gateways and banking systems that understand these nuances. Not all gateways handle split payments or charitable routing out of the box. You might find yourself building custom connectors, which is a pain, I know, but it’s necessary for a secure payment processing infrastructure to keep the ecosystem pure.

Mobile and Digital Banking Interfaces

None of this matters if the user interface is a mess. People expect modern, slick apps. They don’t want to feel like they’re using legacy software just because it’s Shariah-compliant.

You need mobile-first banking platforms that feature these complex products front and center. Think of a dashboard where the consumer can get real-time updates on the performance of their Musharakah investment, with visualizations of the profit share versus capital contribution. Think of a Murabaha tracker that lets the consumer know exactly what stage their home financing is at: “Bank purchasing property,” “Property transferred,” or “Installment plan active.”

The key to success in islamic finance software development is user-friendly dashboards. Your job as a product designer is to translate “profit-sharing ratio” and “asset-backed leasing” into simple, actionable insights. Use plain language. Maybe add tooltips that explain why a certain transaction is structured the way it is. Education builds confidence. If a user understands that the extra step in their transaction is there to protect their faith, they’ll appreciate it. But if the app feels clunky or confusing, they’ll bounce.

Putting all these features together creates a platform that’s competitive and compliant.

ZAD app by Shakuro

Shariah-Compliant Banking Software Development Process

1. Product Strategy and Shariah Compliance Planning

Before a single line of code is written, you have to get your head around the financial model. And I mean really get your head around it. You can’t just say, “We’ll do a home loan.” You have to decide: Is it Murabaha? Is it Ijara? The structure dictates everything that follows.

This is where you consult with Shariah scholars and compliance boards. Seriously, don’t skip this or try to wing it based on Google searches. The best projects start with a whiteboard session involving both your product leads and a qualified scholar. They’ll tell you exactly where the pitfalls are.

For instance, they might point out that your proposed profit calculation method accidentally mimics compound interest. Catching that on day one saves you from rewriting your entire core engine later. The goal here is simple: ensure every product structure follows Islamic finance rules before it becomes a technical requirement.

2. UX/UI Design for Islamic Finance Applications

Once the logic is solid, you move to design. This is tricky because Islamic finance contracts can be, well, a bit wordy and complex compared to a standard “Take $500” button. Your job as a designer is to simplify these complex contracts without dumbing them down so much that they lose their meaning.

You need interfaces that guide the user through the steps. If you’re doing a Murabaha purchase, the UI should clearly show: “Step 1: You request the item.” “Step 2: We buy it.” “Step 3: We sell it to you.” It makes the process transparent. And transparency is key. Users need to see the transaction flow clearly to trust that no hidden interest is slipping in. If the design feels opaque, people will get suspicious. Keep it clean, use plain language, and maybe add a little “Why is it structured this way?” tooltip. It goes a long way.

If you opt for islamic banking software development, you may need to integrate foreign languages, like Arabic. And this means localizing the interface for right-to-left languages, where sometimes you have to rearrange the UI elements.

3. Choosing the Technology Stack

You don’t need some exotic, obscure language to build this. The standard enterprise stack works perfectly fine; it’s all about how you configure it.

For the backend, you’ve got solid options. Java is a classic choice for big banks because of its robustness and strict typing, which helps prevent those nasty logic errors in financial calculations. Python with FastAPI is the way to go when speed and flexibility are the main concerns, especially when dealing with data-intensive operations like investment screening. Node.js is the best choice when dealing with real-time updates, like sending profit-sharing notifications to the user base. C# (.NET) is still the king of finance when you need to integrate with old legacy systems.

For the frontend, React and Vue are the choices here. These allow us to create the dynamic, interactive interfaces we discussed earlier, with components that can recalculate profit shares without needing the user to reload the page.

For databases, PostgreSQL is probably the safest bet. Its ACID compliance is non-negotiable when you’re dealing with asset ownership trails. You’ll definitely want Redis for caching, though, because calculating profit distributions on the fly can be heavy.

When it comes to infrastructure, containerize everything. Docker and Kubernetes make it way easier to manage different environments and scale up during peak times, like Ramadan or Eid, when transaction volumes spike. Trust me, you don’t want your app crashing during those weeks.

4. Compliance and Security Architecture

Security is always huge in fintech, but in islamic banking platform development, it’s doubled with compliance. You need secure transaction processing that guarantees data integrity. If a transaction record gets corrupted, you can’t just “fix it” later; the religious validity might be compromised.

You also need to build compliance monitoring systems directly into the architecture. This is especially vital for a blockchain-based financial infrastructure. Think of it as a watchdog service that runs alongside your main app, checking every transaction against the rule set. Did this trade involve a prohibited stock? Did this loan calculation accidentally use an interest rate? The system needs to flag it instantly.

And don’t forget the audit trails. Regulators and Shariah boards will want to see a complete, immutable history of every action. Who approved this contract? What was the asset value at the time of sale? Your database design needs to support versioning and detailed logging out of the box. It’s a bit of a pain to set up, but try explaining to a board why you can’t produce a log from six months ago.

5. Integrations with Financial Ecosystems

No bank is an island. You’ll need to connect your shiny new platform to the wider world. This means integration with Islamic banks, payment providers that understand halal transaction flows, and specialized compliance services for real-time screening.

You’ll also need to tap into financial data systems for things like gold prices, commodity markets (for Murabaha), and stock screening data. The trick in Shariah-compliant fintech development is that not all APIs are created equal. Some conventional data feeds might include interest-based benchmarks by default. You have to be careful to filter those out or find alternative data sources that align with Islamic principles. Building such a digital payment infrastructure takes some extra legwork, but it’s worth it.

6. Testing and Shariah Compliance Verification

Sure, you’ll do your standard software testing, like unit tests, integration tests, and load tests. But that’s only half the battle.

The critical part is the compliance verification with Shariah advisory boards. Before you go live, you essentially have to submit your software logic for certification. The scholars will review your algorithms, your contract flows, and your edge cases. They might ask, “What happens if the asset is destroyed before delivery?” If your code doesn’t handle that specific scenario according to Shariah, you’re not ready.

Obviously, security audits are mandatory for islamic finance software development. You’re handling people’s life savings, after all. A breach here could shake confidence in the entire concept of digital Islamic banking. So, throw everything at it: penetration testing, code reviews, the works.

7. Deployment and Maintenance

Finally, you launch. Still, there are lots of things to do. Platform monitoring needs to be 24/7. You’re looking for performance issues, sure, but also for any anomalies that might suggest a compliance drift.

Speaking of drift, compliance updates are a constant thing. Shariah interpretations can evolve, and regulations in different countries change. Your team needs to be ready to patch the logic quickly. Maybe a new type of investment becomes permissible, or a certain screening criterion tightens. Your architecture needs to be flexible enough to handle these changes without a total rewrite.

The market moves fast, so the features need to develop consistently. Users will want new tools, better insights, faster payments, etc. You have to balance innovation with strict adherence to the rules. If you get it right, you’re building something that truly serves a community while standing on solid ethical ground.

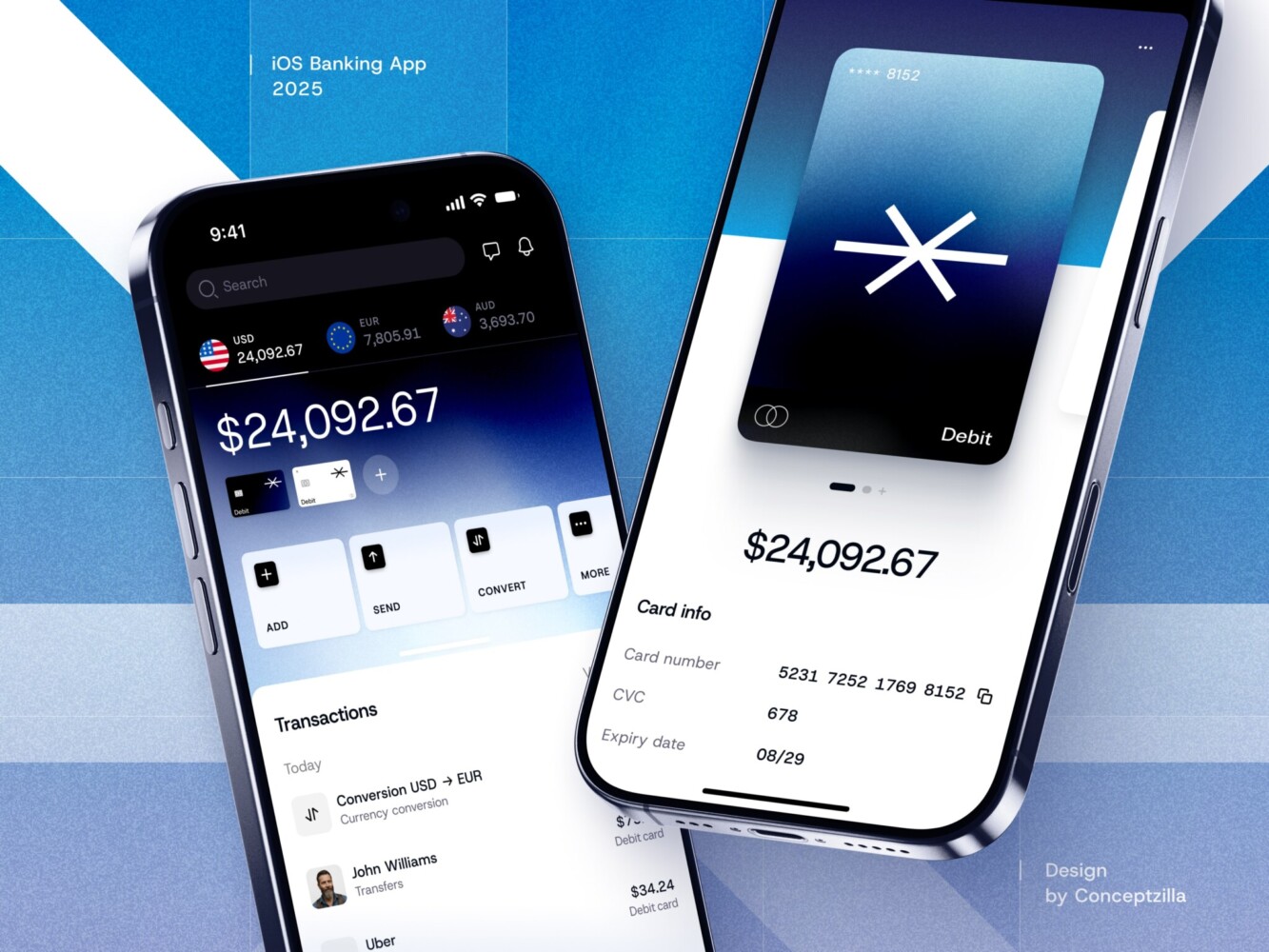

Fintech Mobile Banking App by Conceptzilla

Cost of Shariah-Compliant Banking Software Development

How much does it cost to build the software that handles money the right way? If you’re a founder pitching to investors or a CTO trying to budget for the next year, you’ve probably already guessed that this type of development isn’t exactly cheap. But why? Is it just because it’s “niche”? Not really. It’s mostly because you’re building two systems at once: a high-tech fintech platform and a rigorous compliance engine.

The sticker shock usually comes from underestimating the complexity of financial products. Remember, you can’t just use off-the-shelf loan modules. Coding a Musharakah profit-sharing algorithm that dynamically adjusts based on real-time business performance is way harder than coding a simple fixed-interest amortization schedule. You’re essentially building custom logic for every single product type. If you want to offer a wide range of products, your islamic banking software developers‘ working hours add up fast.

Then there are the compliance requirements. This is a huge cost driver. You aren’t just hiring developers; you’re paying for Shariah scholars, legal consultants, and compliance officers to review your code logic. It’s an iterative process. You build a feature, a scholar reviews it, says “this step violates the principle of X,” and your team has to go back and refactor. That loop happens multiple times. It feels a bit annoying when you’re trying to move fast, but honestly, skipping it would be catastrophic. The cost here is time. And time is money, right?

Don’t forget integrations with banking infrastructure. The Islamic banking world is a bit fragmented. Unlike the somewhat standardized SWIFT or SEPA systems in the West, you might find yourself building custom connectors for local Islamic banks, specific commodity trading platforms (crucial for Murabaha), and niche payment gateways that understand halal transaction flows. These aren’t always plug-and-play APIs. Sometimes you’re dealing with legacy systems that require serious engineering muscle to bridge.

Finally, a Shariah-compliant banking platform should be scalable. If you’re planning to grow across borders, for example, from Malaysia to Saudi Arabia to the UK, you need an architecture that can handle different regulatory regimes and Shariah interpretations simultaneously. Building a multi-tenant system that isolates compliance rules per region adds a layer of architectural complexity that definitely bumps up the initial dev cost.

So, what does this look like in real numbers? Well, I can’t give you an exact quote without knowing your specific scope, but let’s look at two common scenarios to give you a ballpark idea.

MVP Islamic Fintech Platform

Let’s say you’re building an MVP Islamic Fintech Platform. Maybe you’re targeting one product specifically, such as a digital Murabaha-based personal financing system or an ethical investment-based robo-advisory system. Since you’re targeting one market, you’ll only have one set of local regulations to comply with.

You’ll be using the latest technology stack with Node.js or Python with React.js as the front end and heavily leveraging third-party APIs to speed up development with regards to identity verification and basic payment systems. You’ll also need one Shariah consultant on a consultancy basis instead of having them on the board.

The costs? It’ll be between $80,000 to $150,000 at the very least. This will get you a basic app with the necessary features and UI/UX. It won’t be perfect by any stretch of the imagination, but at least it’ll get the job done. It won’t support complex products such as multiple asset classes just yet, but at least you’ll have something to test the waters with and lock in the competition. It’s a tight budget, and you’ll need to cut everything that isn’t strictly necessary for Islamic banking software development. Yeah, right.

Enterprise Islamic Banking System

Now let’s say you’re a traditional bank looking to launch a fully digital Islamic banking subsidiary or a well-funded Fintech looking to dominate the market in one region or another. You’ll want to launch the entire gamut of products, such as savings accounts, current accounts, home financing options (Ijara), business financing options (Mudarabah/Musharakah), wealth management options, and Takaful insurance products.

This beast needs to integrate with core banking systems, multiple payment rails, international commodity exchanges, and comprehensive screening databases. You’ll need a dedicated internal Shariah board, robust audit trails, multi-language support, and enterprise-grade security. The architecture has to be bulletproof, scalable to millions of users, and flexible enough to adapt to regulations in five or six different countries.

Here, the costs jump significantly. We’re talking about ~$500,000 to $2 million+, and that’s just for the initial build. Why so much? Because you’re essentially building a bank from scratch. The testing phase alone could take months. The integration work is massive. And the ongoing maintenance and compliance updates will require a dedicated team of islamic banking software developers. It’s a heavy lift, no doubt. But if you pull it off, you’re building a moat that competitors will find very hard to cross.

While the upfront cost is higher, the long-term risk is often lower. Because you’ve baked compliance into the code from day one, you avoid those expensive retrofits and regulatory fines that plague conventional fintechs later on.

So, is it expensive? Yes. Is it worth it? If you’re serious about serving this market and doing it right, absolutely. Just go in with your eyes open and a realistic budget. Trying to cut corners on Shariah compliance is the fastest way to burn cash and lose trust.

Finance Management Mobile App Design by Shakuro

Challenges in Shariah-Compliant Fintech Development

If building such software was easy, every major bank would have done it years ago. The truth is, while the opportunity is massive, the road is full of potholes that you just don’t see in conventional fintech. Talented teams stumble over these same hurdles because they underestimated how deeply these challenges run into the very fabric of finance and law.

Ensuring full compliance with Islamic finance principles

In regular digital banking platforms, if your code has a bug that miscalculates interest by 0.1%, you fix it, maybe refund the customers, and move on. In Islamic finance, that 0.1% error could render the entire contract religiously void (haram).

The challenge of islamic fintech software development is translating nuanced theological concepts into rigid binary logic. Scholars might debate the finer points of a specific Murabaha structure for weeks. Your job is to take that debate and turn it into an if-else statement that never fails.

It’s not static, by the way. Interpretations evolve. What was acceptable five years ago might be questioned today. You have to build systems flexible enough to adapt without breaking existing contracts. It’s a little annoying, honestly, because it means your “done” list is never really done. You’re constantly validating logic against a moving target of ethical standards.

Adapting traditional financial infrastructure to Islamic financial models

Most of the world’s financial plumbing is built for debt. SWIFT, core banking ledgers, credit scoring models—they all assume money has a time value (interest). Trying to run asset-backed, risk-sharing models on top of this is like trying to drive a square-wheeled car on a highway designed for circles.

Take commodity trading, for example. Many Islamic financing deals require the bank to actually buy and sell a physical commodity (like palm oil or metal) instantly to facilitate the transaction. Conventional banking APIs aren’t built for this rapid, back-to-back trading flow. They expect a simple debit and credit.

You often find yourself building complex middleware just to simulate the ownership transfer that must happen legally and religiously. Or consider profit-sharing: traditional ledgers expect fixed liabilities. Coding a ledger that handles variable, performance-based returns requires a fundamental rethink of the database schema. You can’t just patch it; you often have to build parallel systems, which doubles the maintenance headache.

Integrating Shariah governance processes into software systems

In conventional fintech, compliance is usually a report you generate at the end of the month. In islamic banking platform development, governance is live. You need to integrate the Shariah board directly into the software workflow.

Before a new product feature goes live, it needs digital approval from the scholars. But it doesn’t stop there. The system needs to continuously monitor transactions to ensure they stay within approved parameters. If a fund drifts too heavily into a prohibited sector due to market shifts, the software needs to flag it immediately, maybe even freeze certain actions until reviewed.

Building this “digital scholar” layer is tough. How do you codify human judgment? How do you create an audit trail that satisfies both a tech auditor and a religious scholar? They speak different languages. One wants JSON logs and latency metrics; the other wants proof of asset possession and intent. Bridging that gap requires a UX and backend architecture that captures context, not just data. It’s a unique challenge that standard compliance tools just don’t solve.

Supporting global Islamic finance regulations

You might think, “Okay, I’ll just follow AAOIFI standards, and I’m good. ” Well, not exactly. While AAOIFI provides a framework, local regulators in Malaysia, Saudi Arabia, Pakistan, the UK, or Bahrain often have their own specific rules that can contradict each other.

A product structure approved in Kuala Lumpur might need significant tweaking to launch in Riyadh. Maybe the documentation requirements differ, or the definition of a permissible asset varies slightly. If you’re building a global platform, you need a multi-tenant architecture where compliance rules are configurable per region.

And let’s not forget the regulatory reporting in Shariah-compliant banking software development. Each country wants reports in different formats, with different metrics. Keeping up with these changes is a full-time job. Many startups burn through cash trying to manually adjust their systems for each new market entry. The key is to abstract the regulation layer as much as possible, but even then, it’s a constant battle to stay synchronized with global shifts.

You know, facing these challenges can feel overwhelming sometimes. It’s easy to look at the friction and think, “Why bother?” But then you remember who you’re building for. You’re creating a space where millions of people can participate in the modern economy without compromising their values. That friction is actually a feature. It forces a level of transparency and ethical rigor that the whole financial world could learn from.

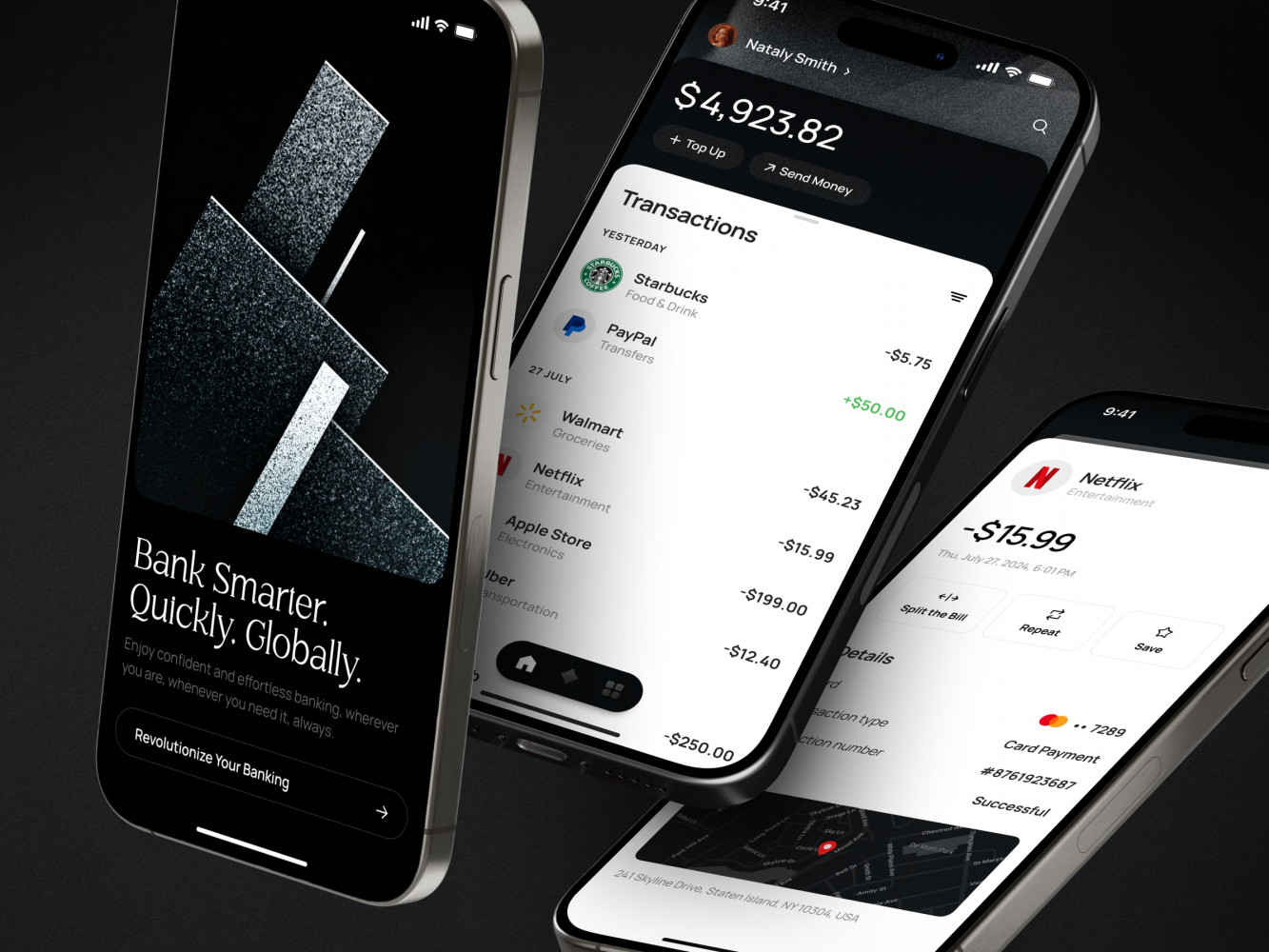

Mobile Banking App by Coneptzilla

Our Experience Building Shariah-Compliant Banking Platforms

At Shakuro, we’ve spent years navigating the complex intersection of cutting-edge tech and strict ethical guidelines. The team has moved past just “understanding” the rules to actually embedding them into the DNA of the software we build.

One project that really stands out for us, and honestly kind of defines our approach to this space, is ZAD. If you haven’t heard of it, it’s Shariah-compliant financial software that we helped bring to life, and it’s a perfect example of how you can marry ancient financial principles with modern digital expectations.

When we started working on ZAD, the goal was to make sure every single transaction, from the moment a user clicked “apply” to the final profit distribution, was structurally sound according to Islamic law. That required a serious rethink of our usual architecture.

Shariah-Compliant Financial Architecture

For ZAD, we couldn’t just plug in a standard lending module. We had to build a custom financial engine from the ground up. This meant coding logic that inherently prevents riba (interest) at the database level. Instead of computing interest over time, the system treats Murabaha and Ijara transactions as two different workflows involving multiple steps. In this project, we realized that the more restrictive the backend is, the freer the user can be.

Secure Financial Transaction Systems

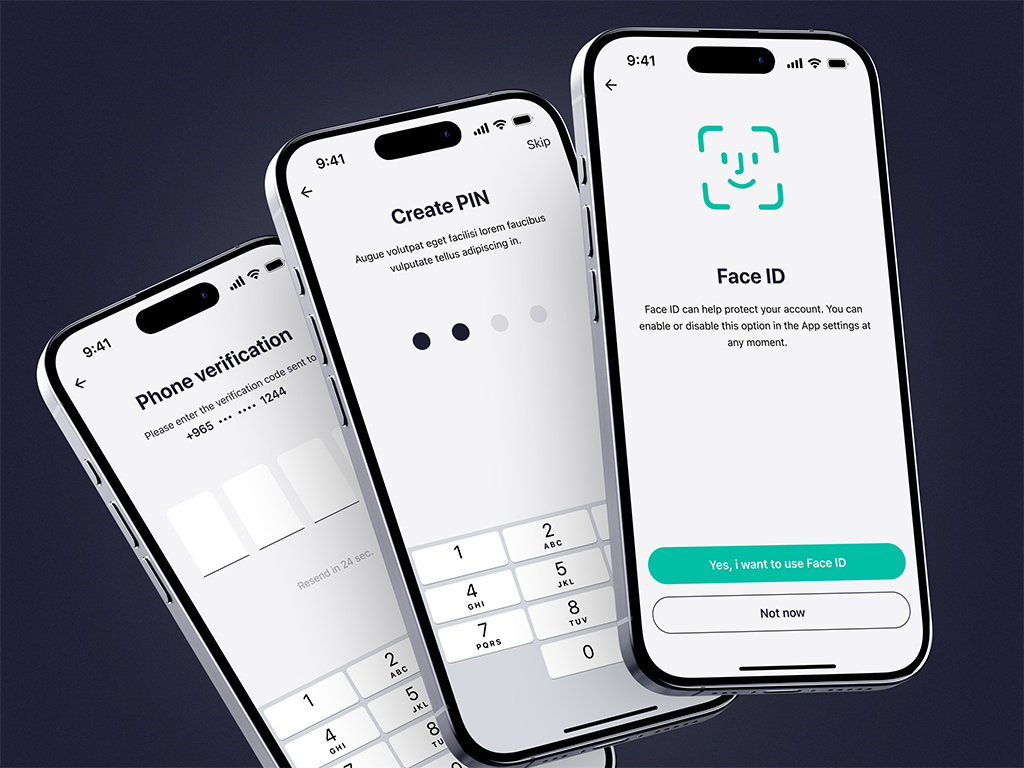

Security is obviously massive for any fintech company, but with Islamic finance software development, there is the additional factor of integrity. Institutions like the Capital Market Authority (CMA) and the Saudi Central Bank (SAMA) have very strict guidelines regarding cybersecurity measures.

In this way, the development team made sure that no one could bypass or alter the particular Shariah-compliant workflows that the system is designed to facilitate. As such, the development team has also incorporated 2-factor authentication, PIN codes, and Face ID as additional security measures.

Modern Digital Banking Interfaces

Just because the backend is complicated does not necessarily mean the same is true of the frontend. One of the biggest myths out there is that ethical banking software must also be clunky and old-fashioned. We set out to make ZAD look as slick and modern as any other top-tier neobank out there.

We worked hard at converting clunky banking interfaces into simple, glanceable, and easy-to-use interfaces. Instead of showing users a wall of legal text about Mudarabah contracts, we used plain language, helpful tooltips, and a clean, mobile-first design that makes managing finances feel effortless.

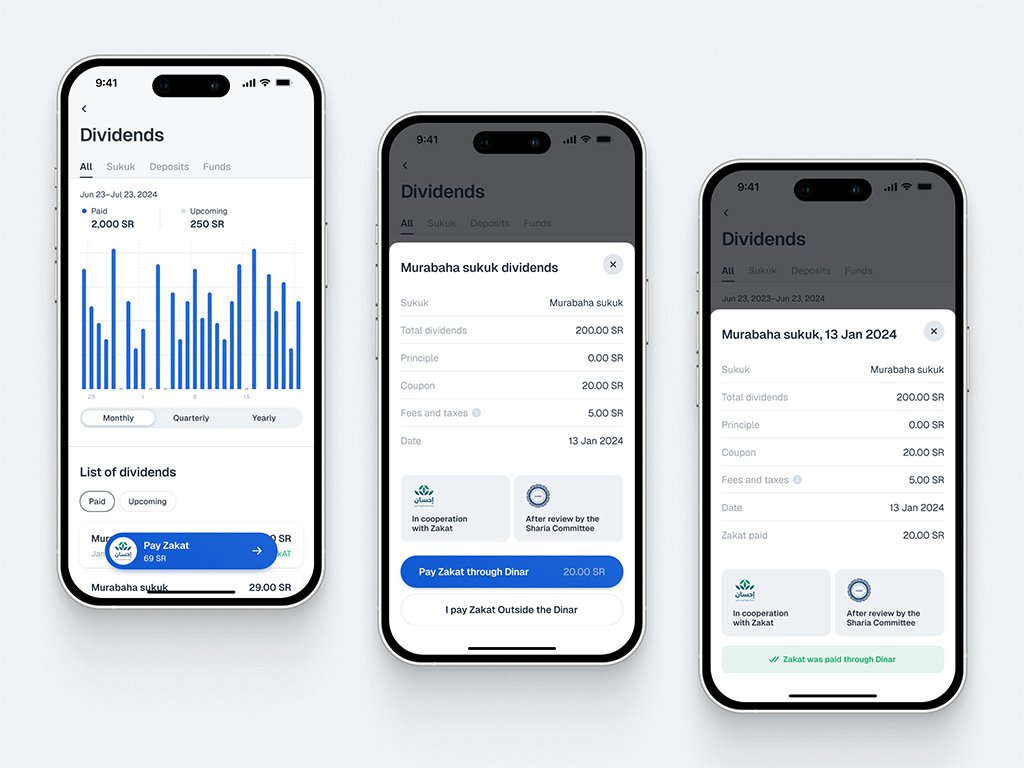

Silent authentication for ZAD app by Shakuro

Why Work with a Shariah-Compliant Banking Software Development Company

When you’re staring at a budget sheet and a timeline, the idea of hiring a specialized development partner might feel like an extra expense you could skip. But building Islamic fintech is about speaking a completely different financial language. Partnering with a company that has relevant experience and deep insights from that market really turns the tables.

Expertise in Shariah-Compliant Financial Models

If you hire generalists, you’re going to spend weeks or maybe months just explaining the difference between Murabaha and Musharakah. And even then, there’s a real risk they’ll accidentally build a logic flow that mimics interest because that’s what their muscle memory tells them to do. It happens more than you’d think.

When you work with islamic banking software developers, that learning curve disappears. They’ve already made the mistakes so you don’t have to. They know that a profit-sharing model is a dynamic algorithm tied to actual performance. They know that late payment penalties have to be routed to charity automatically.

This deep domain knowledge saves you from costly refactors down the line. You are paying to ensure your product is religiously valid from day one.

Secure and Scalable Financial Software Architectures

Financial software is hard. Adding the layer of asset-backing and complex contract states makes it exponentially harder. A standard banking architecture just won’t cut it. You need systems designed to handle multi-step ownership transfers, real-time ethical screening, and immutable audit trails without slowing to a crawl.

A specialized partner brings architectures that are battle-tested for these exact scenarios. Their team has already solved the hard problems of scaling a Mudarabah engine to handle thousands of concurrent users or ensuring that a commodity trade settles within the specific time window required by Shariah.

You get a system that’s secure by design. The same goes for scalability—the product is built with the expectation that you’re going to grow across borders, so the foundation is ready to handle different regulatory regimes without crumbling.

Experience with Global Fintech Regulations

The regulatory landscape for islamic fintech software development is a bit of a maze. What works in Malaysia might need tweaking for Saudi Arabia, and the UK has its own unique take on things. If you try to navigate this alone, you could easily build a product that’s compliant in one country and illegal in the next.

Experienced partners have been through this wringer. For example, they worked with Shariah boards across different regions. Having that global perspective means you can launch faster and with way less friction. It’s basically having a guide who knows all the shortcuts and the hidden traps.

At the end of the day, building a Shariah-compliant platform is a mission. You’re trying to serve a community that values integrity above all else. Do you really want to gamble that mission on a team that’s still figuring out the basics? Working with specialists lets you focus on your vision and your users, while they handle the heavy lifting of making sure the tech stands up to both market pressures and religious scrutiny.

Mobile Banking Application Design by Shakuro

Final Thoughts

And so, we are at the end of the line. We have traveled this journey with you, from the early days of walking that path with the whiteboard sessions, where Murabaha and Musharakah were concepts in your mind trying to find their way in. And we have reached the point where we have created a live and scalable solution that people are using every day.

If there is one thing I want you to remember, it is that the creation of Shariah-compliant banking software is a dance between technology and philosophy.

You start with the Islamic financial model: no interest, a willingness to share risk, and a strong connection to assets. And that choice resonates throughout every part of the project. It is the driver behind every architecture choice, pushing you to build solutions that are based on asset ownership, not asset movement. It shapes your development, where every line of code has to respect ethical boundaries. Finally, it defines your deployment, launching a product that stands on a foundation of integrity rather than just profit.

But these platforms build transparency and trust. When a user opens your app and sees exactly how their money is being used, knowing it’s free from exploitation or forbidden industries, that creates a loyalty you just can’t buy with marketing spend.

This isn’t a space for guesswork, though. Partner with islamic banking software developers who get it. Work with a team that understands the nuance of Shariah law as well as they understand Kubernetes and React. Let’s make it happen.