If there is something we’ve learned finance-wise for the last decade, it has to be how vulnerable and unstable the current banking model is. The world financial crisis left no unaffected. Even if you think your life alone did not get affected by it, the environment you live in, definitely did.

“Clean or dirty, the ocean remains as one” – Being As An Ocean

The disturbance of the world economy left the banking industry in a precarious position. On one hand, banks have to remain profitable, effective, and reliable, on the other, they require a new twist through digital technological disruption and new ways to fight the distrust.

With the power of #disruption comes the risk of becoming obscure which for the most financial institutions is unthinkable. Say what you want about innovation, but when it comes to cash, we all go oldschool. So where does the digital innovation for banking fit? Is it UX for mobile banking as the most frequent usage medium? Or perhaps, AI algorithms for better performance in services? How about Big Data processing for predictive analysis and better “readiness”? Actually, with the newest approach to growth in the banking industry, you can do it all. We’re talking modularity.

Disruption

Since the internet has touched upon everything, there is little argument regarding the advantages of that encounter. “I wish there was no internet connected to that thing.” – said no one ever. Things like availability, speed of interactions, and sheer comfort of digital operations put an all-time indentation on us that we are not willing to trade.

We are dealing with oversupply of choice. And we are terrible at it. The abundance of options made us apathetic to thoughtful consideration. This made clickbait and red flag advertising possible, ultimately devaluing the versatility of solutions available. In this reality, something as solid and reputable as a bank has to find a way to innovate and yet maintain its name and traditions.

Today, banking services are more of a middleware between users and other service providers. Different banks showcase different functionality and users have to deal with a constant tradeoff in features – something that technology has been vigorously fighting to eradicate. First, the search. It became so much easier to find a financial institution based on your own search criteria. Whether it’s the testimonials, the pricing, or even the design, we don’t need to do guesswork and ask those questions. All it takes is a smartphone.

With such availability of data, it makes sense that banks become more field-specific and focused on just a fraction of customer needs. This not only increases the efficiency of their operation but also puts them into an essential customer supply chain, thus cementing the niche, particularly in payments.

This process is called modularization.

The core of banking is the consumer segment and it is the one most influenced by the massive injection of mobile and smart technologies into something that was once a service and became an experience. All of a sudden, it became normal to hop on and off the banks using just your phone, which made banks cautious about what they offer their clients and how they do it. Things are a bit more complicated with corporate banking where it is still a game of checks and balances, mutual gain ratios, personal agreements, and history.

Image credit: Zsolt Varga | SEK

It is yet unclear what type of disruption will bring the necessary change, whether it’s going to be distributed ledgers, mobile experiences, collaborative solutions, etc., but there is something about it that makes modular banking stand out.

In modular banking, the only thing left in common with the traditional system will be the bank account itself.

The all-encompassing services will become obsolete, giving way to a healthier competitive network of providers that a customer can assemble their supply of. Perhaps, a centralized support system could come into play to furnish the traditional bank-level security and service standards.

A chance to bounce back

Since the first time technology and financial industry joined forces to create a user-focused alternative to the rigid and rusty banking service, FinTech startups filled the market with quality solutions capable of handling the same operations as legacy banks but only for a fraction of the cost.

In fact, the independent FinTech service startups were the modules of banking, but not synchronized to create a consistent experience. For example, you may pay your rent using a payment system with its own features and logic, then you do your groceries using an alternative platform because cashback, and you go to the third solution to manage loans and insurance. Each separate product is great in its own way and every module of your supply chain is customized for your specific need.

Image credit: Dana TIleva

This concept is a chance for banks to claim back some of the estate they’ve lost because of the lack of agility and delightful UX. Dealing with individual customers and small businesses in this sense is just too overwhelming, so if banks do realize there is a chance to integrate the smaller providers of agile data-driven and heavily-customized services into their ecosystem, they might reinvent themselves for the future. This especially shines in the middle-market lending segment. Smart FinTech startups took off in alternative P2P lending without the need to carry the expenses of traditional banking services and brick-and-mortar operation.

While some might think FinTech startups took away a chunk of the traditional banking services, in reality, they created an opportunity for banks to step their game up.

Institutional security being the weakest point of P2P lending can be fully provided by the traditional banks that embrace the modular reformation model. The future shows no signals of winding down the trend of disruption:

- Customer expectations brought by one product will be projected on other.

- Lifestyle services with a social following will segway into finance.

- AI will only get stronger.

- Internet of Things will redefine the way we build our own networks.

- Blockchain will remain a dark horse.

- Customer data will no longer be a wild-west commodity.

- The demand for transparency will only increase.

- Information technology giants will continue to capture new markets.

- Online marketplaces and e-commerce, especially for mobile, will continue to bulk.

Image credit: Zsolt Varga | SEK

The crucial changes that banks apply can once again stir up the case. More on that, including the 6 Disruptive banking models, is coming soon on our blog. So stay with us.

Landscape

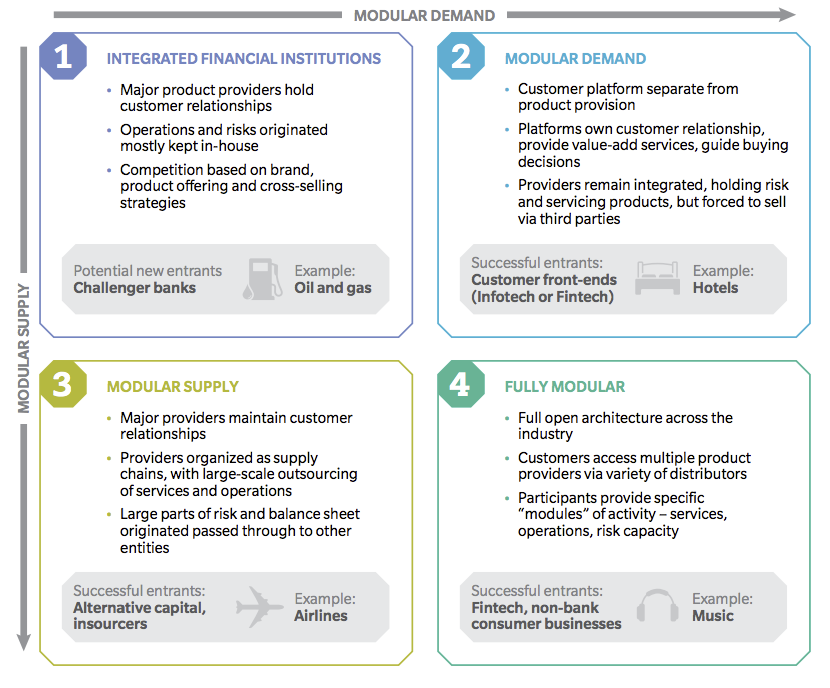

Understanding the idea of modular requires the grasp of two entities: modular demand and modular supply. Modular demand is like a multibrand shop where it’s up to the consumer to decide which products they need for a specific goal. Modular supply is like the providers of stuff for that shop. They are all independent but working in one particular logic of customer satisfaction. This has been the case for a lot of businesses so far, as the benefits of the modular approach are appreciated in retail and service providers.

The financial industry, however, still runs on the integrated model.

According to Oliver Wyman, there are four major incarnations of modularity in the financial industry: integrated financial institutions, modular demand, modular supply, and fully modular.

Image credit: oliverwyman

Integrated financial institution

This is the “umbrella” structure which means all the smaller financial services are parts of one major provider. This only works for giants on the market which can afford to roll out new products under a trusted brand. In that case, the name throttles the product before its value is publicly proven.

On one hand, this protects the user from the risky endeavors as the brand’s overall quality is projected on all of its assets. On the other hand, it gives these providers the ultimate freedom to set the standards of service, the pricing, and so on.

In Asia, this is particularly the case, as reputation is greatly appreciated in that part of the world, which makes it extremely difficult for new FinTech companies to enter the market.

With that said, the environment is changing which requires a whole new level of sensitivity and technological maturity from startups.

Modular demand

This is the type of customer-provider relationship which derives from the oversupply of choice. The customer no longer belongs to the provider’s loop. The customers are by default treated as educated and not pitched products cold-turkey style.

Modular demand is the demand of the future.

It does not imply long-term relationships as the ultimate goal but focuses on the quality and value of case-by-case interactions. Almost every startup faces the problem of nonuniqueness where the services are not invented anymore but rather, redefined. For companies starting off, one of the ways to enter the market is to become an aggregator channel for whatever industry. With no lack of providers, it’s the anonymity and security that become the desired features.

Modular supply

Demand breeds supply. A bunch of good guys who know how to craft things might not always be into a lot of organizational stuff, maintenance routines, marketing, and so on. There might also be specifics like legal regulations that require a certain type of expertise. This is where modular third-party suppliers can come into play.

Modular supply is master of puppets. But who cares as long as the show is good.

It provides a whole bunch of options to effectively scale the production and off-load some of the emaciating parts of running a business.

Fully modular

Multiple suppliers providing different products in no particular relation to one another. Financial products are very specific and delivered by multiple independent sources. This environment can potentially give an edge to some of the high-profile commercial platforms as they could enter targeted markets.

Fully modular is the Darwinian market where you either win or you suck.

It’s natural for us to invent the pathways that got us success. The amount of banking apps on our phones is nowhere near the amount on App Store or Google Play. We are naturally selective and there is no reason for us not to thrive in a fully modular financial aspect with no traditional institutions involved. We have the technologies to execute it.

Here’s Oliver Wyman’s explicit chart of all the possible niches for FinTech startups to delve into the fully modular industry structure:

Time to chime in

The viability of the modular format has been proven by multiple startups across all the industries. Generally, every industry where players compete for customers is a somewhat modular industry. Finance is no exception. The successful modular banking companies offer different layers of value, including the following:

- The customer-facing product

- The core of financial production

- The back office

All of them run different processes within the module. The customer-facing product displays interface and experience design is marketed, within its scope is advisory, research, and every customer activity possible. The core is in charge of the execution, fees, payment processing, risk evaluation, and decision-making process. And the back office is the administrative branch, keeping records, processing transactions, working with outsourced service suppliers, and basically running everything hidden from the end user and even some of the employees.

There is a growing race to make platforms satisfying modular demand for financial services. Functionality alone is not enough though, the experience has to be delightful.

FinTech will presumably evolve to offer mode modular experiences for the following points:

Pivotal moment solutions

Some financial decisions can change lives, yet there aren’t a lot of trusted solutions that can help you with those decisions. Buying a property often means selling the previously owned one which alone is a risky business. There is an opening for a modular FinTech startup here.

Solutions for 2 retail worlds

E-commerce platforms are well versed in processing online payments and generating digital sales, however, these platforms can be enhanced in order to present extra features for the physical stores. And vice versa. There is a huge gap in technological solutions offering both engaging and functional options for electronic marketplaces with point-of-sell presence as well. We plan to write more on this integration really soon.

Personal financial solutions

For the course of our lives, our financial states change. We are yet to witness the emergence of a lifelong financial planner/assistant. For it to be more than a just a monitoring and analytical tool, it has to showcase predictive features powered by AI and ML. The process could run in the background, resort to your bank accounts and other modular financial solutions that you use, the data is secure and private. This type of a FinTech startup is on the intersection of the cutting edge technologies and could present a huge value in the future.

Business financial solutions

Even within one business organization, there are different financial flows that do not always coalesce. Operations like import/export, retail, human resources, legal part, taxation, and so on, could be successfully modularized between different FinTech startups offering their specific segmented services. There might even be a solution to centralize the output from all those providers.

Image credit: Shakuro Design

There is something about non-linear FinTech startups that we still can’t wrap our heads around despite being involved in the development of a huge FinTech platform for over 5 years. And that’s how flexible and unpredictable smart FinTech platforms are. They do not harden up like traditional banks do and by being extremely controllable, remain sensitive to the ever-changing demand.

Due to the engrained agility of FinTech platforms, the newest UX design principles, as well as all the emerging technologies, can be used to gain a competitive edge. We’ve done a lot of pivots while building the MMKT platform, including complete rebranding, creating the mobile experience, adding a ton of functionality that is behind the scenes.

As a design and development agency, we only thrive in new and exciting projects. Data-driven production is our forte which combined with unorthodox design, lets our projects make the cut in such a competitive environment.

Why it is all worth it

Modular FinTech is a great window of opportunities for smaller tech startups looking to have their say on the market. The level of horizontal competition in banking and financing is so intense, it barely lets anybody in. Yet, if you chose the vertical development vector, this might be the disruption path you need. Deep-level knowledge of one particular financial aspect will be highly appreciated by those valuing the long-run perspective. And who’s to say you can’t scale to other aspects once you pioneer a specific service?

Within every opportunity for FinTech to shine, there is something current banks can already do without the need to revolutionize themselves. The reputation that banks have since the early 1800s, is the most precious asset of theirs.

Think of encompassing all the smaller value brought by the modular FinTech startups into a solid rim of a traditional institution granting safety and confidence.

This will help banks concentrate on trading and generating capital other than living on other people’s money. Competing with independent platforms offering better functionality for only a fraction of the bank cost, will get them nowhere. Instead, being a trustworthy umbrella for smaller and reliable startups can be a way to cement their place in the financial fabric of the future world.

Hero image by https://www.thepennyshop.com/