For those who prefer to listen rather than read, this article is also available as a podcast on Spotify.

Contents:

Users expect instant, invisible payments but also full control. Regulators are breathing down your neck. And somehow, you’ve still got to make onboarding feel like TikTok. Payment app development is no easy deal—there are compliance rules, heavy competition, sensitive data operations, pains of the target audience, trends, and whatnot.

But still, it’s totally doable. This field is not just for the usual suspects with VC backing and in-house compliance teams. With the right stack, the right team, and a few hard-won shortcuts, you can build something lean, secure, and actually useful.

In this piece, I’ll walk you through what actually matters: the tech, the traps, and how to focus on what users really care about.

Introduction to Payment App Development

Money moves fast these days. Not in the clinking-coin, paper-bill sense, but in taps, swipes, and split-second approvals across screens. So payment apps are becoming the main way people exchange value. And if you’re a founder or product person watching this space, 2025 and the upcoming years might be your best shot yet to jump in because the timing’s finally right.

What Is a Payment App?

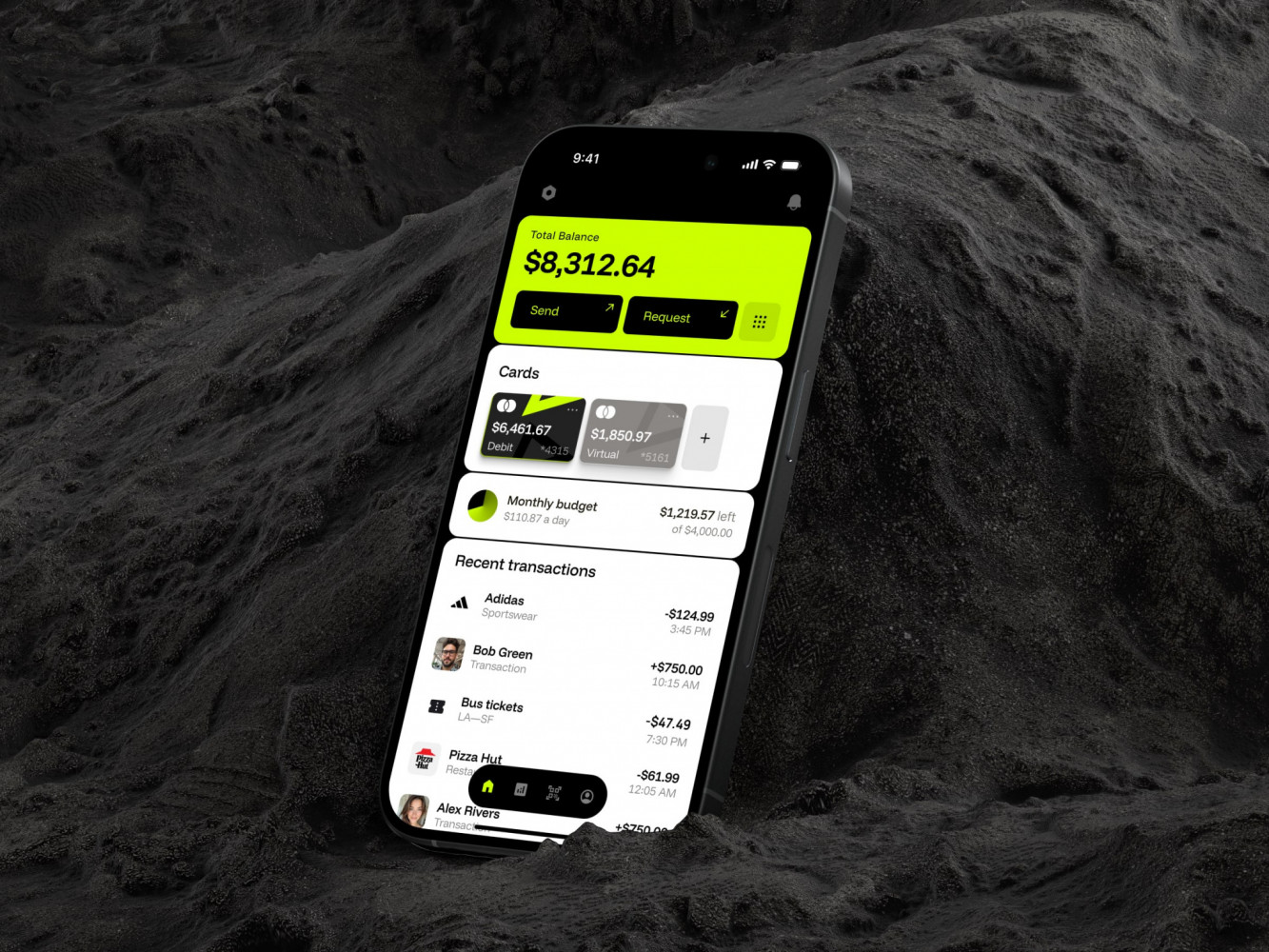

At its core, a payment app is a digital tool that lets people send, receive, or manage money without cash or checks. Just like Venmo, Zelle, or even WhatsApp Pay, they turn your phone into a wallet you don’t have to physically hold.

Modern apps often blend features like digital wallets (where you store balances or cards), transaction histories, bill splitting, QR-based payments, and loyalty programs. Some go further, offering micro-investing, BNPL (buy now, pay later), or crypto top-ups.

And yeah, while “fintech” sounds like buzzword bingo, it’s really just shorthand for “finance + tech working together.” A peer-to-peer payment app sits right at the heart of that mix, where convenience meets regulation, UX meets security, and your business meets real user need.

Why Payment Apps Are Critical in 2025

This year is a tipping point. Digital payments have gone from “nice to have” to “why would you do it any other way?”

According to Statista, more than 60% of global consumers now use at least one digital payment method weekly. In emerging markets like India, Brazil, and Nigeria, mobile money adoption is exploding, often leapfrogging traditional banking altogether. Even in places like the U.S. or Germany, where cash clung on stubbornly, habits shifted hard during the pandemic and never looked back.

Small businesses, like the food trucks, tutors, and indie designers, are ditching Square terminals for app-based invoicing and instant payouts because getting paid instantly changes cash flow. Add to that rising demand for embedded finance, and you’ve got a whole new layer of opportunity.

Market Trends and Growth in P2P and Digital Payments

Global P2P payment volume is projected to hit $10 trillion in 2026. Last year alone, mobile wallet transactions surpassed $15 trillion worldwide, jumping from just $4 trillion in 2020.

What’s driving it? A few things:

- Gen Z and millennials basically flinch at handing over physical cash.

- Real-time payment rails like FedNow (U.S.), Pix (Brazil), and UPI (India) have slashed settlement times from days to seconds.

- Super apps (Grab, WeChat, Gojek) proved that payments stick when bundled with everyday services like rides, food, and shopping.

Most of these systems are now built on open, API-first infrastructures. You don’t need a banking license to start. You can plug into modern providers like Stripe, Adyen, or even crypto rails like Circle and layer your own UX, your own niche, your own magic on top.

By the way, the biggest opportunities aren’t always in competing head-on with PayPal. Sometimes it’s in verticals, for example, a mobile payment software just for gig workers splitting tips.

Mobile Banking App by Conceptzilla

How to Choose the Right Type of Payment App

Standalone Payment Apps

These are the “pure-play” P2P apps, like Venmo in its early days, or Cash App before it added stocks and Bitcoin. They don’t live inside a bank, a social network, or an OS.

The upside is total control. You own the user experience, the brand, the data. You can move fast, experiment with features (like social feeds or cashback rewards), and even layer on financial services later.

The downside is you’re starting from zero trust. Convincing someone to link their bank account to a new app they’ve never heard of is a challenge. Plus, you’ll need serious backend plumbing: KYC/AML checks, fraud detection, liquidity management, and payout rails. Definitely not a weekend hackathon project.

Best for: Founders with fintech experience, strong compliance partners, or a killer niche.

Bank-Centric Payment Apps

Compared to the first ones, these peer-to-peer payment apps aren’t independent. They are either built by a bank or tightly integrated with one. For instance, Zelle or Europe’s many bank-branded instant payment apps using SEPA Instant Credit Transfer.

If you’re a bank or partnering closely with one, this route gives you instant credibility, existing customer bases, and smoother regulatory pathways. Users already trust their bank with their money, so adoption can be faster.

But you’re also stuck in bank time. Change moves slowly. Innovation is often bottlenecked by legacy systems or internal politics. And if you’re a startup trying to partner with a bank? Good luck navigating that maze without a warm intro and serious patience.

Best for: Fintechs with banking partnerships, regulated entities, or teams building B2B solutions for financial institutions.

Social Media-Based Payment Services

Paying your friend back without leaving Instagram DMs. Sounds like a dream.

Platforms such as Meta (Facebook Pay, now rebranded under Meta Pay) and Snapchat have dabbled in this, with mixed success. The idea’s powerful: reduce friction by removing app-switching. But it only works if the platform wants to push payments and if users actually trust sending money through a space they associate with memes and stories.

In 2025, this model of fintech app development is gaining more traction outside the West. In Southeast Asia and Latin America, where super apps dominate, social + payment combos feel natural. But in the U.S., it’s still a tough sell unless you’ve got deep platform access, which, let’s be honest, most startups don’t.

Best for: Teams building inside ecosystems with open payment APIs or those targeting markets where social commerce is already mainstream.

Mobile OS Payment Services (Google Pay, Apple Pay, Samsung Pay)

Apple Pay and Google Pay act as digital wallets that store cards and enable contactless payments in stores or in-app.

As a builder, you plug into them. Their value is instant familiarity, strong security (thanks to tokenization and biometrics), and massive user bases. Over 70% of the U.S. smartphone users have Apple Pay or Google Pay set up, even if they don’t use them daily.

As a trade-off, you’re ceding part of the experience. You can’t customize the checkout flow much, and you’re at the mercy of OS updates or policy changes. Still, for most e-commerce or marketplace apps, supporting these is non-negotiable.

Best for: Practically every mobile payment software that accepts payments, just don’t think of them as your core product unless you’re Apple or Google.

Crypto Payment Applications

Crypto payments had a wild ride. After the 2022 crash, a lot of folks wrote them off. But in 2025, they’re quietly making a comeback, just not the way early hype suggested.

Forget paying for coffee in Bitcoin. Instead, stablecoin-based wallets like those from Circle or Coinbase are offering near-instant, low-cost cross-border P2P transfers. For example, a freelancer in the Philippines getting paid by a client in Berlin in USDC, settled in seconds, with fees under 1%.

The audience for blockchain payment apps is still niche, though. Tech-savvy, globally mobile, often unbanked or underbanked, but growing. And new regulatory clarity in places like the EU and Singapore is helping.

That said, you’ll need crypto compliance chops (VASP licenses, wallet monitoring, etc.), and mainstream users still eye this space with suspicion. Not beginner-friendly, but potentially high-impact.

Best for: Founders focused on global remittances, Web3-native communities, or borderless gig economies.

Messaging Apps with Built-in Payments

WeChat Pay in China, WhatsApp Pay in Brazil and India, Telegram’s new mini-wallets turn conversations into transactions.

Unlike social media payments, messaging payments feel functional. Splitting rent? Sending money to family? Paying a small vendor? All happen right in the chat.

However, for this type of P2P payment app development, you need either massive scale (like WhatsApp) or deep local integration (like Line Pay in Japan). If you’re a startup trying to build your own messaging app with payments, honestly, that ship has sailed. But if you’re building on top of platforms that offer payment APIs (like WhatsApp’s Business Platform), there’s real opportunity, especially in emerging markets.

Best for: Builders targeting high-engagement, chat-first markets, especially in Asia, Africa, and Latin America.

Fintech Mobile App UI Design by Shakuro

How to Define Core Features for Your Payment App

You’ve picked your app type, great. Now you need to figure out what it actually does. It’s tempting to cram in every bell and whistle, especially when you’re staring at competitors with 20 tabs of features. However, your first version shouldn’t try to do everything. It should do a few things so well that people can’t stop using it.

Peer-to-Peer (P2P) Transactions

This is the bread and butter of most payment apps: sending money to friends, family, or that guy who covered your lunch. But “just send money” is deceptively complex.

There should be:

- Contact lookup (by phone, username, QR code)

- Real-time notifications

- Transaction limits and receipts

- Reversal or dispute handling

Payment app security is crucial from day one. Apart from encryption, you need behavioral fraud detection (like flagging a $500 send from a user who usually sends $20). In my experience, users forgive a slow app, but they never forgive a stolen account.

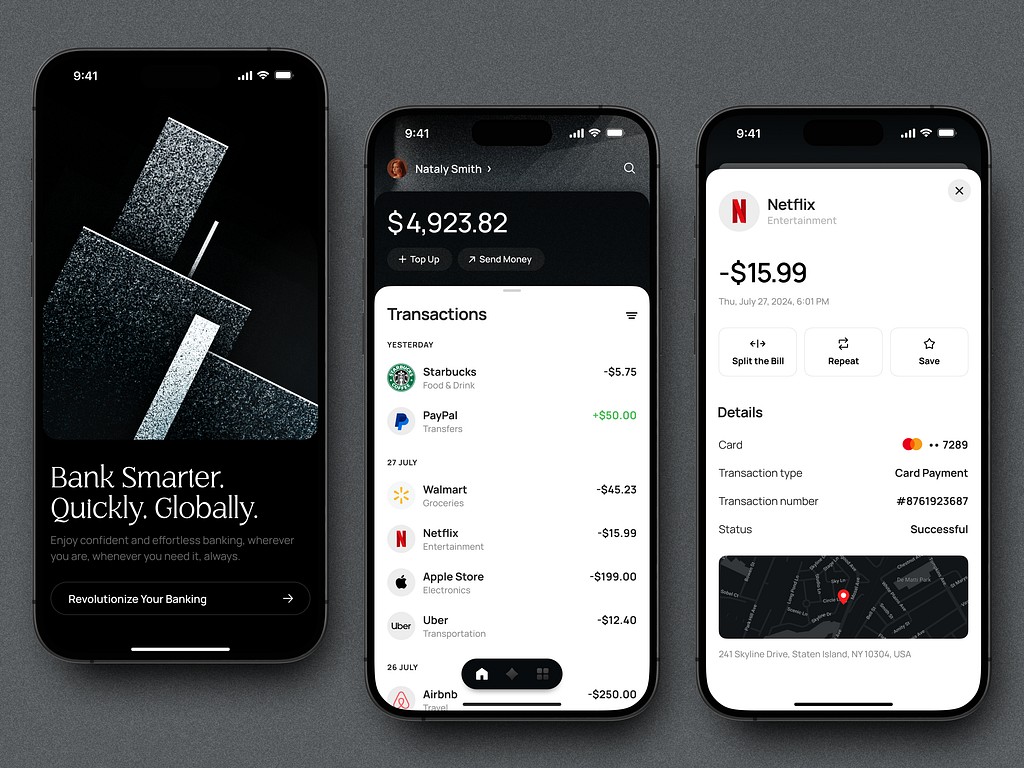

Digital Wallet Functionality

A wallet is a place to store money, and, moreover, it’s your user’s financial dashboard. At minimum, it should let people:

- Check their balance instantly

- View transaction history with search/filter

- Add or remove linked bank accounts or cards

- Hold balances in multiple currencies

But don’t over-engineer this early on. No need to make digital wallet development more complex with sub-accounts or budgeting buckets on day one. Instead, make it feel alive with real-time updates, clean visuals, and no “processing” spinners that last 10 seconds.

Point-of-Sale (POS) Integrations

If you’re eyeing small merchants, like food trucks, salons, or indie shops, you’ll need to work with real-world payment systems. That means including QR code payments, APIs for merchant onboarding, and Integration with common POS systems.

You don’t have to build your own terminal. But if a vendor can’t easily accept payments from users, your app becomes “just for friends,” not a real payment tool.

Spending Analytics and Reporting

People love insights if they’re useful. A flashy pie chart of “coffee vs. groceries” might look nice, but what people really want is “How much did I spend this week?” or “Am I over budget?”

Start simple: a clean dashboard with spending by category, date range filters, and exportable reports (for freelancers filing taxes, for example). Fancy AI-driven predictions should be saved for V2.

Invoice and Bill Payments

Recurring payments = sticky users. If someone can pay their electricity bill, subscription, or freelancer invoice inside your app, they’ll open it monthly, maybe even weekly.

Key payment app features to nail are saved payees, scheduled/automated payments, and bill reminders. They blur the line between P2P and B2C, but in 2025, that’s where the value is: becoming the hub for all personal finance.

Multi-Factor Authentication, OTPs, and Secure IDs

If your app handles money, you are an easy target. So security isn’t a “nice-to-have”, it’s your license to operate.

At launch, you absolutely need:

- Biometric login (Face ID, fingerprint)

- One-time passwords (OTPs) for sensitive actions

- Session timeouts

- Device recognition

Also, there are different compliance rules: PSD2 in Europe, GLBA in the U.S., and local AML rules everywhere. The launch can be delayed by months because you treat security as an afterthought.

Customer Support and Chatbots

When money’s involved, panic is real. A user sees a weird charge? They’ll rage-tap support 12 times. So you can’t afford slow email replies. Start with an in-app chat, AI assistant for common issues, and clear status pages.

Also, add a “transaction help” button next to every payment. It reduces support tickets by, like, 40%, based on what I’ve seen with early-stage apps.

Automatic Currency Conversion

If your users travel, freelance globally, or have family abroad, multi-currency support isn’t optional. Transparency here builds massive trust. During payment app development, you don’t need to strive to be Revolut on day one, but you should:

- Show real-time exchange rates

- Let users hold and send in multiple currencies

- Auto-convert only when needed

Voice and Messaging Interfaces

This one’s forward-looking but worth considering, especially if you’re targeting accessibility or older users.

No need to build Siri-level AI. But even basic voice commands or message-based payment approvals (like replying YES to confirm $15 to Alex) can be a huge differentiator for inclusive design. For example, when people have disabilities.

Abyss Crypto Management App by Conceptzilla

How to Develop a Payment App: Step-by-Step Process

Step 1: Discovery and Market Research

Going in blind right into the development process is unwise. You need to spend time listening and thinking about your goals. Ask yourself:

- Who exactly are you building for? (“Everyone” is not an answer. Be specific: “freelancers in Mexico City” or “college roommates in Berlin”)

- What do existing apps get wrong for them? (Venmo’s too social? Bank apps too slow?)

- What’s your unfair advantage? (Local partnerships? A smarter UX? Lower fees?)

Then, study your competitors, regional players too. In Nigeria, it’s Opay; in Brazil, it’s Pix-enabled apps; in Southeast Asia, it’s all about Grab and Gojek. Moreover, talk to actual users. A 15-minute call with someone who splits bills weekly will teach you more than three months of internal brainstorming.

Step 2: Defining Business Model and Regulatory Compliance

This is where dreams meet paperwork and often shatter. Or reshape into something more functional.

First, how will you make money? Here are some common models that still work in 2025:

- Transaction fees (small % on P2P or merchant payments)

- Freemium features (instant transfers for a fee, free standard)

- B2B SaaS (white-label payment infra for small businesses)

- Interest on float (if you hold user balances, only if licensed)

Now, the harder part: payment app compliance. You’ll likely need to deal with:

- KYC (Know Your Customer): Verify user identities

- AML (Anti-Money Laundering): Monitor for suspicious activity

- PCI DSS: If you touch card data (though most avoid this by using tokenization via Stripe, etc.)

- Local licenses: Money transmitter licenses in the U.S., EMI licenses in Europe, etc.

Don’t wing this and talk to a fintech lawyer early, even if it’s just a one-hour consult. Many teams waste months because they assumed “it’s just P2P, so it’s fine.” But it’s rarely just P2P in regulators’ eyes.

Step 3: App Architecture Design

Now it’s time to sketch the bones of your system. Your backend needs to be modular with separate user auth, transaction engine, compliance layer, and reporting. As for the design, the backend has to be event-driven because payments are async. So plan for retries, failures, and reconciliation.

If you want the peer-to-peer payment app to be scalable, then use cloud platforms like AWS, GCP, or Azure with auto-scaling. To make it resilient, apply idempotency keys for duplicate prevention, circuit breakers, etc.

Last but not least, avoid storing raw card numbers or SSNs. Instead, use vaults (like AWS KMS or dedicated providers like Basis Theory).

Step 4: UX/UI Design and Prototyping

Payments are emotional. A confusing flow = abandoned transfers. A slow load = lost trust. That’s why it’s better to start with user flows. For example, how does a new user send money in under 30 seconds? What happens when a transfer fails?

After answering these questions, build clickable prototypes and test them with real people. Watch where they hesitate. And don’t forget accessibility: dynamic text sizing, voiceover support, and color contrast. It’s often legally required.

Step 5: Development and Backend Implementation

When the app architecture is designed, time to transform that into code. For frontend, leverage React Native or Flutter, unless you’re Apple or Android-only. Keep everything lightweight; payment apps shouldn’t feel like video games.

Next, the backend. From Shakuro’s experience, it’s better to opt for battle-tested languages and frameworks, like Node.js, Go, or Python. Start with REST, maybe add gRPC later.

As for APIs, You need to integrate with payment processors such as Stripe, Adyen, or local rails like UPI or Pix. The same goes for KYC providers (Onfido, Jumio) and fraud tools (Sift, Arkose).

In terms of databases, there are several variants for payment app development. We usually go for PostgreSQL or MongoDB. Use separate read/write paths for performance and always log audit trails—immutable, timestamped, and signed.

One thing to pay attention to: mock your payment integrations early. Nothing kills momentum like waiting for a sandbox account that takes two weeks to approve.

Step 6: QA Testing, Security Audit, and Compliance Check

It’s your safety net. Apart from testing like a user, you need to test like an attacker:

- Penetration testing: Hire a third party

- Load testing: What happens when 10k users send money at once?

- Edge cases: Negative amounts, timezone mismatches, failed bank callbacks

- Compliance validation: Ensure KYC flows actually block sanctioned users

Also, run your app through accessibility checkers and localization tools if you’re going multi-region. Document everything while doing so, for your future self, your investors, and the auditor who will come knocking.

Step 7: Deployment and Launch

Finally, go live, but carefully. Deploy to production with feature flags and roll out to 1% of users first. If you submit to the App Store and Play Store, expect delays. Apple especially scrutinizes payment apps. So have your privacy policy, terms, and compliance docs ready.

After the launch, set up real-time alerts for failed transactions, latency spikes, or fraud signals. You can use tools like Datadog, Sentry, or open-source alternatives. Not to mention that you should have a backup plan for the sake of your payment app security.

Step 8: Support, Maintenance, and Continuous Improvement

Keep monitoring crash rates, payment success rates, and support tickets. Together with reviews, this will give you insights into what people think about your app. Implement the feedback you received in short iterations, and don’t forget about compliance. Set calendar reminders to review AML policies quarterly.

By the way, when gathering feedback, measure what matters: active senders, repeat usage, and net promoter score.

Mobile Banking App by Shakuro

How to Apply Best Practices in Payment App Development

Security-First Approach

A “security-first” mindset means baking protection into every layer, starting from the very design stage. But do it well:

- End-to-end encryption for all sensitive data in transit and at rest

- Tokenization instead of storing raw card or bank details (Stripe, Adyen, or your payment rail handles the heavy lifting)

- Zero-trust architecture: Assume every request is hostile until proven otherwise

Then layer on proactive defenses like real-time fraud scoring and automatic session revocation after suspicious activity. Never forget: payment app compliance is table stakes. PSD2, GDPR, CCPA, local AML laws are your credibility.

Open and Scalable Architecture

Your app might start with 500 users in one city, but design it like you’ll have 5 million across three countries next year. Because retrofitting scalability into a monolith is painful and expensive.

As I’ve mentioned before, go for modular, API-first design:

- Break your system into bounded contexts: auth, wallet, transactions, compliance, notifications

- Use event-driven messaging (like Kafka or RabbitMQ) so services can evolve independently

- Choose cloud infrastructure (AWS, GCP) that auto-scales, especially for transaction spikes during holidays or sales

Also, keep your integrations loosely coupled. Need to swap KYC providers? Add a new payout rail? You shouldn’t have to rewrite half your codebase. Use adapter patterns and abstract interfaces early. Log everything, but structure your logs so you can trace a single transaction across services. You’ll need it when something goes sideways.

UX/UI Flexibility and User-Centric Design

People don’t want to “use mobile payment software.” They want to send money and get on with their lives. So your job is to disappear. That means reduce cognitive load and predict user needs. Make it easy to cancel, correct, or contact support before the money leaves.

Flexibility matters too. Not everyone reads left-to-right. Not everyone uses a touchscreen. That’s why, keep all this in mind and build with dynamic layouts that adapt to language direction. Some people have bad eyesight, so there should be font scaling and color contrast for accessibility. Not to mention that the Internet connection can be unstable, therefore, the app needs to be offline resilient.

AI and Machine Learning Integration

AI means smarter decisions behind the scenes when speed and security collide.

Three high-impact uses in 2025:

- Fraud detection: Instead of blanket blocks, use ML models to score risk in real time. Flag unusual behavior.

- Cash flow insights: For users with wallet balances, predict “You’ll run low by Thursday, want to auto-top-up?”

- Personalized nudges: “You usually split dinner with Sam on Fridays, send now?”

However, don’t over-automate. Humans should always override AI decisions, especially when money’s involved. Your models should undergo a regular audit because bias in fraud detection can lock out entire user groups.

Continuous Updates and Feature Expansion

Your V1 is just the beginning. The real work starts after launch. That’s why having a certain rhythm is so important. You don’t want your users to wait months for crucial tweaks. At the same time, releasing them daily is somewhat inefficient.

I’d recommend you follow a pattern common for custom payment app development:

- Weekly: Review crash reports, support tickets, and failed transactions

- Monthly: Release small UX tweaks or performance fixes

- Quarterly: Add one meaningful feature based on user behavior

Use feature flags to test new flows with 5% of users before rolling out widely. Measure impact: Did that new “split bill” button actually increase group transactions? Or just add clutter? Also, keep your tech debt in check. Schedule refactoring sprints like you schedule feature work.

How to Overcome Challenges in Payment App Development

Security and Fraud Prevention

If there’s one thing that can sink your app before it even floats, it’s a breach or even the perception of weak security.

How to avoid that? Start with PCI DSS compliance, even if you think you’re “just doing P2P.” If your product ever touches card data, even indirectly, you’re in scope. The smart move, of course, is to not touch it at all and use tokenization through Stripe, Adyen, or similar. So raw card numbers never hit your servers. That alone knocks you down to SAQ A, the lightest PCI burden.

Beyond that:

- Encrypt everything: Not just in transit (TLS 1.3+), but at rest using hardware-backed key management (like AWS KMS or Google Cloud HSM).

- Implement rate limiting and anomaly detection. Someone trying 50 sends in 2 minutes? Freeze it, verify it.

- Use behavioral biometrics: Not just “Is this the right fingerprint?” but “Does this user usually send $500 at 3 a.m. to a new contact?”

Run red team exercises at least once a year. You’d be surprised how often a clever intern finds a way to replay a transaction or bypass a confirmation screen. Better them than a real attacker.

Regulatory Compliance and Legal Issues

Nobody wants to talk about this at pitch competitions, but it’s the make-or-break layer.

You’ll likely juggle:

- KYC (Know Your Customer): Verify identities upfront. Use trusted providers like Onfido or Sumsub, but test their accuracy in your target regions. For example, they’re great in the U.S., and spottier in parts of Africa or Southeast Asia.

- AML (Anti-Money Laundering): Monitor transactions, screen against sanctions lists, and file SARs (Suspicious Activity Reports) when needed.

- GDPR / CCPA: If you store user data, you need clear consent, data deletion workflows, and privacy-by-design architecture.

- Local money transmission laws: In the U.S., that means 48+ state licenses. In the EU, you will need an EMI (Electronic Money Institution) license. In India, it’s NPCI approval for UPI access.

In any case, the best decision is to hire a consultant for payment app compliance early, even part-time. And keep a compliance roadmap. This way, you will avoid potential fees and damage to your reputation.

Integrating Multiple Payment Systems

Your users just want to send money in a fast, cheap, and preferred way. They aren’t interested in any connection issues. So you’ll need to stitch together a messy patchwork: cards, bank transfers, mobile wallets, maybe even crypto.

The key is to abstract everything behind a unified payments layer. For example:

- Create a PaymentMethod interface in your code. It can be a card, a Pix key, or a USDC wallet; your core transaction logic stays the same.

- Use orchestration services, like Modulr, Railsbank, or Stripe Connect, that already handle cross-rail routing.

- Never hardcode payment logic. Tomorrow, you might need to add M-Pesa or PromptPay, so your architecture should welcome it.

Also, test every combo. For instance, from card to bank transfer, from wallet balance to crypto payout, etc.

Ensuring Scalability and Performance

Nothing kills trust faster than “Payment failed” during a holiday rush or a viral moment. Scalability should be a part of your product promise.

Start with stateless services, so you can spin up more instances during traffic spikes. Database sharding by user ID or region will protect your system from being tanked by a single hot account. Also, use webhooks and status polling for asynchronous processing. It will help you avoid blocking the UI while waiting for bank confirmation.

Cloud platforms (AWS, GCP) handle a lot in P2P payment app development, but optimize your hot paths:

- Cache frequently accessed user profiles or transaction limits

- Use idempotency keys on every API call, so if a user taps “send” twice, they don’t pay twice

- Monitor p99 latency, not just averages. That one slow user ruins the experience for everyone

To keep high levels of performance, regularly simulate failure. Run chaos engineering drills: kill a database node, throttle your payment gateway, and see if your app degrades gracefully. If it doesn’t, fix it before real users do.

User Adoption and Trust Building

You can build the most secure, compliant, scalable app in the world, but if no one uses it, it’s just expensive code.

Trust is earned, especially with money. So you need to be transparent. Show fees upfront. Explain why you need their ID. Say how long transfers take—no “instant” promises if it’s really “up to 2 days.” Educate people gently on the security. Use onboarding tooltips like “Your money is protected by bank-level encryption” or “We never sell your data.” They will trust your services more.

In the beginning, UX can be spotty, so launch in one small community. For instance, university students, freelancers on a specific platform, etc. This allows you to polish the experience before going wide. The social proof like “Over 10,000 users in Lagos trust us” works better than “cutting-edge blockchain tech.” Real numbers > buzzwords.

Finally, something obvious, support is a trust feature. A fast, human reply to “Where’s my money?” can turn a panicked user into a loyal advocate.

Mobile Banking App by Conceptzilla

How to Estimate Cost and Timeline for Your Payment App

Factors Affecting Cost

There’s no flat “price per product.” Your payment app development cost swings wildly based on these key levers:

- App type: A standalone P2P app like early Venmo is cheaper than a bank-integrated one or a global multi-currency wallet.

- Core features: Just P2P + wallet? Maybe $80k–$150k. Add invoicing, POS QR payments, multi-currency, and analytics? You’re easily looking at $250k+.

- Compliance burden: Operating in one country is simpler than launching in the U.S., EU, and Southeast Asia simultaneously, each with its own licensing, KYC rules, and data laws.

- Integrations: If you need to plug into local systems like India’s UPI, Nigeria’s NIP, or Europe’s SEPA Instant, you’ll need specialized dev effort and often local partners.

- Platform choice: Going iOS + Android + web backend? That’s 2–3x the frontend work. Cross-platform saves money, but not if you need deep platform-specific features like NFC for in-store payments.

And don’t forget hidden costs, for example, payment processor fees per transaction, security audits ($10k–$30k per year), and legal/compliance consultants ($150–$300/hour). The more “real money movement” you enable, the more expensive it gets to operate.

Average Development Timeline by App Complexity

Timelines consist of testing, compliance checks, app store reviews, and waiting for banking partners to reply, which, honestly, can take weeks.

Here’s a realistic breakdown:

🔹 Simple P2P App (MVP)

- Features: User signup, bank/card linking, send/receive money, basic wallet, push notifications

- Tech: One country, one payout rail (for example, ACH or local instant payment system)

- Timeline: 4–6 months

- Team: 1–2 backend devs, 1 mobile dev, 1 designer, part-time compliance advisor

- Cost range: $80,000–$150,000

Example: A campus-focused app for splitting rent among students in a single country.

🔹 Medium-Complexity App

- Features: Multi-currency support, invoice payments, basic analytics, merchant QR codes, enhanced security (biometrics, MFA)

- Compliance: 2–3 jurisdictions, basic KYC/AML

- Timeline: 6–9 months

- Team: 3–4 devs (frontend, backend, DevOps), UX designer, compliance lead

- Cost range: $180,000–$350,000

Example: A freelancer-focused app that works across the U.S. and Mexico with USD/MXN support.

🔹 Complex, Full-Scale Payment Platform

- Features: Global payouts, crypto-fiat conversion, POS integrations, advanced fraud AI, regulatory dashboards, multi-language support

- Compliance: Full KYC, AML monitoring, PCI DSS, money transmitter licenses

- Timeline: 10–18 months or more, often with phased rollout

- Team: 8–12+ people, including legal, risk, and ops

- Cost range: $500,000–$1.5M+

Example: A remittance-focused app targeting immigrant communities across 5+ countries.

Keep in mind, though, that App store approvals for a peer-to-peer payment app take longer. Apple may ask for your compliance docs, and Google might request extra fraud safeguards. That’s why you should always pad your launch date by 3–4 weeks.

Crypto Trading Mobile App by Conceptzilla

Budget Optimization Tips

You don’t need millions to start, but you do need smart trade-offs. Here are some tips I can give you based on Shakuro’s experience with MVPs and startups:

✅ Start with a razor-focused MVP

Don’t build “the next Revolut.” Build “the easiest way for gig workers in Lisbon to split gas money.” Nail that, then expand. Every extra feature in V1 adds 2–3 weeks of dev time and ongoing maintenance. And costs, to be honest.

✅ Outsource strategically but keep core in-house

Outsource UI design, QA testing, and basic mobile dev. Keep in-house or tightly controlled backend transaction logic, compliance logic, and security architecture. The reason is you can’t debug a fraud loophole through a 12-hour time zone gap.

✅ Prioritize features by risk and value

Use a simple matrix:

- High user value + low dev risk → Build first (clean send flow)

- High regulatory risk → Address early (KYC flow)

- Nice-to-have + high cost → Defer (voice payments, crypto staking)

✅ Leverage modern infrastructure

Leverage managed services:

- Auth: Firebase Auth or Auth0

- KYC: Onfido, Jumio (pay per verification with no upfront build)

- Payments: Stripe, Adyen, or local processors with good APIs

This cuts dev time by approximately 30–50% vs. building everything from scratch.

✅ Plan for post-launch costs

Your app isn’t “done” at launch. Apart from custom payment app development, budget for:

- Monthly cloud bills. They can spike with user growth, by the way

- Transaction monitoring tools

- Ongoing compliance updates

- Customer support, even if it’s just a part-time person

Case Studies and Success Stories

Venmo: The “Social” Bet That (Almost) Backfired

What they did:

Launched in 2009 as a simple SMS-based P2P app, Venmo pivoted hard in the early 2010s by adding a public feed like Facebook for payments. You could see friends paying for brunch, splitting rent, and even tipping DJs, all with emojis and comments.

Why it worked at first:

- Perfect timing: Millennials were tired of awkward cash exchanges.

- The feed made payments fun. It went viral on college campuses.

- Braintree and later PayPal gave them massive infrastructure backing.

Challenge:

The social feed became a liability. People accidentally exposed rent payments, medical bills, and illicit transactions. Privacy advocates slammed them. By 2018, Venmo made feeds private by default, which was a necessary retreat.

Lesson for builders:

Novelty drives early growth, but trust drives retention. If you’re adding “fun” features during P2P payment app development, never compromise financial privacy. And always give users granular control. Venmo survived because PayPal absorbed the fallout, but some other startup might not be so lucky.

Pix: The Government-Backed Game Changer

What they did:

In 2020, Brazil’s central bank launched Pix. It was a free, instant, 24/7 payment system open to banks, fintechs, and even individuals. Not an app itself, Pix became a public infrastructure anyone could build on.

Why it exploded:

- Zero fees for individuals

- QR codes + phone/email/CPF keys made onboarding dead simple

- Instant settlement when money moves in seconds, even on weekends

- Mandatory adoption. All banks with >500k customers had to support it

The result is 80% of Brazilian adults were using Pix within two years. Apps like Nubank, PicPay, and Mercado Pago raced to integrate it, and their user bases exploded.

Lesson for builders:

Sometimes the biggest opportunity isn’t building the rails—it’s building the best train on them. If your country has or is getting a real-time payment system (like UPI in India, Instant Payment in EU, FedNow in U.S.), build on top of it. Don’t reinvent the wheel. Just make the smoothest ride.

SteadyCash

SteadyCash is a fintech startup that approached us for a collaboration. They needed a convenient, fast mobile banking app for iOS.

What we did:

Our team created a responsive app aimed at young and middle-aged people (who were the target audience), with intuitive navigation and demanded features.

Why it worked:

- Helped users reach their goals in a few taps

- Detailed analytics and clear expenses representation

- Easy-to-grasp UI/UX design, even for non-technical users

- Built-in digital wallet for quick transactions

Lesson for builders:

You can win a place under the sun by building a more convenient, easy-to-use app than other competitors. Easy access, responsiveness, and one-tap actions sometimes attract greater than pro-level features. In-depth market research showed us hidden opportunities and niches that we leveraged to enhance digital wallet development.

Mobile Banking App by Coneptzilla

How to Choose the Right Payment App Development Partner

Criteria for Selecting a Trusted Development Company

Going by portfolio screenshots or Shopify testimonials isn’t a wise decision. For fintech apps, you need proof of financial-grade experience. Instead, look for:

- Fintech-specific track record: Have they built apps that move real money, not just e-commerce checkouts? Ask for case studies with transaction volume, compliance scope, and payout integrations.

- Security & compliance literacy: They should speak KYC, AML, PCI DSS, and GDPR like second languages. Bonus if they’ve worked with regulated entities (banks, EMIs, MSBs).

- Modern, modular architecture: Avoid teams that push monolithic Rails apps for everything. You need microservices, event-driven design, and cloud-native thinking (AWS/GCP with proper IAM).

- Long-term thinking: Do they talk about monitoring, fraud hooks, and scalability or just “launch fast”? The best partners think like co-founders, where your success equals their success.

- Transparency in process: Daily standups? Shared Jira? Clear sprint reviews? If they’re secretive about workflow, run.

Key Pitfalls to Avoid

Some red flags are obvious, while others sneak up on you. Watch out for:

❌ They’ve done payment integrations but it’s only Stripe Checkout

Adding a “Pay with Card” button isn’t the same as building a P2P ledger with reconciliation, dispute handling, and balance management. Push the agency for details.

❌ Offshoring with zero time-zone overlap

Payment apps need tight feedback loops, especially during QA and compliance testing. If your team sleeps while they code, you’ll miss critical context. A 4–6 hour overlap is the bare minimum.

❌ Fixed-price contracts for complex fintech app development

“$80k for a Venmo clone” is a fantasy. Payment apps evolve as you learn about regulations and user behavior. Go for time-and-materials with clear milestones, not a rigid scope.

❌ No in-house security or DevOps

If they outsource infra or security “to a specialist,” that’s a handoff waiting to fail. You need embedded expertise.

❌ Over-reliance on junior devs

Fintech isn’t the place for “learning on your dime.” Demand to meet the actual engineers who’ll work on your project.

Questions to Ask Before Hiring

What additional questions should you ask besides those about the portfolio? Well, there are hundreds of them, but here is the short list:

“Can you walk me through a payment app you built that handled real user funds?”

→ Listen for specifics: idempotency, webhook retry logic, and reconciliation jobs.

“How do you approach KYC/AML in your architecture? Do you use third-party providers, and how do you handle user verification states?”

→ If they say, “We just collect ID photos,” that’s a red flag. You need workflow states (pending, verified, rejected) and audit trails.

“What’s your strategy for scaling during traffic spikes? Have you load-tested a payment system before?”

→ Good answer: “We use Kubernetes autoscaling, database read replicas, and simulate 10x traffic with Locust.”

→ Bad answer: “Our servers are powerful.”

“How do you ensure PCI compliance if we ever touch card data, even indirectly?”

→ Best answer: “We avoid touching card data entirely using tokenization. But if needed, we isolate it in a PCI-scoped microservice with annual audits.”

“Who will be my main point of contact, and are they technical?”

→ Avoid sales-only PMs. You need someone who understands idempotency keys and OAuth flows.

“Can I speak to a past client who built a fintech product with you?”

→ If they hesitate or offer only non-fintech references, walk away.

Stocks Trading Mobile App by Conceptzilla

Conclusion

Digital wallet development is about stepping into one of the few spaces where real utility meets massive, global demand. People expect and rely on digital money every day. And if you can solve a genuine pain point (splitting bills, paying freelancers, sending remittances home) in a simple way, you’ve got a shot at something sticky, scalable, and seriously valuable.

Why Payment App Development Is Essential in 2025

We’re past the tipping point. Digital payments aren’t “the future”—they’re the now.

- Over 75% of consumers worldwide used mobile payments in 2024 (Statista).

- Real-time payment rails (Pix, UPI, FedNow) are live in over 70 countries, unlocking instant, low-cost transfers.

- Users increasingly reject apps that don’t offer seamless P2P or embedded payments.

If your product involves any kind of value exchange, not having a payment layer is becoming a liability. For founders, that’s opportunity wrapped in responsibility.

Next Steps for Launching Your Payment App Project

Don’t try to boil the ocean. Start here:

- Define your niche: Who struggles to send money today?

- Pick your scope: MVP first. For example, P2P + wallet + one payout rail.

- Talk to a fintech lawyer: Even a 1-hour call can save months of regulatory detours.

- Choose a technical partner with real payment experience.

- Prioritize security and compliance from Day 1 as your core product promise.